Introduction

In 1951, a twenty-one-year-old Warren Buffett wrote an article about GEICO titled “The Security I like Best”. He begins by admitting the broader market was “riding [the] wave of prosperity”, but that the auto-insurance industry had not shared in this ride and was home to many under-priced stocks.

In the article, he outlines GEICO’s business advantages, its cost structure and industry tailwinds, and concludes that its price-earnings multiple of 8 does not adequately price in the growth prospects it faces. The market’s average price-earnings multiple in 1951 was 7.2.

As a fan of the man, this article is also on the security I like best. The broader market has again ridden the waves of prosperity for the last decade and, like the 1950’s auto-insurance industry, South Africa has not shared in this ride. In 2021, the average price-earnings multiple of an S&P 500 company is 37.97. Cartrack’s is 30.7 at the time of writing.

Cartrack is an organically grown telematics and data analytics company. They are vertically integrated, competitively advantaged, with an owner-operator who has sizeable skin-in-the-game and draws a humble salary. The bulk of their revenue is software-as-a-service, they have industry-leading margins and unit economics, and have offline offerings which differentiate them from their peers. Their vertical integration buffers them against cost-pressure, allows them to be the lowest-cost provider, and improves business agility, innovation, and execution.

The telematics industry is capital light and winner-take-most, with the market leaders benefiting from scale through better distribution networks, larger data pools and greater potential for upselling products. The flywheel effect of more data allowing better analytics, which draws more customers into the ecosystem trends the industry towards winner-take-most. The industry has hefty tailwinds in insurance companies adopting telematics for risk modelling, regulation requiring commercial driving data tracking and broader IoT adoption, autonomous vehicles, and smart-transport systems. For a high-level understanding of telematics as it relates to insurance, have a look here.

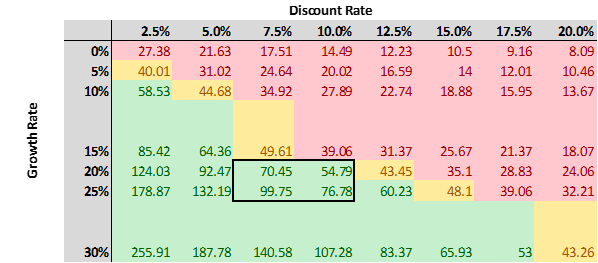

Valuation is always more art than science. Because of the quality of the business, its offshore exposure and the current levels of international money supply and interest rates, a discount rate will likely be on the low end. Additionally, the expected growth of the company can be projected linearly, however this will not account for the embedded optionality Cartrack carries (Figure 1).

The thesis for Cartrack is that it will a) grow cash flow at a faster rate than the roughly 18% per annum that the market is pricing in, b) it contains embedded optionality, obfuscating the expected growth rate, c) continue to compound capital at high rates for a long time going forward, and d) provide a strong inflation hedge given its robustness to interest rate movements and strong pricing power. The primary risks here are several: short term trading multiple compression, key-man and political risks, buyout risk, and a faster-scaling competitor.

This article will dive into much of the above, segmented into context, quality, growth,and counterweights (major factors and risks to be cognisant of).

Context

For the uninitiated, Cartrack’s main role as a telematics company is to provide fleet management software and analytics to logistics companies. They provide a dashboard to management (think Waze, but for many different vehicles at once) which lets them communicate with drivers, have access to all kinds of data analysis and send on-the-go updates.

Industry Overview

The telematics industry is increasingly differentiated by the ability of some players to offer an IoT ecosystem rather than IoT solutions. Per a 2019 Deloitte article:

An IoT solution consists of sensor networks that generate various types of data that a company can analyze to create insights for making business decisions. An IoT ecosystem links those solutions with other digital tools and technologies to create even greater value for the company and its customers.

Most notably, these tools are artificial intelligence and predictive analytics. Both require immense data (the first, to train, the second, for accurate predictions). Thus, the more data a IoT provider has access to, the better their ecosystem.

Historically, the people who use telematics the most are logistics companies who use it for increased fleet productivity and efficiency. Increasingly however, insurance agencies are pushing individuals to adopt telematics so they can better price risk premiums and the like. Cartrack has even stepped into the pseudo-insurance offering with their R99 p/m stolen car recovery guarantee.

Characteristic of the telematics industry are high margins and low capital expenditure or working capital. The marginal costs of distribution, tracker production and analytics software are very low, but revenue is recurring and powered by the user-generated data gathered.

Since bigger data pools mean a competitive advantage, rapid scaling is key. This is why Cartrack (and others) spend so highly on marketing. Further, because the industry is shifting away from simple tracking towards advanced analytics, a lot of money is spent on research and development to keep pace with industry innovation.

The total addressable market is not clear yet. Mix Telematics estimates the current commercial vehicle TAM to be around $90B[1] and current penetration to be 17%, which would put Cartrack at roughly 1% of the total market and 0.15% of the commercial vehicle TAM. This excludes the individual consumer TAM, which is likely equally large. The telematics industry is expected to grow at roughly 20% per year between 2020 and 2025[2]

Because of the low capex and attractive return potential, one would assume there are a flood of entrants to the telematics market. However, governing entry (and incumbent market share gain) are four primary barriers:

- Each original equipment manufacturer (OEM) has their own architecture and specifications – new entrants will have to partner with OEMs on a pre-install basis to maximise data gathered on each vehicle.

- Existing data pools and scaled distributions prevent entrants from offering the same level of analytics or installation service as incumbents and disincentivize customers to switch.

- Given the nascency of the industry, R&D and marketing spend are necessary to compete in rapid scaling before a steady state is reached.

- A lower-level manager of a logistics firm cannot simply implement a fleet management system. For many of the larger clients, only senior management (with incumbent relationships) can make the decision.

In terms of business drivers, commercial demand for cost control and efficiency gains underpin most of the logistics’ adoption. There are also tailwind regulatory requirements as governments make efforts to improve road safety, as semi-autonomous driving takes centre-stage, as OEMs seek to manage vehicle warranties and service dates, as insurers adopt telematics in risk pricing and as consumers adopt tech that requires in-vehicle connectivity and IoT. In developing markets (where Cartrack operates), there is also crime protection.

Competitive Overview

South Africa does vehicle theft, rugby, and financials really well. In each of those categories, we have flirted with the top of the log for as long as most can remember. Our banking and insurance sectors are world class, as are the Springboks. Our crime rate is unfortunately world-leading too.

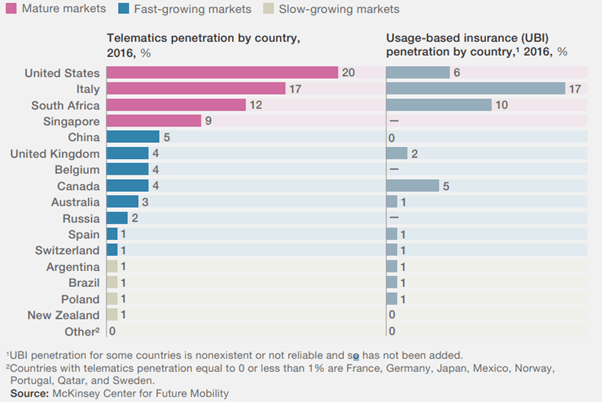

An odd outcome of this milieu is that we have top-notch telematics companies. The combination of high-crime and proactive insurers has been an unusually rapid combination of adoption and innovation in the telematics market. Mix Telematics and Cartrack (two of the global leaders) both come from South Africa.

Figure 3 below gives a high-level idea of different market penetration rates. South Africa and Singapore are both pretty mature markets (Singapore is the headquarters for Cartrack’s R&D centre).

Cartrack is a top 10 global player and is already the market leader in many of their geographies. However, the thesis rests on their scalability and their holding that market leader position. So, what sets Cartrack apart?

