This article is both an investment thesis for ISA holdings and a demonstration on how we think about investing in general and how we attempt to factor for our own uncertainty in decision-making.

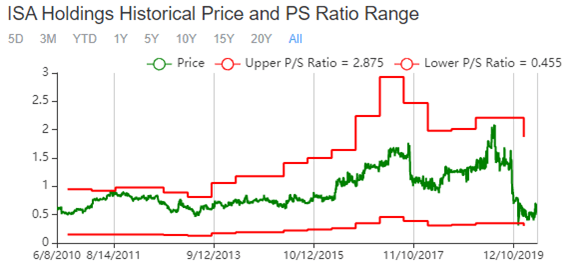

With approximately 23% of the share price being cold, hard cash and the company trading in the rock bottom ranges of its historical Price-to-Sales ratio range, we were immediately interested when we came across this tiny company in the corner of the JSE.

Now, ICT companies are typically something we put in our “too hard box”, as we usually understand neither the product nor the economics around the firm’s pricing power. However, ISA is a very simple company, with very easy-to-understand financials and an operating model very similar to management consultancy, which just so happens to be our industry. Thus, while we have little doubt that ISA management would be able to correct us around some of the specifics, we hope that for the most part they would agree with our understanding and exposition of their company.

As always, if you are looking to invest, we strongly recommend you read the entire article. If you are merely reading for interest sake, the bits in bold should suffice to get the gist of the article across in plain English. And if you’re really in a rush, the Explain Like I’m Five section above can act as a summary.

Disclaimer: At time of writing share price is 67c. We will admit, we bought in at 46c over March and have since seen the rise brought on by the catalyst we were expecting as the 2020 annual report came out. This has not brought the stock as high as we had hoped, but there has been enough of a price increase for us to be happy about the investment (45% in 2 months) and we believe there is still significant upside in the investment.

Microcaps and Mental Models.

ISA Holdings is a tiny company nestled in the corner of the main South African stock exchange: the JSE. When we first discovered it in early 2020, its 2019 price tag of R180 million had fallen to a whopping R70 million due to being downgraded by a key supplier. Just to give you perspective on how small this company is relative to its peers, at R70 million you could fit nearly 800 ISA-sized companies inside Bidvest – the smallest company in the JSE Top 40 Index. If that doesn’t quite hit home according to Pieter Du Toit’s book “The Stellenbosch Mafia”, ex-Steinhoff CEO Markus Jooste would occasionally drop R180 million on horseracing in one year alone.

Now, small microcap companies like ISA pose their own problems – they are illiquid, often very dependant on key personnel and are usually subject to far more volatility than the large stalwarts. Thus, when evaluating the investment potential of microcaps, one needs to borrow heavily from the Private Equity model of thinking. (Brandon Beylo of Macro Ops has a great article on applying such a mindset to the public markets for those interested).

In essence, while smaller public market investors like ourselves are not exactly in a position for investor activism, there are other things Beylo suggests we can learn from the Private Equity mental model when appraising an investment:

Serial Private Equity (PE) investors (excepting venture capitalists) generate higher returns typically through acquiring smaller sized companies through leveraged buy outs (LBOs) financed usually by the acquired company’s own balance sheet, applying activist policies to increase cash-flow (either to the PE firm, or via earnings to the acquired business) and selling the firm on a multiple much higher than that they bought at due to the increased earnings.

There are also companies which will merge with a business on motivations of strategic synergies, product/industry diversification or other growth hopes, but for the sake of our retail-investor heavy audience we will neglect these motivations.

The mental model of PE investing is thus one intently focused on:

- The downside (if you have a highly leveraged buyout, any significant drop in earnings can wipe you out, hence you will avoid “double leveraging’ by buying into a highly leveraged firm),

- The fundamentals (you have to be sure that you are buying at a material discount to intrinsic value else you stack the odds against you in being able to rapidly improve the company’s cash flow), and

- The long-term (you require several years at least to recognise the increased cash flow and the market’s appreciation thereof; also a long term horizon is necessitated by the illiquidity of the company’s shares: if it tanks in the short run – as microcaps are prone to do – you cannot sell).

Alright, comfortable with the mental model we will employ going forward? If you are a frequent reader, you probably should be – it’s value investing 101.

An overview of the investment thesis.

ISA Holdings is a very small, BBBEE certified ICT security company which operates in a niche market (predominantly financial services managed security systems). Approximately 70% of their income is recurring revenue and generates a very predictable cash flow.

The investment thesis is essentially this: being a SA Inc. company, being illiquid, and being a microcap mean that ISA is unlikely to interest international investors and is too small to interest local institutional investors. It is thus under researched and overlooked by the market at large. This means that it is subject to significant price/value dislocations. One of these dislocations occurred when the company released a statement saying they had been downgraded by their key supplier of software licenses (Checkpoint). Mr. Market overpriced in the depression in revenue likely to occur due to the downgrade (see ISA’s SENS on 16 January 2020 for more information). The price was driven further down by the onset of COVID-19’s devastation on all companies.

The price at which we started buying (45c per share) and indeed even the price today (67c per share) is significantly below intrinsic value (as shown in calculations towards the end of this report). Thus, the investment thesis is that the management will show resilience in returning the earnings to their 2020 levels by 2024, serving as a catalyst for Mr. Market to revaluate his view of ISA and revert to a price closer to intrinsic value. Should the market remain pessimistic, ISA will return (within the 4-5 years) to its regular dividend pay-out which we bought in on at a very low price for a forward-looking dividend yield of around 20-30% per annum.

