The year is circa 935 BC and The Teacher lifts his gristly hand to reach for his quill once again. Dabbing it in the inkwell, he traces it across the page with the well-hewn motions of a man altogether weary of such practice. There is nothing new under the sun he writes, careful not to smudge the paper. This is to be his last letter – a memoir to a life lived at the musty altar of thought and knowledge.

Little did he know it, but those words would be repeated ad infinitum by generations of scholars and laymen alike in the millennia to come. As they have in many other times, these words will find a home in the future of a young, highly successful businessman from Mumbai, India.

A late bloomer, Mohnish Pabrai only began investing around the age of 30, after reading a series of articles on first Peter Lynch, and then Warren Buffett. This is not to say he was inactive before then; after varsity he went directly into working at a technology company called Tellabs, which he worked at until at the age of 27, when he started an IT consulting firm funded with $30,000 from his retirement account and a maxed out credit card.

Ultimately, Pabrai sold the company in 2000 for $20 million – a compounded annual growth rate of around 80% – in the process proving to himself that he was most certainly cut out for life as an adept businessman. In 1999 Mohnish Pabrai founded the Pabrai Investment Funds, which he still runs today. To date, the fund has beaten the S&P by nearly 1100% over the course of its lifetime.

The reason why Pabrai is effectively the poster-boy for the Ecclesiastes 1:9 verse in the introduction is simple: he has made a very lucrative living, given away fortunes and impacted the lives of a great number of people (including that of yours truly) by doing absolutely nothing outside of the well-trodden path set before him by the likes of Warren Buffett, Charlie Munger and Peter Lynch.

As far as the US Securities Exchange Commission is concerned, Mohnish runs a concentrated, long-only portfolio of approximately 3-6 stocks, all listed equities, usually somewhat distressed, usually on what he likes to call “a hidden PE of 1” and usually with durable economic moats. Our understanding of Mohnish’s investing approach – derived mostly from his excellent book “The Dhandho Investor” – can be summed up in about 5 primary principles (all of which, while simple to write, are incredibly challenging to implement correctly):

- Copy, copy and copy some more.

- Invest in no-brainers. This is another way of saying “look for the stocks with a hidden PE of 1”. This means that these companies have income sources or assets that are not reflected in totality on the balance sheet figures most analysts will look at.

- Begin with distressed and neglected industries.

- Take big bets infrequently where the risk to reward ratio is overwhelmingly in your favour.Wall Street is handicapped against uncertainty but has little regard for true risk. Take advantage of this.

- Invest in businesses with durable moats; earning high returns on invested capital keeping in mind that most moats are hidden or in partial view and that there’s is no such thing as a permanent moat.

To unpack these, let’s take a dive into some of Pabrai’s previous purchases:

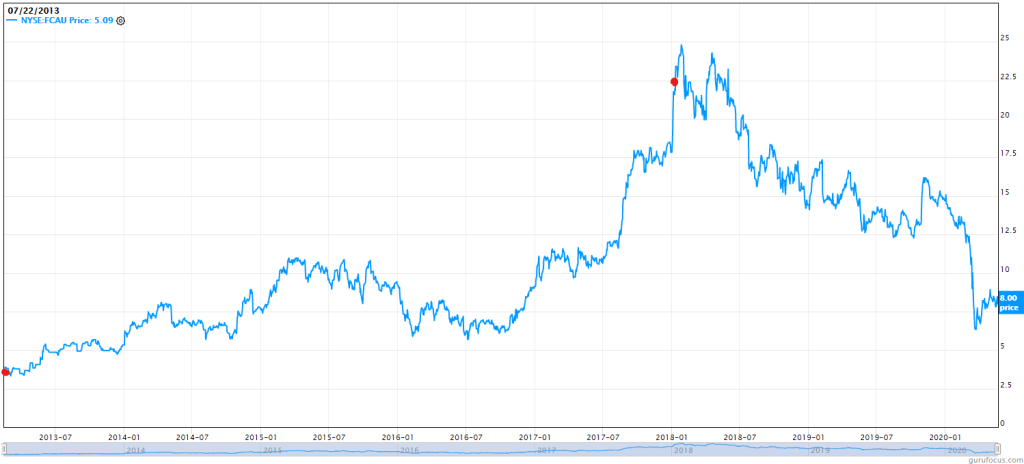

Pabrai began his research into Fiat-Chrysler (NYSE:FCAU), one of his current holdings, after studying David Einhorn – a hedge fund manager who had previously taken a position in General Motors (read copying). By and large, the auto industry is disliked by investors due to the high CapEx it necessitates, the strong levels of unionization it faces and the constantly changing nature of consumer demands. These factors lead to an industry based on the sale of products which are very costly to make and are subject to being rejected quickly (read neglected industry). This is not an industry with the bountiful margins investors typically dream of.

Mohnish found that in 2012, despite the unfavourable nature of the industry, FCAU was unlikely to go bust and its shares were trading at an average price of $4. At the time, the Earnings per Share were $2.22. This puts it at a PE of around 2.