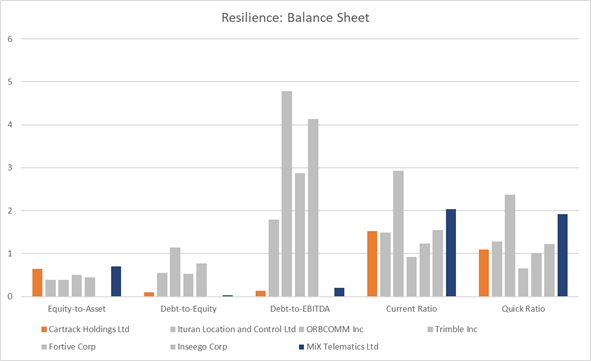

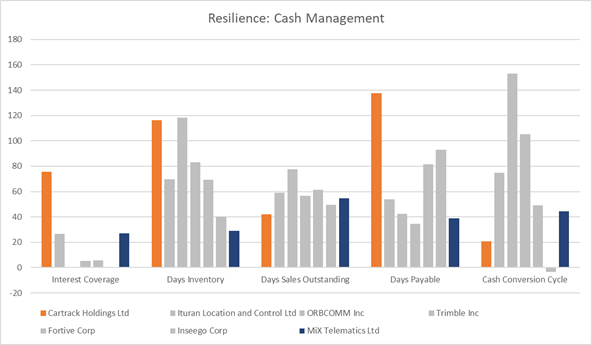

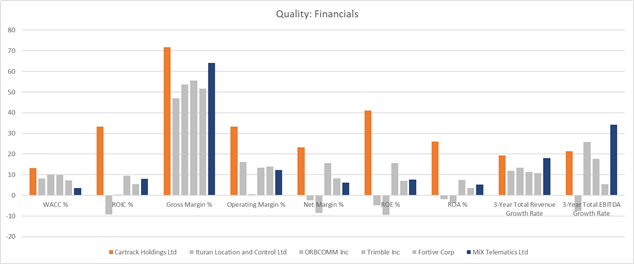

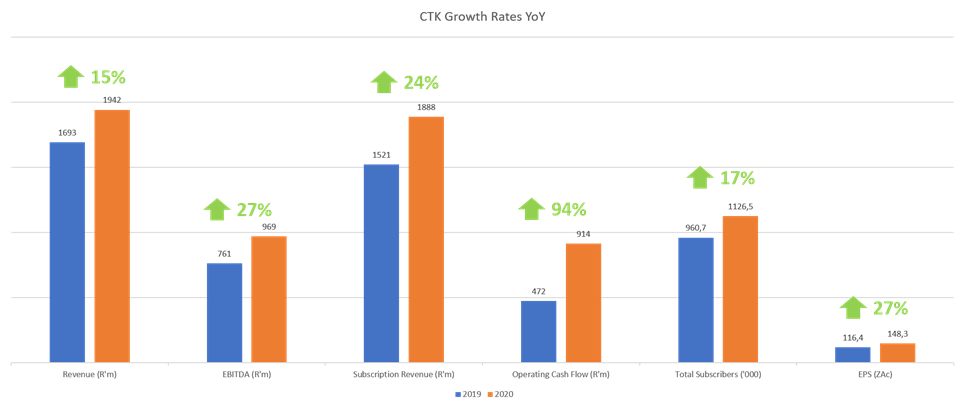

The easiest first look is at the financials. Cartrack is second to Mix Telematics in their balance sheet resilience (Figure 4) and takes first place in their cash management (Figure 5). They lead comfortably on their margins, returns on capital/equity, 3-year revenue growth, and are third in 3-year EBITDA growth rate (Figure 6).

Qualitatively, Cartrack’s product UX is terrific and anecdotally all of the logistics providers I spoke to both used Cartrack and said they found it streaks better than any alternatives. The three major differentiators between Cartrack and their competitors are:

- Their vertical integration and organic growth allow more agile innovation and implementation and gives them buffer to be the lowest cost provider. It is challenging for the software-first competitors to incorporate the physical design and production elements necessary for vertical integration – both because of the experiential challenge, and because their cost structure has not grown with vertical integration in mind.

- Cartrack’s offline vehicle recovery warranty and in-house IP separate them from SaaS/cloud-only providers.

- In early 2019, they began installing their tracking devices at the OEM level, both broadening customer reach and lowering costs through replacing the advertising/trial/sale model in part with pre-sale installation costs. OEMs win because they can more effectively manage warranties/service due dates and provide extra value-add services, while Cartrack wins through the added reach and cost benefits.

The effect of these three aspects is to flywheel extra customers and extra data through the Cartrack system. They keep and process their data entirely in house and do not sell it. This data is what enables Cartrack to offer more accurate and advanced predictive analytics and underpins their telematics ecosystem.

Their cost advantage is also sizeable. A large US competitor – Samsara – price themselves around $129 for the hardware and $400/year for small to midsize fleets whereas Cartrack is roughly $125 per year in total.

Quality

What is a high-quality business? Roughly speaking, it is a business with a high enough degree of resilience to external and internal vicissitudes that it is able to stay in the game for long enough to compound cheaply financed capital at high rates of return for a long time.

Business Resilience

Cartrack is a resilient business in most every sense that counts. Their vertical integration and the in-house IP and hardware development buffer them against supplier dependence and increase their agility and execution speed. The fact that their customer base is diversified across subscriber types, geographies, and a broad number of subscribers and industries buffers them against demand troubles too. No customer contributes in excess of 10% of their group revenue.

As a capital light business, whose mission-critical product carries high switching-costs and gives them substantial pricing power (especially on the upper bounds of their product range), they are a decent hedge against inflation. They are not affected materially by changes in interest rates given their conservative balance sheet and eschewing of long-term debt.

Their hefty marketing spend has positioned them as the premier brand in Sub-Saharan Africa, and they are focusing on replicating this brand positioning in Asia and Europe. They put considerable effort into their branding and carry an enviable reputation in the market. This is enhanced by their pre-sale installation deal with the OEMs, solidifying their reach and market position.

From a unit economics perspective, they generate roughly $56 per subscription off of a revenue of $125 at an EBITDA margin of around 45%. They have an average subscription lifecycle of 64 months, which tracks well to the average length of vehicle ownership before replacement. This technically gives them a churn rate of between 15-17%, which is rather misleading given that many customers opt to re-sign with a new vehicle. Their customer retention rate here is 97%.

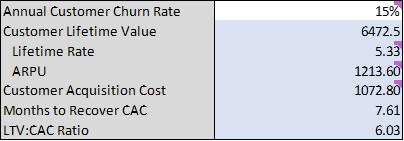

Figure 7 breaks down the unit economics further. Herein lies the crux of the company’s resilience. They make back their cost of acquisition in roughly seven and a half months, while the lifetime value of a customer is 6x their cost of acquisition. As a scaled, growing and already-profitable SaaS company with a long runway for reinvestment, strong industry tailwinds and decent unit economics, Cartrack is in a very robust position.

Their model is highly cash generative as customers pay in advance, revenue is recurrent and essential capital outlay is minimal. This year, Cartrack yielded a 25% FCF margin (as opposed to the 2-3% margins in 2018 and 2019) as they opted against reinvesting cash as heavily due to the COVID-caused disruptions. This gives us a decent reference point for what steady-state cash margins would look like.

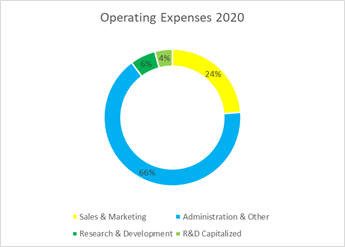

To have a summary look at their cost structure and revenue model, Figure 8 outlines Cartrack’s revenue sources and Figure 9, their expenses. Again, their spend on R&D and marketing speaks to the early stage in their telematics S-Curve that they are in. The margins in Figure 6 above provide a reference for their cost structure relative to peers, while the leverage ratios in Figure 4 also speak to their relative gearing. Since debt fragilizes, Cartrack’s general conservativism reinforces their resilience without dampening their balance sheet efficiency.