This thesis is based on many assumptions, and we are most certainly not fortune tellers. As such we have tried to probabilistically weight our bets with as much conservativism as possible. As it largely rests on the company’s ability to grow earnings back up to the current level, a lot of time is going to be spent on evaluating the fundamentals of the company and the capacity of the management.

Now, back to ISA. They have a decently broad product offering centred around managed security services (MSS) such as authentication, remote access, intrusion protection and the like. Having begun way back in the early 2000s they rode the wave of selling firewalls and malware protection and used it as an inroad to the financial services sector. Due to the growing commoditization of these products however, they have – since 2013 – been actively branching into higher-margin services such as ICT security consultancy and higher margin products like cloud computing.

It is said that “niches make riches” – hopefully a truism in this case as ISA is highly focused on providing their services to the high-end banks and telecom companies where they are paid both for project work (non-recurring things like delivering and setting up the security systems or running risk assessments and threat hunting) and for subscription sales (recurring things like reselling security licenses or running maintenance and system support). The subscription sales account for around 70% of their revenue and contracts are typically renewed annually.

The company also historically receives about 10-12% of its income from finance income such as interest on its cash and loan accounts. Combine the fact that most of its cash is held in foreign currency and that most of its suppliers are international and we see that it is unusually subject to exchange rates. In their most recent annual report, management estimated that a 15% strengthening in the ZAR/USD would have strengthened net income by 35% respectively. This, in our view, along with the key personnel dependence typical of microcaps, poses a significant risk to the business and consequently our investment. We will dive deeper into risk analysis in the section on risk below.

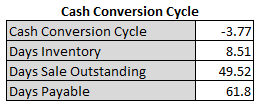

As far as operations are concerned, the company’s model is relatively simple: inventories consist predominantly of security software licenses for resale and are either bought once a sale has already been secured or are bought and quickly turned over (as indicated by the company’s low Days in Inventory and negative cash conversion cycle in Figure 1). Other than the inventory expense, operating cost is made up predominantly of the cost of hiring out ICT consultants (as it is a highly technical field, ICT skills are in high demand and employees make up a large part of operating cost). This cost however is not entirely a bad thing and as we shall see in the section on moats, may form a decently solid competitive advantage.

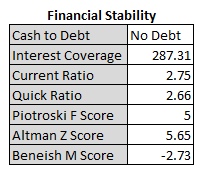

Keeping in accordance with our private equity mental model, ISA nicely ticks all the boxes of a very robust balance sheet. Figure 2 shows some of the key metrics one looks for in a stable balance sheet. There is no debt (outside of minor trade payables) and plenty of cash. The company is certainly solvent in the short run and has enough cash on hand (R45 million) to cover operating expenses twice over (R21.5 million). In effect, the company can run for two years without profit on it’s cash reserves alone. One thing we particularly enjoy about ISA, is that their management uses very little debt. They took out a debt position from 0 to 17.5% of equity in 2013 and paid it off completely by 2016. They have been entirely debt free since.

A brief word on the scores in the bottom three metrics of Figure 2: The Piotroski F Score is used to assess the strength of a company’s financial position and is ranked from 1-9 with scores above a 5 being good and below a 4 being worrisome. In the past decade ISA has only dropped to a 4 once and has typically ranged between 6 and 8. The Beneish M Score is used as a cursory probabilistic scan for accounting manipulation. Anything lower than -2.22 suggests that the company is not manipulating earnings. Finally, the Altman Z Score is used to assess a company’s likelihood of going bankrupt. Anything above 2.99 is in the clear and anything below 1.81 is in severe distress. While any one score on its own is not too informative, the ISA’s clear passing all three quite strongly reinforces the financial stability of the company.

Alright, so far we have established an overview of what ISA is, what it’s major risks are, how it operates and what it’s balance sheet looks like. What we have not covered yet are its growth and management.

Peter Lynch, the genius behind the Magellan fund, categorized companies into one of six categories:

- Slow Growers (large-cap, dividend-paying stable-growth companies such as Firstrand).

- Stalwarts (large-cap companies with strong fundamentals and growth prospects whom everybody knows such as Naspers).

- Fast Growers (while not necessarily as large or fundamentally strong as the first two, these companies are looking at very high growth rates driven by increasing revenues. An example of this would be Cartrack).

- Cyclicals (companies whose profits fluctuate in predictable fashion, usually in tandem with external factors like commodities. Afrimat is such a company).

- Turnarounds (companies which have recently suffered severe losses or near-bankruptcy and will return high profits if the turnaround is implemented successfully. Post-COVID, Comair could be such a company).

- Asset Plays (these companies typically have assets on its balance sheet that are not recognised by the market and offer investors the opportunity to buy these assets at very cheap prices. An example of a South African asset play would be African Rainbow Capital).

