Disclaimer: I have written an updated and revised version of this article here. Please read that instead. The article below does not do a great job at valuation, it is not well structured and I do not agree anymore with either the applications of the Monte Carlo simulation nor the Kelly formula.

I read recently in a report by Rudi van Niekerk that Cartrack (CTK), a South African global provider of telematics (they put chips in cars to track them and then sell the tracking service on a subscription basis), was a “wonderful business”. Much of my research stands on his shoulders, and I owe him enormous thanks for bringing the business to my attention.

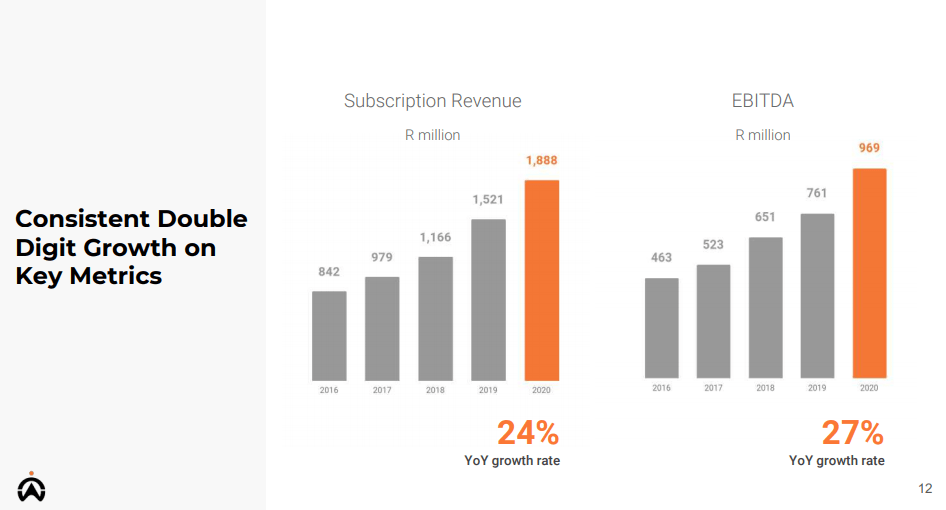

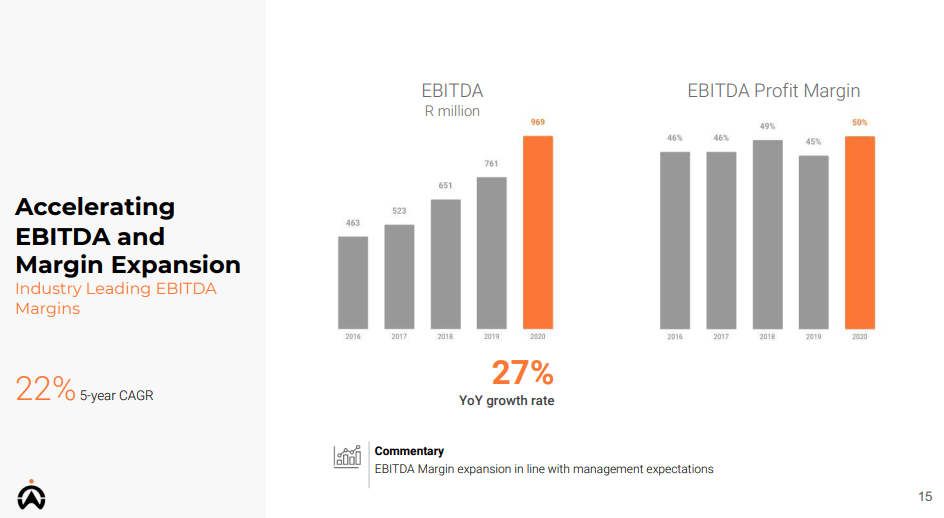

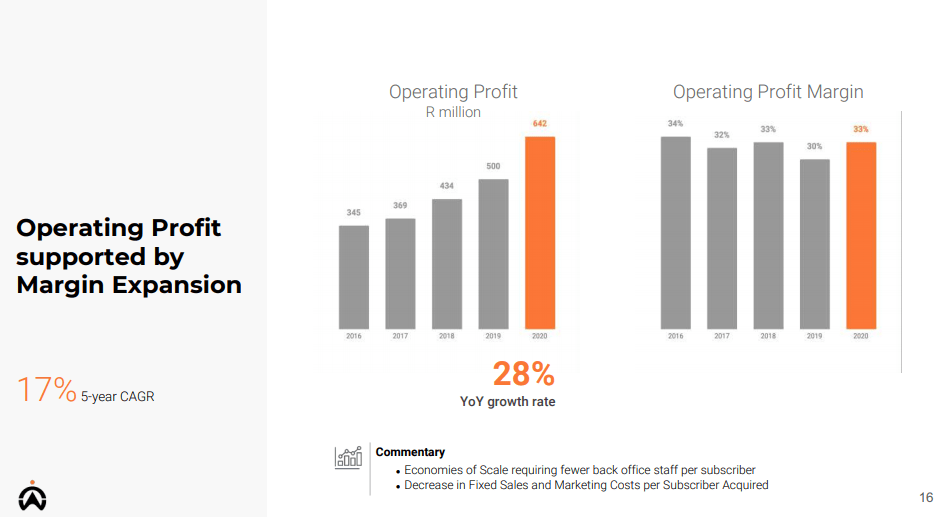

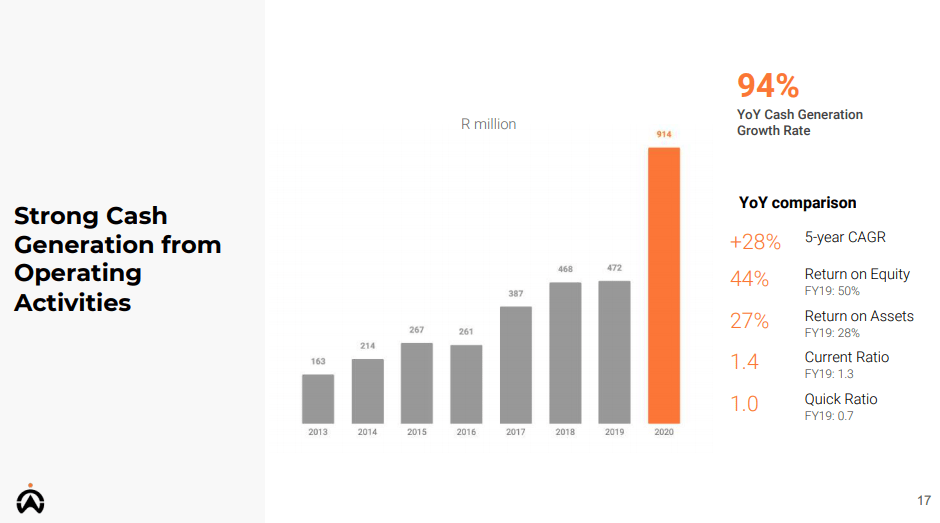

At first glance Cartrack does seem to boast some very impressive results, here are the growth measurements shown in their most recent results presentation, taken directly as the data presented is quite staggering.

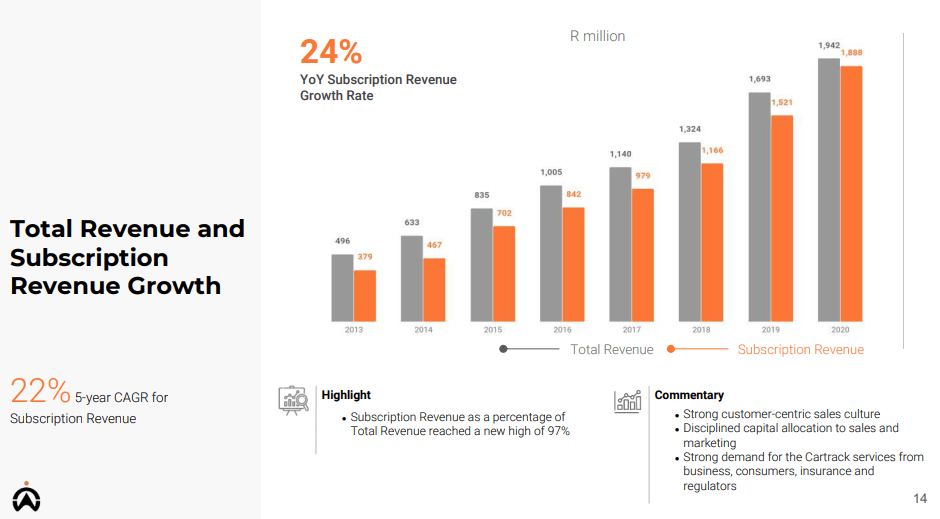

- Subscription Revenue: 24% YoY growth rate; 22% 5-year CAGR.

- EBITDA: 27% YoY growth rate; 50% margin.