From a legislature perspective, Cartrack is on the right side of the legal trend. To quote perspicar744 from their excellent VIC writeup:

Government regulations have been passed in many jurisdictions requiring commercial fleet managers to use electronic logging devices (ELDs) to track data and provide reporting on a driver’s Record of Duty Status (RODS) to improve safety and reduce carbon footprints.

-perspicar744, VIC, July 2019.

In the US for example, under the ELD mandate, commercial driving operations must now keep records and file monthly reports on HOS (hours of service) and the IFTA (International Fuel Tax Agreement), and daily Driver Vehicle Inspection Reports (DVIR). Similar [regulations] such as Europe’s E-Call initiative, Brazil’s Contran 245 Mandate, DLT taxi GPS in Thailand, and many others elsewhere are eliminating the old paper-based tracking systems and driving demand for turnkey solutions.

Two other aspects of resilience are the company’s access to and needs for capital, and their cash conversion cycle. Figure 5 above has already spoken to their relative cash conversion standing; they take on average 20 days to convert investments into resources and inventory into cash – this leads their peers comfortably. As for their capital demands, they are very light because of the low marginal costs associated with each subsequent customer. Most capital expenditure will be funnelled into research and development to maintain an innovative lead in a steady state. Because of their financial stability, Cartrack is able to raise debt capital relatively cheaply. Their listing on the NASDAQ should also help them to raise equity capital at a cheaper cost too.

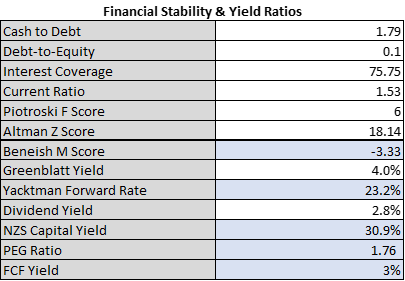

Figure 10 beside has a couple summary ratios and heuristics used to gauge a company’s financial security. The gist of all these figures is that the company is in a very secure position.

The yields are various methods of estimating future returns given historical growth rates and FCF yields and the scores are metrics used to determine likelihood of imminent bankruptcy or financial shenanigans.

One flag around business resilience would be Cartrack’s shareholder base. With 80% insider ownership and founder-CEO Zak Calisto owning 60%, there is considerable risk to minorities that their interests are brushed aside. On the other hand, this founder-mentality and skin-in-the-game certainly aligns Zak with shareholders and with making good long-term decisions.

Management

The benefit of having such a concentrated ownership in the founder is that it goes a long way towards avoiding the Innovator’s Dilemma. Here is a recent interview with Zak – in it, notice the mindset towards innovation, long-term planning and addressing new markets.

The Innovator’s Dilemma, as put by Clayton Christensen, is the idea that firms are disincentivized to invest appropriately in disruptive technologies because of their small market today, their low immediate potential for returns and the individual incentives of good middle managers to avoid low-returning projects.

As someone who has most of his family’s net worth in a business, he built from the ground up, Zak is incentivized to avoid short-termism. Truthfully, his customer-centricity (which comes through in many other interviews) may dampen this positive incentive. Per Henry Ford if you had asked customers what they wanted they would have said faster horses. However, Zak’s shrewd capital allocation to date and heavy focus on R&D suggests a wiser approach towards internal spend and it is likely his customer-centricity is reinforced more in Cartrack’s UX and service than in their capital allocation. The returns in Figure 6 above echo this sentiment with ROIC reaching roughly 33% for 2020.

A final word about Zak, in 2020 he earned a financial year-end bonus of R284,000, bringing his total package to R3.84m. For the CEO of an R18 billion company, this is a very humble salary.

Staff churn is notably high at Cartrack, but so are the base salaries. Employees are paid well in cash relative to peers and the company avoids stock options. Reviews on Glassdoor suggest a pretty demanding working environment where employees are pushed hard towards delivery – a sentiment echoed by Calisto in the interview above. Several reviews mention micromanagement. Ideally a company like Cartrack would be more decentralized. Moving the decision-making to where the information lies is usually a better way of ensuring you are well positioned for industry trends. This culture is somewhat concerning, it seems to view value creation as zero-sum where employees are turned over quickly.

Anecdotally of the several employees I have spoken to, they seem very content. The SA CEO greets most employees by name, and many have commented on the “flat structure” and lack of ego-stroking titles. Another common theme is the hard work ethic, but this is spoken of positively and none described it as excessive. This is in contrast to the reviews on Glassdoor, which admittedly typically have a sample of disgruntled employees who draft reviews. As far as strategy goes, Cartrack’s intent is to focus on their four primary growth drivers:

- Connected vehicles – through leveraging the OEM partnerships and to continue to grow in the materially underpenetrated global market.

- Technology investment – increasing emphasis on maintaining their tech-lead in the industry. This will work out as continued R&D spend.

- Increased demand for data analytics – continuing to develop centric solutions for both predictive and as-is analytics.

- Cross-selling and new product development – such as their cost accounting software and live video streaming management tools.

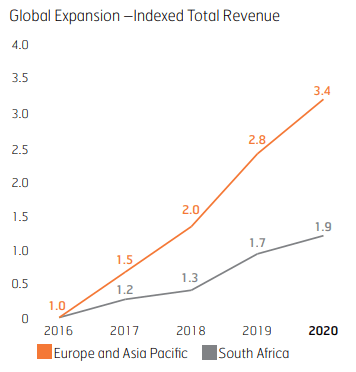

They are intent on growing their ex-SA market share, as evidenced by their graphic in Figure 11.

Moat

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business.”

– Warren Buffett

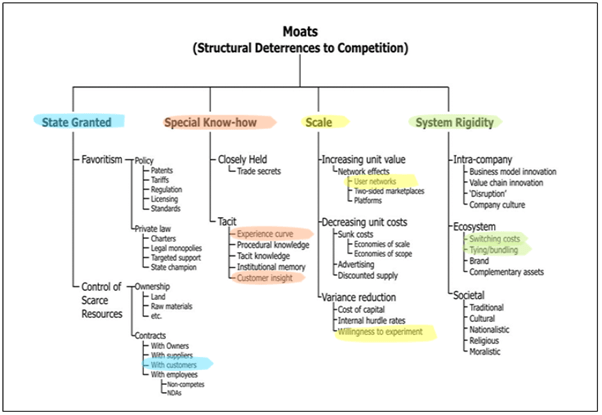

One cannot discuss quality without discussing competitive advantages. Much of this has already been discussed under competitive overview and will not be rehashed here. This section will be a filtering of Cartrack’s competitive advantage through several models put forward by several prominent investors.

In Chapter 4 of their paper on Complexity Investing, Slingerland and Johns of NZS Capital argue that traditional “moats” are built around a lack of free-flowing information. They contest that Porter’s well-known 5 Forces are anachronistic, and that modern businesses should rely on innovation, adaptability and providing more value to customers than competitors to build large network effects which reduce their vulnerability.

Innovation and rapid market-testing of new products are part of Cartrack’s make-up. In 16 years, they have built 13 different solutions ranging from insurance telematics to fleet administration off the back of what began as a simple vehicle tracker. Many of these initiatives began without profitability and were subsidized by the dependable revenue that their major platforms provide. Further, Cartrack has been actively innovating at the low-end of the market (specifically consumer-focused) – an example of which would be their R99 theft warranty.

In their article on Pricing Power, Ensemble Capital suggested that pricing power can be divided into two camps: one which consumers are happy to pay (e.g. Apple’s premium range), and one which they begrudgingly pay (e.g. Valeant’s yearly 50% drug price increases).