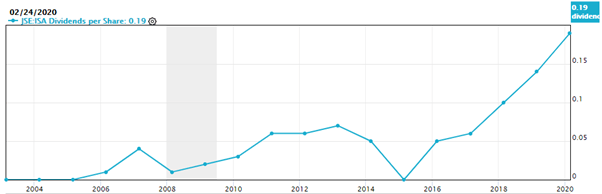

Now, classifying ISA according to these categories is a little challenging, as while it could be called a turnaround, it has been experiencing very decent growth and has very strong fundamentals. It is also nowhere near bankruptcy and has not (yet) experienced severe losses. In addition to this, ISA has done as typical slow growers would and blessed investors with increasing dividends over the last several years (Figure 3).

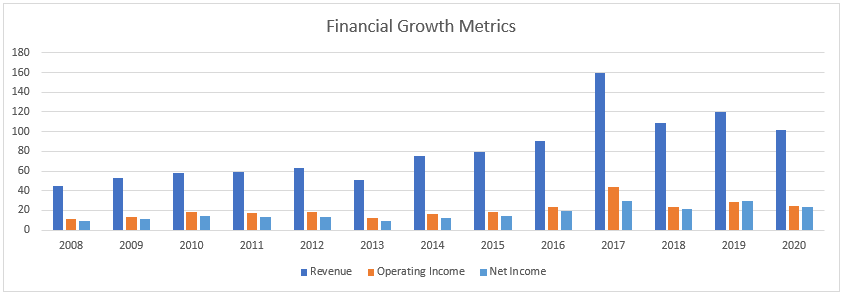

While not astounding and by no means a Fast Grower, the growth metrics for ISA have been very respectable. Figure 4 shows the growth rates of varying metrics over several time frames.

As you can see, ISA has been enjoying very respectable growth rates over the last decade, with much of the under-performance of 2020 coming from a stellar out-performance in the year prior (as shown in Figure 5.

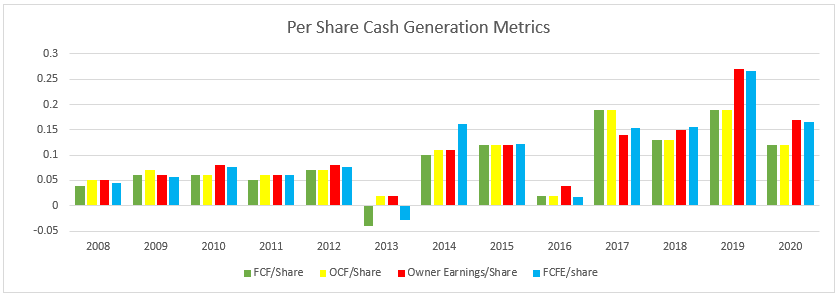

ISA’s management has a wonderful policy of matching income with cash flow. This has got to be by far our favourite policy of any company. Any company which gushes cash is an investors dream and, as you can see in Figure 6, ISA’s income (here measured as owners earnings per share, but is materially interchangeable with earnings per share) tracks almost perfectly with its cash flow.

On the topic of management, they seem to be very partial to shareholder’s interests. To illustrate this, in the last financial year, one of ISA’s debtors repaid a R20 million loan in full. The management promptly issued the entire amount and then some as a special dividend of 20c per share to shareholders (on top of the 19c regular dividend shown in Figure 3).

The only years the dividend has been missed thus far have been 2015 (during which they used the dividend money to fully repay the only loan of significance they’ve ever had) and 2020, during which the management has opted to keep the money in reserve to afford management the headroom to source alternate suppliers and address potential COVID-19-related issues. We believe this to be a prudent and wise choice indicative of a management who will not sacrifice sound business principles to smoothen their share price by putting unnecessary strain on the business’ finances.

We also found reading the annual reports to be refreshingly simple and clear, with management seeming forthright about issues, honest and fair about remuneration and not making any grandiose predictions about future performance. The board is diverse and all three executives have skin in the game, with 49% of the company being owned by directors (of which 36% is owned by the executives). The simplicity of the annual reports is emphasized by the fact that the company structure is incredibly simple, without any significant subsidiaries or other operating branches.

Finally, as with most of the companies we invest in, ISA is run by a founder/CEO, Clifford Katz, who has been in the game for 21 years. He is very knowledgeable about the industry and seems intent on giving easy-to-understand information to the shareholders and public. As an aside, in 2013 he ranked on a list of top 10 underpaid CEOs.

Right alongside Katz is Philip Green, the Chief Technical Officer. After graduating from Wits University with a MSc in Computer Science, Philip went on to found Internet Solutions – now South Africa’s leading internet service provider. In the early 2000’s he formed iSecure, a focused IT security company and joined the board of ISA in 2004 when iSecure and ISA merged. Philip now owns 13% of the company.

The final executive is Priscilla Mogoboya- the Financial director. Having been with the company since 2012, she was appointed to directorship in 2018 and is currently studying towards her ACCA qualification. She owns approximately 0.03% of the company, and also has skin in the game.

All-in-all, management have decent tenure, experience in the industry, and are under the oversight of a diverse and highly educated board (5 board members). Add to this that both the board and management have skin-in-the-game. We are fans.

All that mushy stuff said, we are cautious of reading into management too much. We have not met them, nor do we think that it would necessarily be a good thing if we did – there are too many tales of investors being taken along for a ride by a charismatic CEO (*ahem* Steinhoff). Hence, we place significantly more faith in the quantitative measurements of Figure 7. One other cautionary remark: in 2020, executives took home R6.7 million, up 55% from 2019, largely due to bonuses awarded. This does raise an eyebrow as metrics all round for 2020 were down from the previous year.