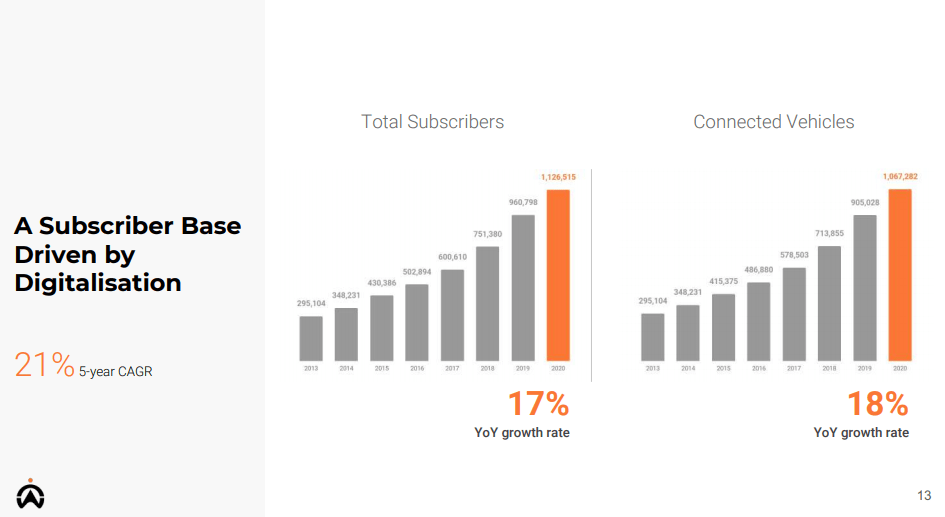

- Total Subscribers: 21% 5-year CAGR; 17% YoY growth rate.

- Operating Profit: 17% 5-year CAGR; 28% YoY growth rate; 33% margin.

- 94% increase in Operating Cash Flow on the back of 28% growth in Operating Profit and tight capital management.

- 28% 5-year total CAGR.

- 44% ROE.

- 27% ROA.

- 1.4 Current Ratio.

- 1.0 Quick Ratio.

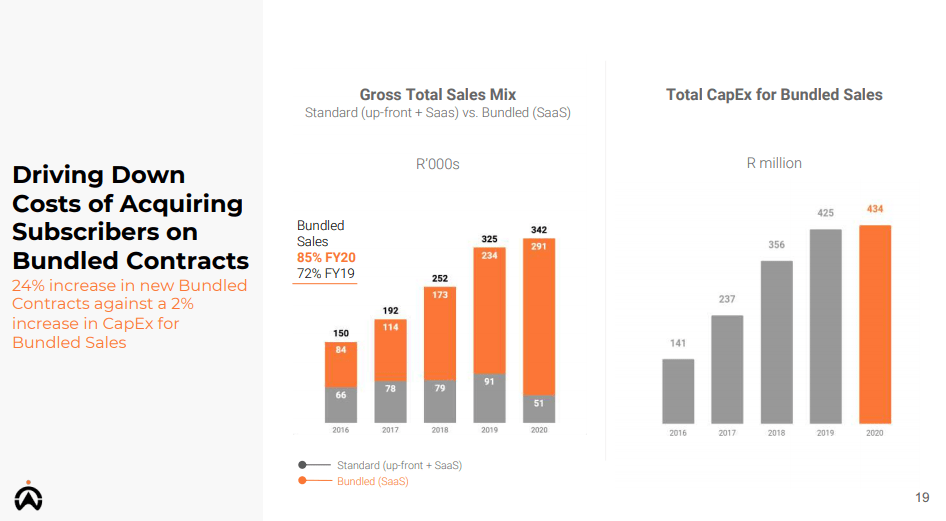

- 24% increase in new Bundled Contracts against a 2% increase in CapEx for Bundled Sales. This is indicative of decreasing costs affiliated with acquiring subscribers – the beginnings of economies of scale and improving global footprint.

- 18% EPS 5-year CAGR since listing.

- 147% increase in Full Year Dividend on the back of strong Free Cash Flow and improved Earnings.

I mean, these are shockingly good results which certainly warrant further investigation.

For those of you not familiar with it, Cartrack is a JSE-listed, global Stolen Vehicle Recovery “SVR” and SaaS Telematics business. While based in South Africa, it is a globally operative company with a growing footprint in 23 countries across 5 different continents. It is fully vertically integrated with protected in-house technology that provides vehicle owners with intelligent, real-time, actionable data. Think along the lines of solutions that include vehicle tracking, stolen vehicle recovery, vehicle maintenance optimization, vehicle camera systems, insurance driver behaviour scorecards, cost management and accounting software, etc.