They contest that companies which raise prices through customer exploitation are “mortgaging their moat” and are accruing risk towards some future blow-up.

Cartrack is in the fortunate position of holding pricing power given the mission-critical nature of their product for many logistics firms. This increases the more companies rely on their products. However, Cartrack holds the lowest-cost provider position and have kept base prices flat for the last several years, profiting instead from optional add-ons at small prices relative to their customers’ overall cost structure. Because of the price-sensitivity of logistics companies, this most certainly constitutes a moat.

In his Saber Capital article, Connor Leonard outlines the benefits of having a reinvestment moat. This is a moat which allows a business to compound capital at high rates for a long period of time. These companies need long runways in underpenetrated markets, network effects, and low-cost production or scale advantages. Extra points if the company is capital light.

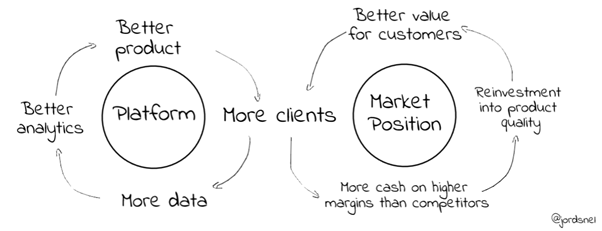

Presently, Cartrack has a network effect (shown in Figure 13 below). This effect kicks in when a platform (e.g. Airbnb) becomes more valuable the more both buyers and sellers are on it. As predictive analytics take centre stage in smart mobility trends, it is feasible that Cartrack would use their data flywheel to manufacture a pseudo-two-sided network effect where it becomes more valuable for Company X (the buyer of predictive analytics) to make use of Cartrack when Companies W, Y and Z all use it to (as “sellers” of the data necessary for the analysis).

The second component in Cartrack’s flywheel – the part that reinvests to further benefit customers – is similar to Nick Sleep’s Scale Economics Shared. It is an incredibly powerful cycle when a company has a cost advantage and looks to reinvest that cost advantage into the customer value proposition.

Cartrack is growing subscriber count, has a high “flow-through” margin on incremental subscribers, lower cost models than competitors (arguably because of their vertical integration and OEM agreements), and takes up only a fraction of their total market. It is likely they will be able to compound capital at high rates for the next decade.

Ecosystem shared value.

The final component of quality is the hardest to measure. It is the company’s emphasis on creating shared value for all constituents of its ecosystem. This encompasses inter alia ESG-metrics, social inclusion, societal value-add, employee education, ecological awareness, and supplier/consumer/employee surplus. In short, do they give more than they take away?

Companies that focus on such non-zero-sum thinking tend to create positive goodwill in their ecosystem – a trait which ultimately tends towards both longevity and improved shareholder returns.

We have hashed out already that Cartrack adds surplus value to consumers and OEM partners and given their vertical integration, they do not have as heavy a supplier dependence. Unfortunately, their employee churn does not suggest surplus value internally – despite the impressive employee education program described on page 27 of their 2020 IAR and positive feedback from interviewed employees.

Socially, they are active in several community outreach programmes and have 33% of the board previously disadvantaged and 33% female. They are not BBBEE certified. From an ecological perspective, their product leads to reduced travel distances, fuel consumption, maintenance costs and traffic congestion. They also use renewable energy to power their offices.

All considered, their product is fundamentally designed to make people safer and improve transportation efficiencies globally. This is admirable and for lack of a better word, good. Will this product make the world a better place a decade from now? Probably, yes.

So, Cartrack ticks most of the quality boxes in business resilience, management, moat and shared value creation, but will it grow?

Growth

Prediction is far more art than science, and all comments on future growth are a form of prediction. Insofar as determining growth is just a question of extrapolating the past into the future Cartrack looks set to grow revenue anywhere between 15-20% per year. Figure 14 shows their year-on-year growth rates, and Figure 15 their historical annualized growth rates. However, to quote Munger:

“It’s stupid the way people extrapolate the past – and not slightly stupid, but massively stupid”.

Speaking to the quality of growth, thus far it has been entirely organic, and management have indicated that they will continue to reinvest in organic initiatives. Further, because of the nature of vehicle tracking and the uniquely manufactured devices, there is no risk of multi-tenanting or multi-homing. Cartrack’s customers are likely exclusive and increase switching costs with time.

Another model to estimate growth would be to look at industry expectations as base-rates. Figure 16 below unpacks the expected growth rates of Cartrack’s various industries. As an average of these four industries, Cartrack would be expected to grow at roughly 22% per year.

| Current Global TAM (ZAR) | Est. Industry 5Y Growth Rate | Bibliography | |

| Data Engineering | 825 000 000 000 | 18.20% | Source |

| Analytics & Visualisation | 379 500 000 000 | 7.5% | Source |

| Telematics | 990 000 000 000 | 20.70% | Source |

| Artificial Intelligence | 643 500 000 000 | 42.20% | Source |

A third model for growth expectations would be a TAM analysis. Given Mix Telematics estimate of a $90B total addressable market for commercial vehicles, Cartrack (with its roughly $140M in revenue) currently has 0.15% of the TAM and between 2-5% of the already-penetrated market. If they can capture between 1-3% of the TAM within the decade, that is between a 21-36% CAGR in revenue.

In his recent excellent letter for ShawSpring Capital, Dennis Hong highlights the importance of trying to be accurate when underwriting the future. Rather than viewing additional growth prospects as a “free option” and pricing it downwards, he suggests that it is in this activity when investors deal most with the opacity of the world where they are most likely to gain an advantage over the market.

So, to try and price these prospects we’d look at where they are in their S-curve, whether they operate in a world of increasing or decreasing returns, what feedback loops are in place to spur and govern growth, what a steady-state might look like and what kind of optionality is present in their business model. To follow these up, we can filter them through some rough prediction heuristics and base-rates and see if there are any catalysts on the horizon.

S-curve progression

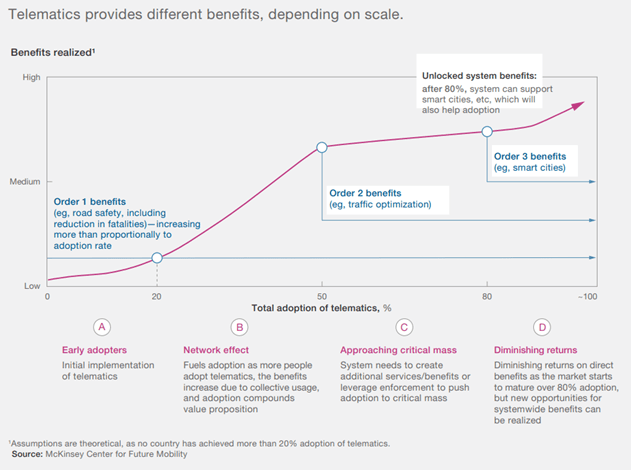

In a 2016 article, McKinsey outlined an expected S-curve for telematics adoption (Figure 17). Since even the most mature countries hover around the 30% telematics adoption mark, the expectations are theoretical if plausible. This kind of growth would scale the TAM rapidly, benefiting Cartrack disproportionately given its market-leading status. Cartrack’s SaaS model makes them scalable enough to capitalize on adoption as it occurs – they have a track record of scaling in the SA market as it has matured and are in the process of doing the same in their global markets.

On estimation, Cartrack is likely on the maturing end of their South African market S-curve (despite the 24% growth that market saw in 2020) and is beginning their global expansion S-curve (Asia-Pacific and the Middle East grew at 40% during 2020).

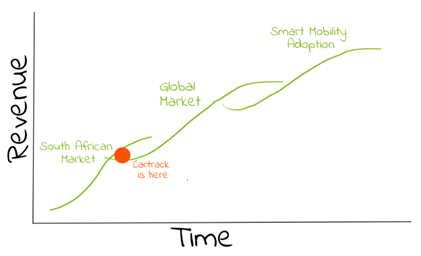

It is possible that post-global expansion, the markets will begin to mature, trending increasingly towards smart mobility and predictive analytics. This could stack a third S-curve in a demand for Cartrack’s higher end services (Figure 18).