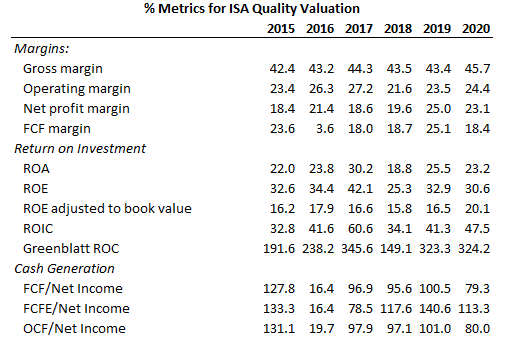

Several key takeaways from the block of text in Figure 7 are that:

- The management has consistently been able to compound capital, assets, and equity at above average rates, suggesting a very high calibre management team,

- ISA’s margin’s have remained comfortable and large, indicative of a sturdy competitive advantage (discussed below) and

- The consistently high correlation between income and cash flow speaks to the quality of earnings received.

In the past, management has distributed all this cash to shareholders. In time they will likely return to this policy, however over the next couple years they have indicated that they will prioritize the businesses financial position to ensure longevity.

The combination thus, of a management team capable of excellent returns, a cash flush operating model, growing revenue, and high margins suggests that ISA stands every likelihood of restoring earnings to their current level within the medium term. In the short term, they are likely to experience a very significant drop in earnings, but their strong financial stability stacks the odds in their favour for pulling through.

The Checkpoint down-grade

Given the centrality of the downgrade to our investment thesis, we shall spend a little time discussing it before we move on to the industry and competitor analysis.

Checkpoint (CHKP), PaloAlto (PANW) and Fortinet (FTNT) are currently the only real three names in cyber security software. Most of them offer highly complex products which require specialist knowledge to operate. ISA and other consultancy-esque resellers manage, integrate and sell these products, mostly to financial firms or other large clients mandated to have them.

In the past (1996-2010) Checkpoint was the only big firm offering such products. It enjoyed almost 100% market share and those who sold its products enjoyed a client base devoted by necessity. In the last decade however, PaloAlto and Fortinet have come to challenge Checkpoint’s market leadership, with the prior leader now a faltering third (as shown below). The latter two have purportedly better offerings with a greater focus on modern tech such as cloud computing. The narrative is that Checkpoint has seen its day and is now being outstripped by the younger firms.

Now, to-date South African financial institutions largely operate on Checkpoint’s software as ISA (which previously enjoyed the lions share of the market due to its partnership with Checkpoint in the early 2000s) had only offered PANW and FTNT’s products as ancillary offerings to complement their Checkpoint base. Therefore, going into 2019 PANW and FTNT were very keen to aggressively capture further market share in South Africa. Right. Now that we’ve established the history of the security firms, lets take a look at the recent events leading to the downgrade.

We have already outlined our perception of management, as such, it is of little use to harp on them further. Just because we are aware that charismatic management can often turn astute investors into suckers, it does not mean we are any less prone to suckering. That said, when we arranged a call with him to discuss the Checkpoint downgrade, we found Clifford Katz to be refreshingly blunt and honest about the company’s position. He spoke frankly and often referred to the cash inside the business as “shareholder’s money”. His manner of speaking was far less that of a large corporate CEO predicting future earnings and growth rates, and far more that of a small business owner engaging with the realities of running a business.

From Clifford’s perspective, the downgrade occurred like this: ISA and Checkpoint “grew up” together in the early 2000s and had a thriving relationship until the beginning of 2019. A new management took over the South African Checkpoint branch and the relationship quickly soured as Checkpoint allegedly began charging increasing prices to retailers (of which, ISA is by far the largest in South Africa). ISA believed the prices are not market related and, in November of 2019, refused to pay them (prices are largely variable due to the seller-rating of the company reselling Checkpoint’s product). Until then, because of their history, ISA had been Checkpoint’s highest rated reseller in SA. This standoff ultimately led to Checkpoint downgrading ISA to the point where ISA will not be able to sell or manage their products profitably.

Theoretically, this should not have cost ISA too dearly as, because of the consultancy nature, many of their clients had far more integrated relationships with ISA than they did with Checkpoint (who they hardly spoke to). Beyond this, prior to refusing to pay the fees, ISA had spoken to its customers about switching to PaloAlto or Fortinet and had received enthusiasm from around 2/3 of them.

However, the extraction of an old and integration of a new security system in institutions as large as those ISA serves, is a very complex and lengthy process. The onset of COVID-19 meant that all the customers ISA had planned to onboard to the PANW and FTNT systems were forced to renew their Checkpoint contracts with alternate resellers (such as ISA’s competitors: Dimension Data and Bizconnect).

This is where things currently stand. ISA’s ability to reclaim revenue in the coming years will thus be reliant on three primary things:

- Checkpoint’s offerings vs PaloAlto’s and Fortinet’s.

- The customer service of Bizconnect and Dimension Data vs ISA’s existing relationships with its clients.

- The switching cost associated with migrating from Checkpoint’s offerings to Palo Alto’s and Fortinet’s.

Clifford believes that PaloAlto & Fortinet’s offerings are materially better (hence the enthusiasm expressed by clients prior when ISA mentioned they wanted to leave Checkpoint) and we tend to agree.