The management is superb with the founder-operator owning 68% of the company and other management owning a further 12%. This ensures “skin-in-the-game” as management seek to maximise shareholder returns. Zak carries with him much of the start-up mentality that owner-founders enjoy and – despite the impressive growth shown thus far – still believes that the company is in its early stages of growth. I personally enjoy the low leverage approach that Cartrack has taken in choosing to repay debt as quickly as possible and grow through organic reinvestment instead of debt-laden acquisitions or heavy financing.

The market in which Cartrack operates is a “winner-take-all” market. The total telematic market is expected to grow to $750 billion by 2030 and has been characterized largely by the dominant firms growing through acquisition. As mentioned, Cartrack is one for the few globally dominant operators to have grown organically ensuring cohesive cultural identity and proving it’s operating model. Primary drivers in the telematics industry include increased global connectivity (particularly the decreasing data costs across Africa), regulation (the increased prevalence of governmental and insurance agencies mandating vehicle tracking) and adoption as more and more companies realize the cost benefits of telematic services. The reason this market is considered “winner-take-all” is because of the high scalability and data-based intelligence that companies achieve as they grow: the more customers you have, the more data you gather, the more intelligent and accurate your services.

When reading the latest investor presentation linked above, pay special attention to the global growth that Cartrack is achieving. Per Rudi van Niekerk:

“Europe and Asia Pacific are the two priority global growth areas. For the most recent reporting period, Cartrack’s European EBITDA increased 98% and Asia Pacific’s EBITDA grew 139%.

In 2014, only 6% of revenue was generated outside SA. Over the last five years, global revenue has grown to contribute 27% to the total. The trend is accelerating and soon more than half of Cartrack’s revenue should be non-SA, global business. In the short term, we get the SA-listed valuation discount. In the long term, we get a great global company.”

As we can see, Cartrack is lining up to be a truly wonderful business. When considering the growth potential, superb management and the enjoyable economics of a company which has a predictable revenue stream and a very long runway, it is surprising to see it trading on a relatively humble Price/Earnings multiple of 16 and Price/Sales of below 4. The Price/Book ratio is a little less humble at nearly 6, however this is a little more understandable when considering the asset-light nature of a services provider. All in all, this is a little pricey for my cheap taste, but I am hard pressed to ignore the staggering numbers and wonderful economics of the business in favour of my frugality.

Now, in general, I tend to be more of an Excel guy than a Microsoft Word guy. Although I enjoy reading far more than accountancy, I find that – when arriving at decision-making – the numbers help to sway my opinions more convincingly than text. This, unfortunately, violates number 5 of Pabrai’s 10 Commandments of Investing: “Thou shall never use Excel”.

“The investment process is simple,” advises Pabrai “and you should not take help of an Excel sheet to figure out if something is a great investment. If you cannot figure it out in your head, it can’t be a great investment. If you find yourself reaching for Excel, you take a pass”.

Nevertheless, I cannot help but reach for the little green X-shaped logo when wondering just how wonderful a company Cartrack might be.

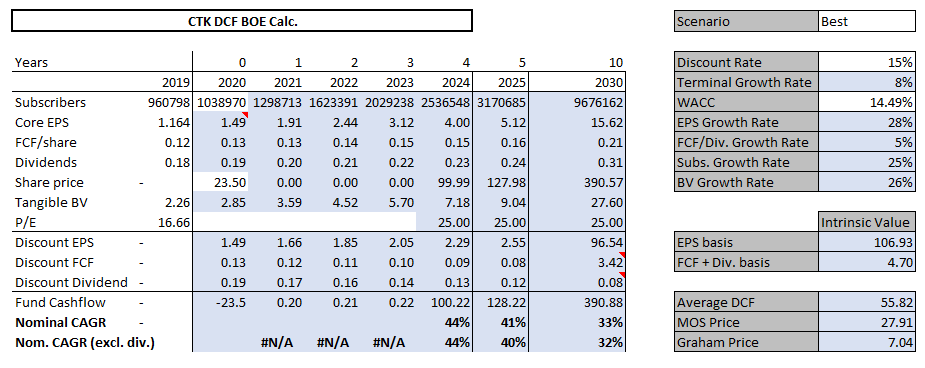

Using current growth rates as a best-case scenario, here is a quick projection for how well I believe the company can do. Note the assumptions used on the right and the estimated returns in bold.

In his book the Dhandho Investor, Pabrai gives examples of a simple “back of the envelope” Discount Cash Flow valuation model (such as above). I have applied this below for Cartrack’s expected earnings and have used a conservative exit Price/Earnings multiple in 2030 of 25.