In his 1996 Harvard Business Review article, W. B. Arthur contrasts the capital-intensive world of the early 1900s wherein he believes our concept of diminishing marginal returns originated, with the modern knowledge-driven, low marginal cost, networked world. His argument is that companies operating in the latter should optimize for adaptability and innovation. In a winner-take-most world, the best positioned are most likely the winners. Per Arthur, these winners are networked into an ecology, have access to abundant resources, understand the upcoming industry trends and the feedback loops that govern the market.

Cartrack’s cash generative base in South Africa give them capital and their R&D headquarters in Singapore open them up to top talent (who are drawn by both the growth and the massive data pools). Calisto has spoken frequently about capitalizing on the smart mobility and enhanced analytics movements, and their OEM agreement anchors them in the ecosystem better than many competitors.

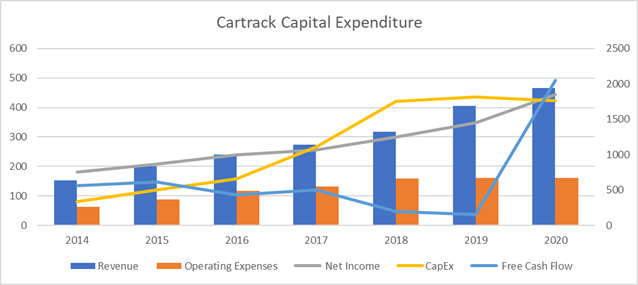

To effectively scale these S-curves, Cartrack needs to be able to reinvest the capital. Such reinvestment could take the form of R&D, increased marketing expenditure, new lines of product development or improving existing platforms/products. Figure 19 beside outlines the financials displaying Cartrack’s capital expenditure so far. The jump in FCF in 2020 was due to conservativism around COVID-19’s effect on supply chains. The current high level of Capex suggests a company aggressively reinvesting.

As far as feedback loops go, the positive flywheel in Figure 13 is one. Another positive would be the growth/talent attraction cycle. Because duration of growth is as important as speed, negative feedback loops – those which prevent hypergrowth – need to be in place too. For one, the switching costs inherent in Cartrack’s product (data captured) is similarly inherent in competitors. This makes taking market share from one another challenging and is one of the reasons why all companies are pushing for scale as much as possible. Another negative feedback loop would be the inability of lower-management to quickly implement a company-wide adoption of a telematics provider. Because it requires senior go-ahead, there is an added layer of switching costs.

A quick word on a steady state for Cartrack: assuming the s-curves in Figure 18 are vaguely accurate, we can expect three periods of heavy expansion before the company’s cash margins return to what they were in 2020 (roughly 25% FCF). One can assume Cartrack will not pay much of a dividend during this period. Figure 20 beside outlines potential financials for a hypothetical steady-state.

Optionality

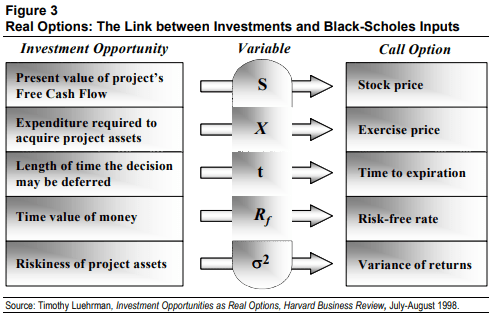

In their recent Hayden Capital and ShawSpring letters, Fred Liu and Dennis Hong both unpacked frameworks for understanding optionality. Liu references a 1999 Mauboussin whitepaper which analogizes thinking about option pricing under the Black-Scholes model to the way investors can think about real options that certain businesses carry.

An example of this type of real option would be investing in projects which enable rapid scaling of supply should demand surge. In this instance the firm with the option to scale would likely capture more of the surge than competitors, increasing market share off something that originally looked redundant.

These options are made valuable when companies have an aligned, smart, and long-term-thinking management team, when companies are market leaders and innovators, and when the future is uncertain and volatile.

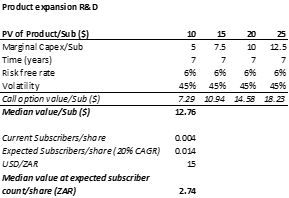

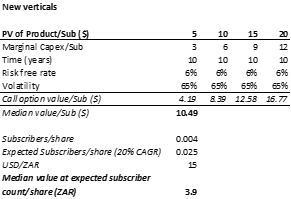

Liu and Mauboussin suggest an accurate business valuation should include a regular DCF model, plus a portfolio of these options. Figure 21 outlines the Black-Scholes analogy, while Figure 22 provides practical examples of the thinking model.

The irony that this paper was written in 1999 is not lost on me. By orthodox measures, one could understandably write off Cartrack as too pricey and its optionality as a misguided means to justify the present valuation. Perhaps, but I find value in applying Mauboussin’s thinking.

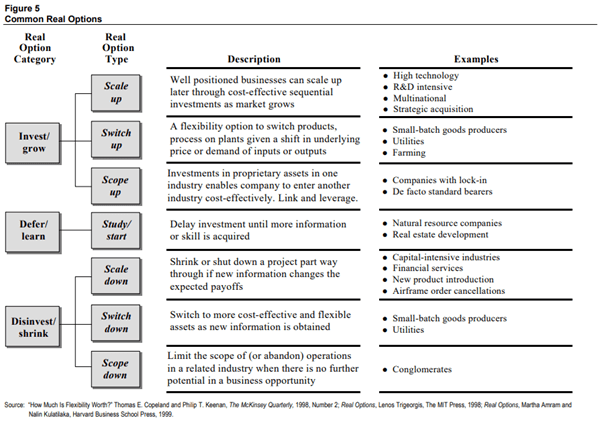

Using Liu/Mauboussin’s examples (Figure 22), Cartrack is well suited to both scaling and scoping up. Their investment into R&D ensures they capitalize on as much market growth as possible, and the ecosystem they are creating allows them to link-and-leverage their existing product range into both horizontal markets (such as their expansion from Fleet Management to Mi Fleet & Communicator) and vertical markets (like their Insurance Telematics offerings).

In Dennis Hong’s letter, he provides a similarly premised framework to Liu and Mauboussin. Hong identifies four types of optionality:

- New Business/Business (think Amazon or JD.com forming epic logistics businesses after leveraging the logistics demand of their ecommerce businesses).

- Product/Category Expansion (a good case study would be Tinder adding a “Boost” function to its core app – this often trends to expansion in new verticals).

- Strategic Shift/Evolution (ala Adobe’s shift from an on-premises model to a SaaS one – this has a superior customer value proposition and allows better unit economics).

- Geographic expansion (for example, Starbucks’ expansion into international markets – occasionally businesses are expected to grow linearly in local geographies, but their entering and scaling in international markets is unconsidered by the market).

Even in a semi-efficient market, these types of optionality are likely to be priced in relatively quickly given the speed of information flow today. Typically – per Hong – it requires a structural impediment for the market to not price these effectively. These can come through opaque disclosure (Amazon’s financials pre-separation of AWS), through an under-monetized asset blurring earnings power (Match Group’s Tinder) or poor current unit economics during the scaling process (Sea Limited’s financials while Shopee was young).

Cartrack certainly carries optionality in geographic expansion and likely too in the ability to expand into idiosyncratic higher-margin or disruptive offerings. This expansion would be unique because there would be no competitors with the data on Cartrack’s customers. Again, the more quality data points Cartrack gathers, the more possible the idiosyncratic offerings become.