Further, as consultants ourselves, we have seen first-hand the importance of relationship and longevity in the industry. ISA has been advising these clients for over two decades and is intimately familiar with their systems, strategies, and people. For competitors to replicate this relationship is very hard, and it is one of the reasons ISA as enjoyed its market position for so long.

Due to its extreme specialisation in security (as opposed to enterprise-wide system management), ISA has been unable to capture the market share of smaller enterprises who do not need such extensive security. While this has in the past worked against them, it is likely to play out positively here as the larger clients will have come to rely on such specialisation and its integration with their company. Neither Bizconnect nor Dimension Data are as specialised in security as ISA.

While the switching cost will deter some clients from changing products away from Checkpoint, both PaloAlto and Fortinet are aggressively pursuing market share in South Africa and have reached out to ISA with very competitive offerings. PaloAlto has even offered to refund any of ISA’s clients the existing book value of their Checkpoint system should they opt to replace it. This will hopefully go a long way toward mitigating the switching cost for clients.

As far as the future is concerned, Clifford’s expectation (pleasantly) matched ours in a conservative estimate of a 4-5-year return to current earnings level. He expects the coming year’s earnings to drop by approximately 60%, but affirms the company’s solid cash position and holds that ISA’s client relationships, niche expertise and new product offering should help them to reclaim revenue rapidly once the client annual contracts signed earlier this year are over.

Industry review and a competitor analysis

As we mentioned in the preface, we are not experts in the ICT sector by any stretch of the imagination, so undoubtedly many of the readers who are more familiar with the sector (or perhaps ISA’s management themselves) will have much to correct us on.

Our understanding of the ICT security niche suggests it has several headwinds going for it, and that companies with long-established relationships with clients are likely to develop respectable competitive advantages in their operating niche. ISA, which favours banks and telecom companies, likely enjoys such a “moat”.

The industry, being about security, essentially consists of three things: “keeping the bad guys out”, “letting the good guys in” and “keeping it all together”.

As constant evolution of attackers leads to a need for constant evolution of software catered to the client there is a need to “keep the bad guys out” that does not dissipate once a product is bought. As each client uses distinct software platforms, they need bespoke solutions – plug and play solutions are insufficient for those in financial sector given the real high risks of data violation. This leads to a software-as-a-service type model, with solid retention levels due to the high switching costs and tacit special know-how creating a moat around the recurring revenue. Thus, the high switching costs, the specialist knowledge and the absolute essentiality of the security makes for a very decent moat for ISA.

The industry has good tailwinds stemming from the growth in online banking in SA and the general ICT skills shortage in South Africa. The larger banks like Absa, Nedbank and Standard Bank are scrambling to digitize their offerings as fast as possible, to compete with industry leader FNB, the pioneer Capitec and upstarts TymeBank and Discovery Bank – all of whom offer more digital products. As ISA covers things like secure remote access, user identity management, virtualisation, and data protection (“letting the good guys in”) it will benefit increasingly and perpetually the more its clients develop their online models.

Further, ISA is a business process outsourcing (BPO) company. Complex, technical systems like those used to protect information in the financial services industry require lots of monitoring and tweaking. This is where the service component of BPO companies like ISA comes in. They “keep it all together”, overseeing the system, checking for leaks, and educating clients on its workings. This forms the bulk of ISA’s offering. Active service enables them to integrate themselves into the client’s business, grow relationships, drive sales, and otherwise make themselves indispensable.

There are predominantly two factors which drive BPO models: cost savings and technical knowledge. Usually, if a company can outsource a service for less than it costs to do it in-house, it will. This means that for highly technical services (like ICT security) it often costs companies less to get someone else to do it due to the high costs associated with internal hiring/training and the economies of scale that companies like ISA enjoy. This cost-saving headwind is especially useful to ISA when their clients are trying to cut costs (such as in a COVID-19-effected world).

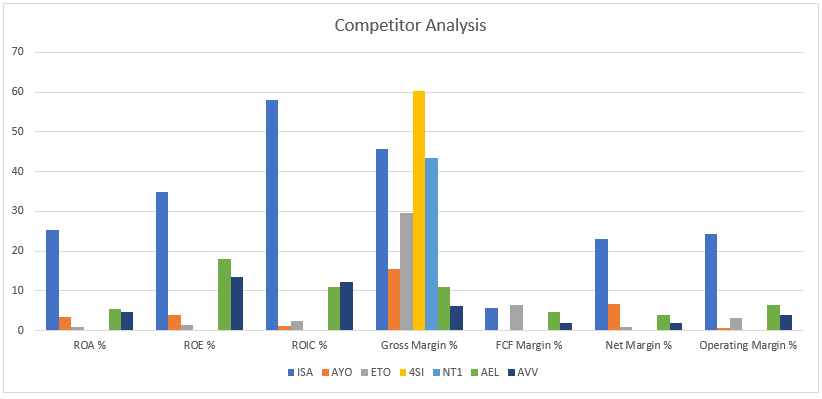

While ISA has many competitors in the ICT sector, its advanced fintech security niche affords it a relatively open market. Nevertheless, we have outlined a brief competition analysis below to show you how ISA compares to its peers. It is important to note that as asset light businesses (like ISA) require very few assets to generate very high earnings, this means their ROEs can be unusually high.