Please note that the Free Cash Flow (FCF) basis for a DCF model is not entirely applicable in the case of Cartrack, given their heavy re-investment in PPE and consequently tighter free cash flow figure.

Best case scenario represents current growth (afforded 35% probability); Base case (55%) represents slightly depressed growth rates with and worst case (10%) includes a “lost” 2020 netting 0 income and severely lagging growth rates). I have assumed an unrealistically high discount rate and have used current WACC for estimates, despite the likely decrease in WACC that comes with economies of scale. Even in worst case scenario, we are only buying the stock at the admittedly upper range of its intrinsic value.

Given the above as a best case scenario, and running the two other similar scenarios (base and worst case respectively using even more conservative growth estimates) I estimate the intrinsic value for Cartrack to be anywhere between R34 per share to R92 per share. This represents approximately 50% upside at least to intrinsic value.

In Fortune’s Formula, William Poundstone outlines the use of the Kelly formula in determining optimal portfolio amounts to “bet” on investments, given their expected return. Using this formula yields the below percentage of the portfolio to place in Cartrack.

This is an exceptionally high amount, one with which I am a little uncomfortable. However, it does indicate how great of a “bet” this company would be.

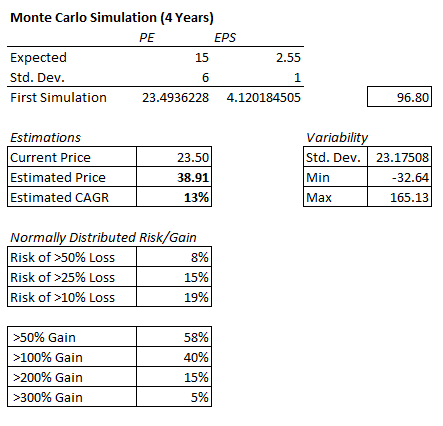

Running a Monte Carlo simulation on the above predictions yields the below results. I would like to highlight the simplicity of this model – it is a quick and very dirty rendition of what is usually a far more complex simulation method. Its use comes not in it’s accuracy, but in highlighting the potential for convex upside gain and disproportionate risk to reward offered in Cartrack.

In conclusion Cartack’s price tag positions it, while expensive relative to most SA-based mid-caps, definitely below intrinsic value. To summarize, Cartrack is a wonderful company (low debt, cash generative, strong growth) with a wide moat (data, switching costs), a predictable income (subscription based) and excellent management (high ROIC) who have skin in the game (80% insider ownership). It has lots of room still to grow, and while it may look expensive, it’s SA Inc. status and Mr. Market’s shock to COVID-19 have brought its share price to well below intrinsic value, even with very, very conservative estimations.

All in all, I expect this company to return between 25-40% CAGR for many years to come. I’m backing up the truck.

I’m very curious about how cost management and accounting software fit into this equation. I use accounting software, myself, and the translation isn’t immediately obvious to me. Thanks in advance!

LikeLiked by 1 person

Hi there, thanks for reading and commenting. Cost accounting software like Mi-Fleet (here https://www.cartrack.co.za/mi-fleet-administration) is Cartrack’s offering to customers that is intended to assist in calculating vehicle usage and the costs associated with it.

It syncs with the user’s internal system and will notify them whenever things like servicing are required. It will include key information such as cost per kilometre driven, cost per vehicle, and historic maintenance costs. The purpose of this is to avoid untimely servicing needs, as well as to calculate efficiencies on a cost-accounting basis.

LikeLike

Hi there, interested to know your thoughts on the proposed foreign takeover and how we might see this impact price going forward? Seems as though the proposal is being seriously considered and the company has again issued further cautionary announcements

LikeLike

Hi, thanks for the comment.

CTK’s management have recently started repurchasing their shares, perhaps in preparation for this deal. So, given the high multiples that growing SaaS companies trade at usually, I think that the takeover price is likely to be well above the share price. While I would rather hold the company for years, as it really is a wonderful company, the takeover bid is likely to generate a decent return.

My worry is thus not so much about the ROI for my CTK holdings, but – as suggested by the SENS – the shares that will be exchanged for them by the purchasing company. I don’t know who this company is and that threatens the investment thesis for the long run.

All considered though, as shareholders currently, we have optionality here: if we like the bidding company, we can hold the shares while the price difference between the merger price and the existing share price is arbitraged away, thus realizing value, and sell before the merger. Alternatively, if we like the company (and, being Singaporean, it may have decent macro tailwinds) we may hold on and get access to an international company at the price we paid for CTK’s SA Inc. shares.

LikeLike