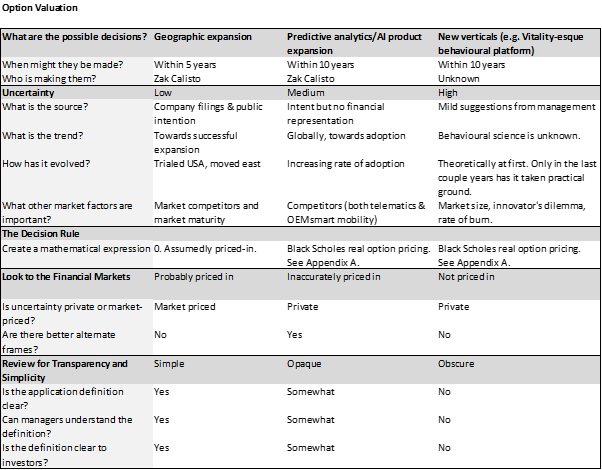

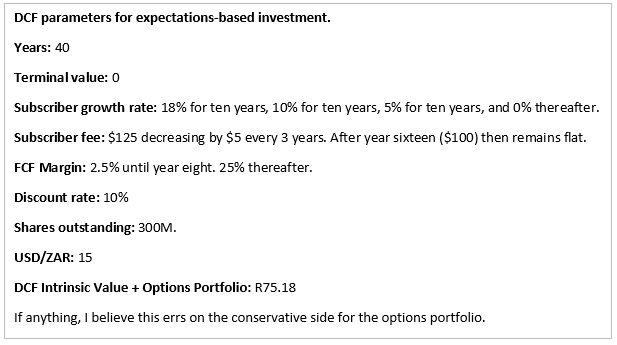

Now, Cartrack has arguably blurry financials as their reporting is not segmented by product sales, and its feasible their unit economics will improve as they scale. However, neither of these hold much water as structural impediments, so it is hard to imagine why Cartrack would be mispriced and/or provide a buying opportunity. As a thought exercise, a simple DCF of Cartrack an intrinsic value of R69.54/share. One could think of a range of potential real options available to Cartrack (Figure 23 is an example). Adding the value of the portfolio of options (roughly derived using Mauboussin’s real options approach), less a 15% leakage (hidden costs et al.) lands one with an intrinsic value per share around R75.18.[3]

Obviously, this is needlessly precise and likely inaccurate, but it gives you an idea of the kind of expectations baked into Cartrack and separates those expectations into linear growth and optionality.

Forecasting

Speculation around optionality, S-curves and linear growth are well and good, but how understandable is the company? How many predictions and what kind of predictions is the valuation forcing investors to make?

Broadly, there are three types of predictions: those focused on determining truth, those on optimising for a certain impact, and those black-swan types which bet on unlikely events where the payout of being right is larger than the cumulative cost of being wrong multiple times. Armchair investor estimations about Cartrack’s growth fall exclusively into the first category.

Predictions in the first category should avoid speaking in absolutes and should weight simpler outcomes in favour of complex ones. It is also better to think in probabilities than in exact points. As mentioned, there are network effects inherent in Cartack’s business model, and there is a cumulative effect in industry maturation, progress in AI and data analytics across the board and Cartrack’s specific growth. Because of these, predictions should consider the possibility of exponential growth (if Cartrack is market leader) or decay (if they are not).

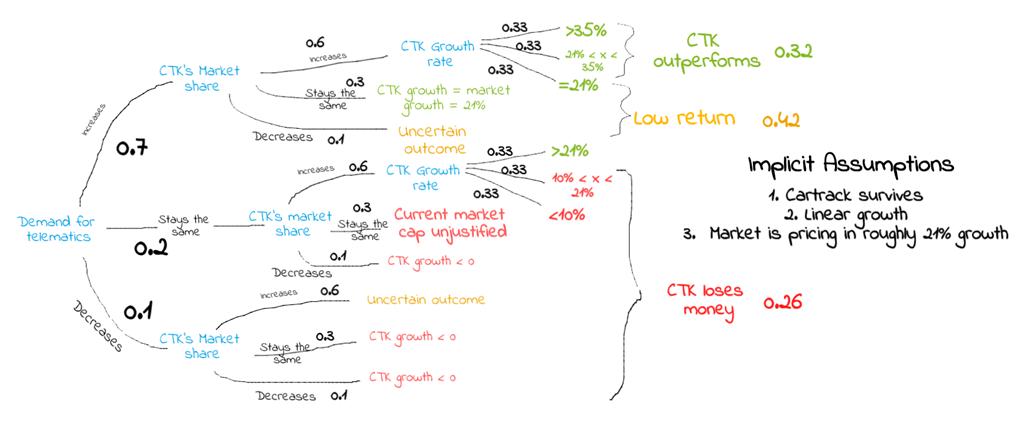

Because of their recurrent revenue, low churn, and strong customer stickiness, one can expect revenue to be pretty consistent. Therefore, the outcome of Cartrack’s growth less optionality is a factor of the demand for telematics broadly and Cartrack’s ability to take market share from competitors. Roughly, this plays into a probability tree that looks something like Figure 24.

The magnitude of outperformance would be significant, given that it’d likely include an instance of exponential growth. Further, the “low return” outcome is questionable. Outcomes in the “low return” category are those where you’re paying full fair value for the company. In this instance, you limit the upside to returns from ROIC. These returns may be entirely satisfactory. Another quote from Munger:

“Over the long term, it’s hard for a stock to earn a much better return that the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you’re not going to make much different than a six percent return – even if you originally buy it at a huge discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay an expensive looking price, you’ll end up with one hell of a result.”

Having weathered a global pandemic and the supply chain disruptions it caused, it is challenging to think of a scenario which would blow up Cartrack. They are not levered to the money supply, nor the interest rates. Smart logistics would be required in wartime and they are not overly affected by a shock in any commodity pricing. Their offshore expansion lessens their susceptibility to natural disasters, political risk, and currency fluctuations. One thing which would damage them would be a solar flare EMP, but the world would likely have bigger problems then.

As the bulk of their clients are in logistics, disruptions to global supply chains would trickle down to Cartrack, but because they are mission-critical in many instances, they are likely to be one of the last costs cut by clients.

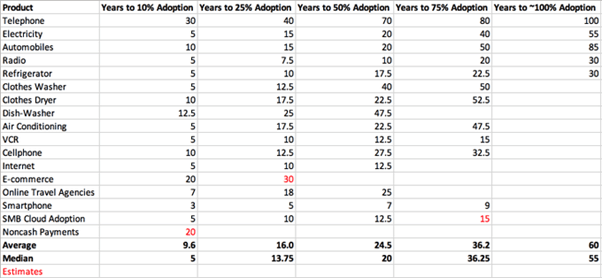

In terms of a timeline for predictions, Figure 25 has a set of years taken to X% adoption for various technologies. Using the medians as base rates, and assuming telematics is roughly at 25% market adoption, we can infer it will take another 7-10 or so years before it reaches 50% adoption.

To capitalize on this adoption rate and grow at rates of outperformance, Cartrack’s management should continue what they are doing: reinvesting heavily in R&D and marketing, focusing on offshore expansion in ex-US markets and facilitate room for tinkering and market-testing new products into both alternate and existing client bases.

Should management continue this, then over the next 7-10 years, Cartrack is expected to grow at a faster-than-industry rate, taking shares from competitors with a roughly 32% probability. This would likely lead to an exponential payoff, even from the current valuation.

Counterweights

Counterweights are the various factors to keep in mind when betting on a company. They include the valuation, various risks – both to the thesis and the company, and some biases and mental models to check the bet against.

Valuation

Beginning with the valuation, much has been said already: Appendix A outlines the DCF + options portfolio valuation mentioned above and Figure 1 in the beginning shows the outcome of a DCF model using different growth and discount rates.