Figure 8 shows the drastic difference in returns and in margins between ISA and its closest public competitors. A quick note on the figure: the graph will not show negative returns or margins. The table below in Figure 9 will show a more detailed breakdown of the differences.

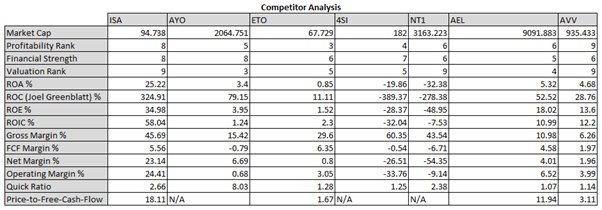

As mentioned, Figure 9 below will outline in more detail (but perhaps less stark a presentation format) the performance of ISA’s peers. While many of ISA’s peers in the ICT security space are private (primarily Dimension Data and Bizconnect), the ones listed below have their information publicly available, making them much easier to analyse. The ranks given for valuation and profitability as well as the financial strength score are of our own doing. They are based of several factors which we are happy to share but would make this article unnecessarily longer to unpack here. We hope the rest of the data is sufficient to convince you of the relative accuracy of the scoring.

As we can see, ISA is streaks ahead of its listed competition, with AVV and AEL being the closest competitors. Admittedly, none of them operate in the exact niche that ISA is in, however they are all ICT companies which have some security-related offerings – as close to competitors as we could get.

The big takeaway though is how much further ahead of its competition ISA is when it comes to returning capital, operating efficiently, and cornering the market. ISA’s exceptional returns are not “typical of its industry” when compared to its peers. Further, the high returns combined with high dividend pay-out in Figure 3 suggest that ISA’s business does not need much capital to grow other than investing in continuing operating costs.

In addition to this, the industry drivers remain very solid, with the move to digitization and cloud services rapidly increasing the need for increased security mandated for banks and financial services companies.

Risks

Alright.

So the investment thesis (that ISA will be able to recover from the downgrade from its key supplier and the market will reprice it nearer to its intrinsic value within 4-5 years, during and post which we benefit from high cash returns paid out at dividends or reinvested at superb rates) relies on the fact that ISA is a high quality company with good management. Hopefully, we are assured of this fact now. However, there remain some material risks that threaten to derail the thesis and pose real loss of capital.

We believe these risks to be the following:

- Exchange rate risk as most inventory is sourced overseas.

- Dependence on key vendors (Checkpoint case) & inability to offer new products to replace lost ones.

- Dependence on key personnel (only 3 executives & small 35-man team). We estimate this to be the biggest threat and should be accounted for duly.

- COVID-19 may cause debtors to default.

For the most part, operating as small retail investors, we are unable to use activism to mitigate risks. Hence, our only option is to be aware of them and factor for them in our decision-making.

In respect to the first risk, the exchange rate will do as it does. ISA hedges its exposure by holding forex reserves in the currency it will use to pay the suppliers, however beyond this there is little it can do without overextending itself into costly hedging strategies. We believe that ISA has managed this risk successfully over the past decade (during which the ZAR saw an unprecedented decline in relative value) and will continue to do so going forward. We have afforded this a 1/100 chance of being so detrimental that it wipes out the investment (i.e. South Africa experiences a Zimbabwe-eque currency depreciation).

Regarding the key vendor risk, this was one that unfortunately blew up towards the end of last year with the Checkpoint downgrade. Management has since begun to engage with a new supplier, NextGen, and believe – per company SENS – that clients will react positively to NextGen’s offering. Nevertheless, the risk remains pertinent. The company could face a similar situation where NextGen decides not to do business with ISA (as Checkpoint effectively did) and ISA would experience a repeat of the downgrade. While we do not afford this a very high probability of happening (about 1 in 50), if it were to occur, we could lose the entire investment. We have also afforded the probability that the client base completely rejects NextGen’s product and ISA ultimately liquidates given no revenue income a 1/50 chance.

The third risk boils down to: what is the likelihood that Katz or Green leave the company? Katz has been CEO for 21 years and is 50 years old. We estimate that his leaving in the next 5 years is unlikely, but the probability between 5-10 years increases quite a bit. Philip is much the same, having extended tenure but also a decent decade or so before retirement age. Regarding succession planning, Clifford has said that he is in the process of grooming his sales manager to take over his position, however as yet he will admit that the business will still take a decent knock should either himself or Philip Green kick the bucket. Neither have any intention of leaving anytime soon though, thus, we have incorporated this risk as a 1/50 chance that a departure from the company leads to a total wipe-out of our investment.

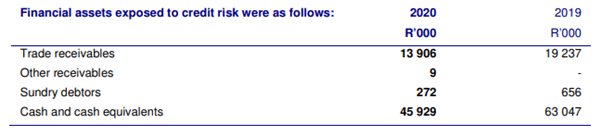

The final risk is significantly more probable than the others to occur, however it is much less likely to lead to a devastation in share price as (unlike the banks), ISA does not rely much at all on debtors for income. However, as their clients are largely financial companies ISA is indirectly exposed to this possibility. ISA’s debts receivable amount to 2 million. These can be written off (on COVID-19 basis) without materially effecting the company’s cash flow. A further possibility could be that the financial companies holding ISA’s cash and cash equivalents account and the clients with sales outstanding could potentially default and ISA may not be able to retrieve its funds. All in all, we do not believe the likelihood of any of these latter occurrences happening to be very high, but their impact on ISA’s financial position would be immense (Figure 10).

Post COVID-19 there are two possible scenarios for ICT’s recovery in the financial sector. As banks are cutting costs to preserve liquidity, there can be only two real outcomes:

- Mean reversion: ICT spending is core to banking, thus ICT spending is simply getting pent up in the system and will likely recover aggressively within the short to medium term.

- New normal: Increased cost pressures coupled with some degree of banking sector deflation or commoditization have forced banks to change their spending habits on ICT and this lower level of demand for technology from the sector is here to remain.

Given that the banking sector spends roughly a fifth of the total ICT spend in South Africa, the 2nd scenario is a key systemic worry for the local ICT sector and one to carefully consider going forward. We have assigned the probability of total loss of investment for the combination of these factors to be 3/100.

One risk we did not mention above, as it would not be material loss to the company, but would effect the investment thesis, is the possibility that a private equity firm or competitor is enticed by ISA’s depressed price tag into a merger or acquisition. In this case, our investment thesis would not play out and – given the short-term volatility – our investment could yield much lower than we estimate. We have assigned the likelihood of this happening as 1/100.

All in all, this is a 9% chance of total loss we will account for in the odds section below. We add to this a conservative 6% buffer and our chance of total loss accounted for becomes 15%. It is important to note that we do not realistically ascribe the odds of total write off as 15%, but we want to account for them being that high in our estimates of risk. Before we dive into the odds and outcomes however, we must try determining the intrinsic value of ISA.

Valuations and Odds

Most times, you could ask 100 analysts their estimate of intrinsic value and you will receive 100 different answers. The goal of the investor then is not to be 100% accurate, but to make a decision that is approximately right enough that you return a decent amount on your capital. As such, we have provided a range of approximate valuations below using various methods, some more appropriate than others.

Charlie Munger said: “To us, investing is the equivalent of going out and betting against the pari-mutuel system. We look for a horse with one chance in two of winning, and that pays three to one. In other words, we’re looking for a mispriced gamble. That’s what investing is, and you have to know enough to know whether the gamble is mispriced.”

Since we have opted to run a concentrated portfolio, we must inevitably be incredibly picky in the companies we choose to invest in. We want the numbers to scream “This is a good company!” and the price to scream “I am dirt cheap!”. As Buffet said, we are trying to jump over a 1-foot post rather than vault a 10-foot wall. In most cases, 1-foot poles and numbers that hit you over the head with their greatness will be found long before you come across them and will be priced accordingly. Hence, we must structure ourselves to find bargains in nooks and crannies that most others do not look in. One such nook is microcap South African stocks.

There is an old saying that “profit in an illusion, working capital is a reality, and cash flow is the dream”. Ultimately, any good valuation comes down to predicting future cash flow and discounting it to the present value. This means that there are a whole host of assumptions we must make when attempting to determine this future cash flow, and the more ignorant we are of the business and industry, the less likely our predictions will be correct. This is why we have spent so long discussing both ISA and its niche, so we can try to mitigate much of impact of ignorant speculation. To further mitigate the effect of our ignorance, we have tried to assign probabilities to various outcomes, as well as to factor for our uncertainty around our probabilities.

In our articles on Afrimat and Cartrack, we outlined some of the way we value companies. If you are interested, give them a read to better understand our valuation process.

To save time, Figure 11 is a back-of-the-envelope discount-cash flow model that will demonstrate the basics of our method. We assumed that the company turns no profit in 2021 due to a combination of COVID-19’s cost pressures on clients, and an uncertainty around ISA’s new NextGen product offering. We also assume a 15% discount rate (high, but not altogether too high given SA’s current bond rates as the “risk free” rate) and use a Price Earnings multiple of 7.5 to exit the investment in 10 years’ time.

This is a very conservative estimate (as you have seen the historical growth rates), and still places the intrinsic value at 89c per share. This means we are buying at an approximately 32% discount to intrinsic value.

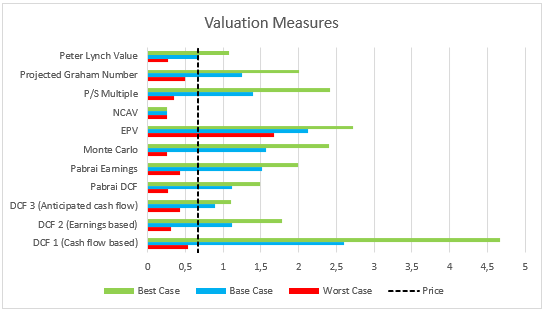

In our valuations, we have run three scenarios (worst case, base case, and best case; with 25%, 40% and 26% probabilities respectively) through 5 different types of DCF models. We have also compared our models with the same scenarios run through classic formulae like the “Graham Number”, “Peter Lynch Value”, Maximum, Median and Minimum Price-to-Sales Multiples, and have worked out the Net Current Asset Value for ISA. If you do not know what any of these are, a quick Google will explain. They are all somewhat useful for approximating intrinsic value, however it is in combining them that one can derive some very useful results.