Citizens of Graham and Doddsville will balk at the 8x Sales or 31 P/FCF multiples, and admittedly they make me skittish. However, two pragmatic contestations on the multiples: firstly, it is likely that international expansion and the heavy marketing spend are artificially suppressing present earnings to benefit the long run vitality of the company. Secondly, multiple-driven valuation implicitly extrapolates the future linearly. This is great for stalwarts and steady-growers but underestimates the optionality and non-linear progression that companies early on in their S-curve experience. Regarding multiples, I would contest that at PEG multiple of 1.56 (during a global pandemic which “severely disrupted operations” and limited growth to a mere 20%) is actually a fair price for a business of Cartrack’s quality.

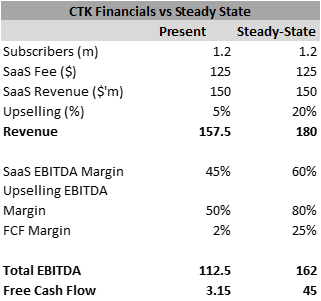

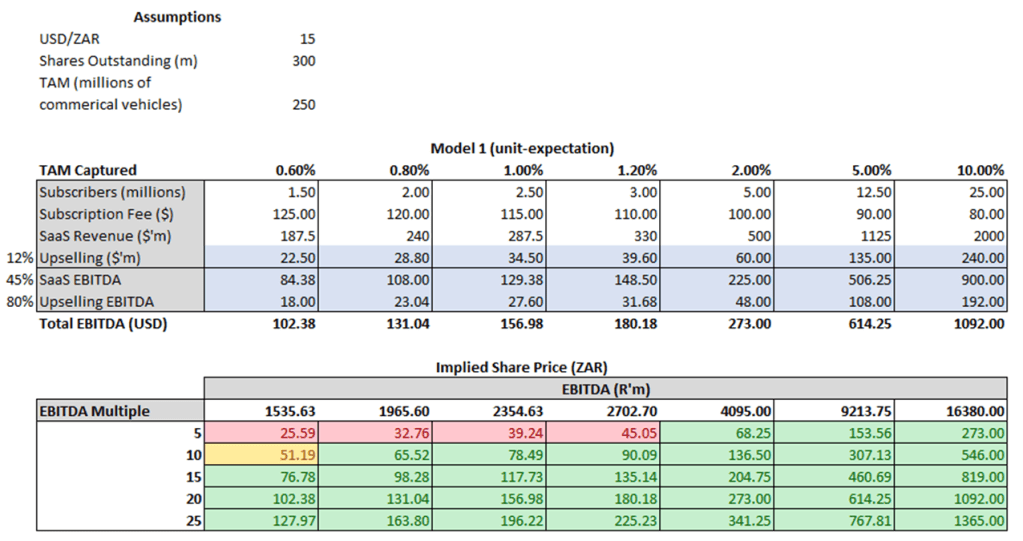

Figure 26 below is a rough model of potential valuations for Cartrack. I have assumed a TAM of 250m commercial vehicles only, have modelled a decreasing subscription fee over time, and show the percentages for upselling ratio and the EBITDA margins used next to them. It is a very simple model but highlights the potential for Cartrack currently.

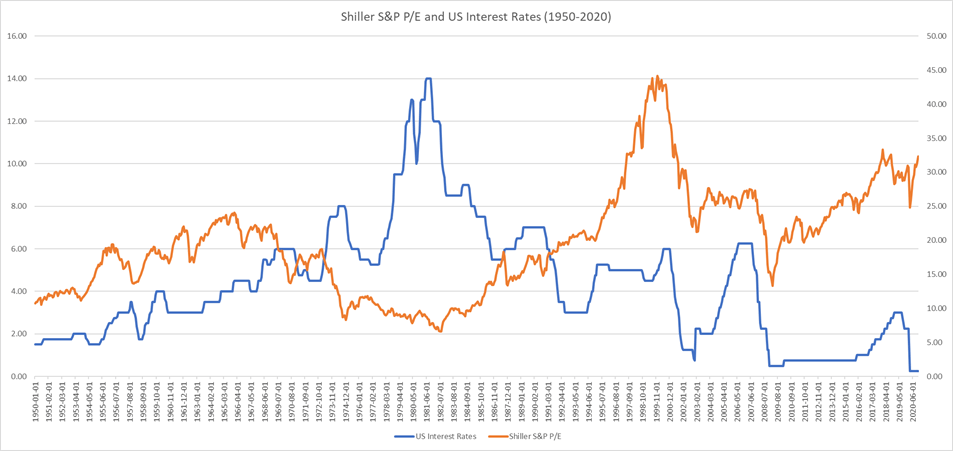

A further comment on valuation. In the DCF in Appendix A, I have used a 10% discount rate. Cartrack has a WACC of 11.28. South Africa has a 10-year government bond yielding 8.8%. The US yields roughly 1.1% and has interest rates near all-time lows (Figure 27). At these rates, it would not be hard to argue for a substantially lower discount rate. I have refrained from this for conservatism sake.

One crucial element of valuation is the “margin of safety”. Is one buying at a price substantially below intrinsic value, enough to buffer one from misjudgement and luck’s battering? This is not a paper about portfolio construction or investment methodology. However, it should be noted that Benjamin Graham’s definition of the margin was purely price-based, and he would sell once companies were 50% up or more. The Buffett-Munger definition is a little more fluid, factoring for future growth and business ROIC.

In NZS Capital’s paper Redefining “Margin of Safety”, they make the argument that nimble and adaptive companies offer investors a wider margin of safety through giving management more buffer-time to adapt to industry changes and avoid future pitfalls. They suggest that managers running slow-growth, long-duration businesses with decentralized and innovative cultures are able to stack S-curves well over long periods of time, compounding shareholder value.

They juxtapose this with hypergrowth, short-product-cycle businesses like Groupon or FitBit who often end up being one-hit wonders because management do not have the time to adapt. This adaptive ability and time-buffer acts as a margin of safety for investors in quality companies.

So, what should be considered a margin of safety in Cartrack’s instance? They are high quality, innovative, slow-growth and long-duration and have good management. They do not appear decentralized and their price is about as far from a net-net cigar butt as possible.

The honest answer is I do not know. I am comfortable with the risk-reward of its current pricing, and believe the company is closer to fair value than over- or under-valued. As such, holding a wonderful and growing company at a fair price is more rational than attempting to “call the top” in hope of a pullback and repurchase.

Risks

Outside of the valuation, there are several key business risks for Cartrack and investors. Foremost is the competitive risk of others having improved telematics solutions. There is also the culture risk discussed earlier, and the potential for regulation surrounding data ownership. Further, Zak Calisto poses a key-man risk, both as a majority shareholder and as a dominant founder-operator.

Prior to the NASDAQ listing announcement, a major risk was a privatization from management or an international private equity firm as the company was under cautionary. With the listing however, this risk has dwindled substantially and may be one of the reasons for the recent price surge.

Competitively, although discussed above, Cartrack does face some already-scaled peers. Per South African CEO Andre Ittman, in September 2016, Cartrack entered the US market with hopes of expansion. In other countries, their plug-and-play process of setting up their tech platforms has been with cellphone towers as a communication backbone. In the US, cellphone operating systems vary from state-to-state, which prompted Cartrack to look to Eastern markets for expansion instead.

Mix Telematics, however, has been focussed on the US market from as far back as 2013, and have seen substantial growth and infrastructure establishment there. Mix’ focus is on the large logistics fleets of developed market economies, and they have scaled to roughly 800K subscribers. There are several competitors (mentioned above) who are at similar scale and most are aggressively pursuing data accumulation. The risk to Cartrack here is that:

- a competitor is able to offer better products due to better data and gains the competitive AI advantage, and

- that they are locked out of the US market by the flywheel caused by (1), cutting off a large potential growth node.