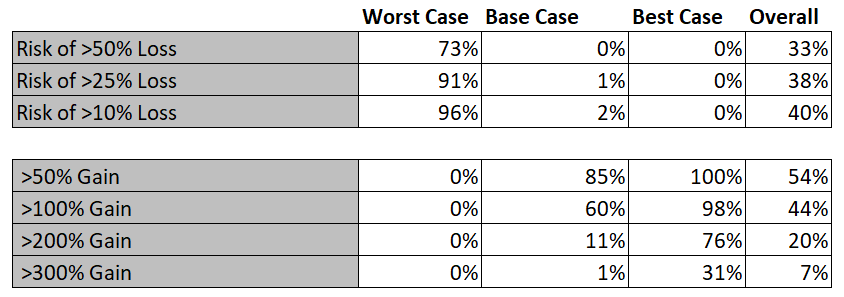

You will note in the figure above, that there are several Monte Carlo simulations (which is where a computer generates a bunch of random outcomes based on the same starting point), each with starting points based on the three scenarios mentioned earlier. We also briefly cover the Monte Carlo simulation in our articles on Afrimat and Cartrack. These simulations do help us approximate a value based on a future Price/Earnings estimate and an Earnings per share estimate, but their real value lies in being able to outline a normally distributed risk and gain possibility.

Figure 13 below shows us how many of the randomly generated outcomes result in the various risks or gains. This gives us an approximate idea of how likely we are to really risk capital loss. As you can see, there is a big difference between the best- and worst-case scenarios. This is because, given our ignorance and inability to estimate with precision, we have tried to cover for a great number of possibilities in our evaluation. The “Overall” probability includes a 15% chance for complete wipe-out (as mentioned in the risks segment) and has been calculated by adding the products of the probabilities across scenarios and the respective probability of that scenario occurring.

For instance, there is a 73% chance of losing half our money in the worst-case scenario. The probability that the worst case occurs is 25% and the probability of total loss is 15%. Therefore, because there is no risk of losing half our money in the best and base cases, the overall likelihood of losing half our money is 33% (73% x 25% + 15%).

Finally, we run our results through the Kelly Formula, a very useful tool for bet-sizing and portfolio allocation. The Kelly formula calculates the optimal “bet size” one should place given the odds of a win and the win payoff. Renown investor Mohnish Pabrai has written on it at length in his book “the Dhandho Investor”, and it is a tool that we have become increasingly convinced of using, especially in the face of uncertainty.

The Kelly formula can be calculated several different ways. In Figure 14 above, the outcome we most rely on is the one with the little purple banner. Here, anything positive suggests that the bet is in our favour and in this case, Mr Kelly suggests it is a good enough bet to risk 32% of our entire portfolio on. This requires a little more tolerance for portfolio fluctuations than we have, but nevertheless affirms our belief that our idea is a good one.

Also, the probability for total loss (the figure with the little red note) is the same as the 9% we mentioned above in the risks section. We understand this may be a little too mathematic for some readers, but the key takeaway should be this: ISA presents a very lopsided bet.

The Kelly formula and the Monte Carlo simulations serve predominantly to factor for our own uncertainty and ignorance in this process. They are essentially an acid test to our basic thesis, and if we pass (as we did), we can be reasonably certain that we stand a good chance to make a buck.

Judging from the valuations in Figure 12, we can see that ISA is priced very near to its worst-case scenario, and well below the conservative base-case. We believe there is very significant upside for the enterprising investor, with little real risk relative to reward. In our base case, priced at 67c per share, we believe that ISA is an investment that will compound our capital at 28% per annum for the next 4-5 years, thereafter we can re-evaluate. As it is a wonderful business, our guess is that we will hold it for much longer than 4-5 years, especially if we were able to buy in to the high dividends it has historically paid out, at the low price that it is currently trading at.

As a final note, we would like to point out that ISA is unlikely to be a 10 or 100 bagger. Its niche market and extreme specialisation prohibit it from using much more cash than it currently is. This constrains its size and ultimately prevents it from compounding at the superb rate its ROE implies. We believe we reasonably stand to return between 2-4 times our money over the 4-5-year period given the catalyst of management being able to restore earnings above the market’s expectation.

After that, we will have an excellent, cash-gushing company which was purchased at a multiple far below its usual.

Hi JD

Very, Very Impressive.

Digesting this theory requires some depth of understanding – but a great insight into financial risk taking, and so diligently put together.

It also shows much of the author’s passion and acumen for what is developing under the bonnet !

Keep it up JD – such an incredible undertaking and very easily coached through a language that says “we do not have it all” but “this is my best shot”, and it’s only going to get better.

You’re going to get a lot of followers, introducing the depth to which one needs to go to extract the juice.

Loved the read.

Love GP,

*Tim Hoskings* *C: *082 459 2960 *T:*031 705 7744 *www.books2you.co.za*

The information in this e-mail is confidential. It is intended solely for the addressee. Access to this e-mail by anyone else is unauthorised. If you are not the intended recipient, any disclosure, copying, distribution or any action taken or omitted in reliance on it, is prohibited and may be unlawful. Whilst all reasonable steps are taken to ensure the accuracy and integrity of information and data transmitted electronically and to preserve the confidentiality thereof, no liability or responsibility whatsoever is accepted if information or data is, for whatever reason, corrupted or does not reach its intended destination. Any view or opinion expressed in this message may be the view of the individual sender and should not automatically be ascribed to the company

LikeLike