A second risk is the potential for changes in data ownership legislature. Humans have had thousands of years evolving regulation of traditional assets, but data is relatively recent. It is a non-zero possibility that data is increasingly regulated over the coming decades. In this case the nature of the regulation – unknowable right now, but likely more stringent on ownership – could affect the thesis for Cartrack negatively.

The final notable risk is the incentive for Tier 1 suppliers to OEMs to install telematics devices in the production line. This is likely to have a cost advantage over an aftermarket installer, and they would be able to white label a product which they could use to sell data in a SaaS model to an aftermarket integrator. Despite Cartrack being the lowest cost provider amongst telematics peers, they would likely be unable to compete with Tier 1s.

Importantly, it would be tough to imagine the OEMs doing this, as they already receive the benefits of tracking their customers without having to put extra funds into R&D or maintain a complex online and offline system. Their model is high-volume manufacturing. Besides, fleet managers require a brand-agnostic data system, something only Tier 1s or aftermarket integrators could do.

The probability of this is complicated by several barriers. Firstly, Tier 1s usually have tight relationships with one or two major OEMs and arms-length relationships with others. Secondly, it would be tough for the Tier 1 to capture related revenue on telematics for servicing or insurance-premium savings. Hence, the risk is not that Cartrack is replaceable by OEMs or even Tier 1s, but that Cartrack has to shift their model away from using their own installed devices and towards leveraging off Tier 1 devices. This would likely benefit software-only competitors while harming Cartrack who built their business around vertical integration.

When a time comes that all consumer cars require telematics capabilities, or the commercial market matures to a point where Tier 1s become interested, then the risk will come to the fore. Until then, Cartrack has the time and first-mover advantage and may be able to solidify its position in preparation.

Biases and Mental Models.

It always helps to check for biases and filter an idea through several mental models.

For this piece, as the author I am subject to several biases:

- Self-interested bias: I am already long CTK, so it is in my interest to write a strong bull case. I try to counter this by publicising my work openly for criticism.

- Saliency bias: The work of many US tech investors and the market performance of US SaaS companies may be over-influencing my thinking. I have tried to counter this through making explicit the assumptions in my writing and by thorough ad hoc analysis.

- Confirmation and availability biases: Being long, I may look for sources which promote the upside. To temper this, I write out the risks, force a biases checklist and can review writing more objectively when others criticise it.

- Anchoring bias: I began buying CTK around R18. I am also used to South African companies trading around 9x Price/Earnings. These anchor me to a lower valuation than may be accurate.

- Halo effect: Calisto has been successful with Cartrack; I may be overestimating his and his management team’s capacity to innovate further and introduce new products. I hope to counter this through transparency around potential shortcomings.

- Competitor and disaster neglect: It is possible that the worst-case scenario is not adequately worst-case. Having written about the competitors and disaster possibilities above, I am confident in Cartrack, but may have underestimated the black swan probability.

There are several others, but these are the most prominent. In 2016, Mauboussin et al. published a fantastic “base rates book” which investors can use to lay over their thinking in an effort to improve accuracy of forecasting and rely more on the rates of past occurrences (the “outside view”). The data below comes from this book.

Historically, only 18% companies of Cartrack’s size able to compound sales at >20% for 10 years. The average for companies that size is 12% sales CAGR over 10 years. The book does note that companies in the tech sector have far lower correlation coefficients to industry means than other industries. This is likely because of the network effects that tech companies often carry – it is a more “winner-take-all” world.

The average gross profit margin for companies in the information technology sector is 42%, down from Cartrack’s 71% and an average operating profit margin of 15%, down from Cartrack’s 33%. Again however, the companies on top in this sector tend to remain there, increasing their lead year on year.

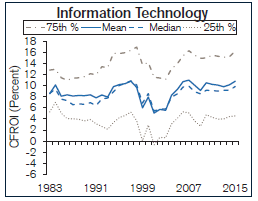

For cash flow return on investment (CFROI), companies in the information technology sector trend towards an average of 9% with a distribution shown in Figure 28 beside.

The purpose of these is to give pause and reflection on the assumptions used in all the models and growth expectations mentioned above. Cartrack is well above the 75th percentile in all instances. There is the possibility of mean reversion here, however there is also the possibility of sustained dominance and outperformance – the rich get richer.

A final component of this brief self-check procedure: what could kill the company? What is it fragile to?

From my perspective, of all the risks spoken about above, the key-man risk in Calisto is one of the biggest. As the owner-founder-operator, Calisto is to Cartrack what Bezos is to Amazon. He is a great capital allocator, highly customer-focused and at 50 and having several previously successful businesses under his belt, his contribution to Cartrack cannot be overstated. God forbid any harm befall him but were it to, Cartrack would probably not be the same company.

Another thing that could potentially kill the business is a disgruntled employee base. Because so much of the businesses market leadership depends on maintaining an innovative lead, Cartrack needs to make sure they keep tacit IP within the business. While employee churn is low amongst key employees, it is relatively high amongst the less-key ones. The company is aware of this and puts a lot of money and attention into funding extra studies, fostering growth and career development, and high-quality recruitment.

The first of these risks is subject more to vicissitudes than the second, and the company is addressing the second well. The quote “culture eats strategy for breakfast” rings true often enough to take it seriously. As a part-owner in the business, I am looking forward to watching Cartrack’s culture thrive as the company grows in time.

Conclusion

Cartrack is the security I like best. In 2021’s global market, finding a profitable company with as strong growth prospects as Cartrack trading for fair value or below is all but impossible. Most high-quality companies with strong tailwinds and long investment runways are trading at wild multiples. I wrote in May of 2020 that I believe Cartrack will be a 10-bagger from the then-valuation of R6.6 billion. I hold to that now and can see the company compounding for many years from here yet.

Typically, a conclusion contains a summary. But this has been a long article and the Explain Like I’m Five segment satisfies the need for summation.

Lastly, I owe a very big thank you to perspicar744 on ValueInvestorsClub for the wonderful 2019 writeup, Rudi van Niekerk for the original idea on MOI, both of their work has greatly influenced mine, and I recommend you read theirs ASAP. Further, a massive thanks to David Eborall, Aheesh Singh and Dede Eyesan for teaching me stacks about this company and investment strategy throughout many conversations.

Investing is a game of competitive learning. I put these reports out to learn in public and have been blown away by the amount of much smarter people than I who have reached out and shared their time with me. If you have any questions, comments, or criticism of this thesis – I would genuinely love to hear it. You can reach me on twitter or at jordsnel@vineyardholdings.net.

Appendix A

Appendix B

Questions for Cartrack’s management:

- What is the succession plan for Zak Calisto?

- Are newer cohorts retaining better on a dollar basis, for every given time period, than older cohorts?

- Is your user retention improving for newer cohorts?

- What is the upselling percentage? Are subscribers becoming more engaged in the ecosystem over time?

- Are participants in the oldest markets — for businesses with local network effects — better retained, than those in newer markets?

Appendix C

Sources for interested further readers:

- Creating IoT ecosystems in transportation – Deloitte

- Overcoming speed bumps on the road to telematics – Deloitte

- Insurance telematics: A game-changing opportunity for the industry – Accenture

- Telematics extend ‘co-opetition’ to keep wheels of industry turning – Alex Howlett, FT

- Big Data in Logistics – DHL

- Automation in Logistics: Big opportunity, bigger uncertainty – McKinsey & Company

- Fast and Furious: Riding the next growth wave of logistics in India and China – McKinsey & Company

- Telematics: Poised for Strong Global Growth – McKinsey & Company

- Telematics in Auto Insurance – towardsdatascience.com

- The Dynamics of Network Effects – Li Jin

[1] MiX Telematics Integrated Annual Report 2020.

[2] Mordor Intelligence Report, Telematics Market (2020).

[3] For those interested, the assumptions & figures used in the model (DCF & Black Scholes) are in Appendix A.

How do you compare them to Ituran form Israel?

LikeLike