While in most cases, Mr. Market’s appreciation of companies is reasonably accurate (consequently, most stocks on a PE of 2 are not worth touching with a ten-foot pole), there are the odd exceptions. In this case, it worked out that Mr. Market was not adequately factoring in Ferrari, the well-known subsidiary of FCAU comprising approximately 40% of the purchase value. If we deduct 40% of the 2012 purchase price as the value gotten from Ferrari, we get to a PE ratio close to 1. A clear no-brainer for those who have done the work researching.

In 2018, FCAU’s stock rose to around $23 per share. On top of that, we must add the Ferrari spin-off that has a market cap almost as big as FCAU. Double the gain there for Pabrai.

Another company Pabrai recently owned – but fully sold out of as of March 2020 – is Graftech International (NYSE:EAF). As all Pabrai investments, the company was a classic instance of how a little digging goes a long way.

Without expanding too much on the economics of the graphite electrode industry or Graftech’s role in it (Oliver Sung of Junto Investments has a superb article on it here for those who are interested), here is a quick overview of Graftech’s business:

They manufacture graphite electrodes – a scarce resource necessary in the fast-growing segment of steel manufacturing known as EAF (electric arc furnaces) manufacturing. Emerging countries (i.e. China) typically do not use this method but prefer to use traditional smelting methods – called BOF or basic oxygen furnacing – to manufacture steel. Given the benefits of EAF (greater resilience, a more variable cost structure, lower capital intensity, and more environmentally friendly nature), most manufacturers would ultimately like to switch to the EAF method. As such, China is aiming for 20% of its manufacturing (which constitutes 56% of the world supply) to be EAF within the next year. Since steel production is such a vital industry for China there is a big chance that the country would want to localize all links of production and limit imports.

The issue with this is that it is really complex and expensive to convert to the EAF method, especially given its dependence on a material known as petroleum needle coke – which China has in short supply. This has led to the only viable players in the game being those who already have the equipment and know-how necessary to make the needle coke. It has a huge barrier to entry… a moat.

As far as market awareness goes, companies manufacturing graphite electrodes are typically priced in relation to the demand for their product, which is in turn priced in relation to the demand for steel. When China shocked the steel supply (using BOF methods of manufacturing) in 2011-2015, this placed significant downward pressure on the price of GrafTech’s stock and also made the price of graphite electrodes exceptionally volatile.

Now, as for GrafTech itself – they manufacture approximately 25% of the world’s graphite electrodes outside of China and have deep integration with their customers by way of supply chains and logistics. Further, in terms of technical know-how, GrafTech’s business is complex, highly technical stuff depending on highly skilled technical and managerial personnel. This reinforces the large moat around the business in terms of locational advantage, a 130-year experience, proprietary know-how, trust, and quality.

Even more importantly however, GrafTech is the only vertically integrated supplier of graphite electrodes in the world. This is an astounding moat. GrafTech owns and operates one of the world’s only standalone petroleum needle coke plants – giving them an internal supply for approximately 70% of the needle coke they need.

As per Sung in his article mentioned above:

“This gives GrafTech a big competitive advantage since if a competitor goes bust due to a giant increase in the price of petroleum needle coke, it would decrease the supply of graphic electrodes, and GrafTech would take a greater share.

Furthermore, GrafTech’s uninterrupted, low-cost access to petroleum needle coke allows the company to operate a method of contracting that GrafTech as the only player in the industry can do.”

Oliver sung, junto investments

Combine this moat with the fact that GrafTech essentially secures income in advance through long-term contracts with it’s customers and you have a relatively predictable surety of what the company will earn, regardless of the market price of graphite electrodes.

Mr. Market however, prices GrafTech largely according to it’s disappointing financial results over the last 5 years (due primarily to the Chinese steel supply shock) and the big debt increase that management took on in 2018. This, combined with the perceived volatility in the pricing of graphite electrodes, makes many investors on Wall Street think the stock is much riskier than it actually is.

Pabrai capitalizes on Wall Street’s reticence, relaxed in his position, assured of the income the company will bring by both the forward contracts and its deep, technical, and vertically integrated moat. The depressed stock price suggests significant upside when the market ultimately recognises its misjudgement of the risk and in the meantime, Pabrai stands to lose very little of his investment given the aforementioned surety of his position. This is a perfect outplay of “heads I win, tails I don’t lose much” where the upside is drastically in his favour and the downside is minimal. Ultimately The GrafTech bet is one of probabilities and very simple math. If we understand the math and can accurately guess the probabilities, we can assess the risk-reward.

To recap quickly, Pabrai’s 5 key principles include:

- Copy shamelessly. (Pabrai copied Einhorn in the automobile space).

- Invest in no-brainers. (FCAU had a hidden PE of 1).

- Begin with distressed and neglected industries. (Both the automobile industry and the graphite electrode industry are disliked by investors).

- Bet big when the risk-reward is overwhelmingly in your favour. “Heads I win, tails I don’t lose much”. (both Pabrai’s bets on GrafTech and FCAU were stacked strongly in his favour with the price being so low and upside so high).

- Invest in businesses with durable moats. (Most moats are hidden, such as GrafTech’s exceptionally strong position due to future contracts and vertical integration).

Outside of these, there is still an immense amount the average investor has learn from Mohnish. Guy Spier does a fantastic job of sharing some of the lessons he has learned in his book “The Education of a Value Investor”. Much can be learned from Mohnish online through Youtube videos of his lectures and on his blog, chaiwithpabrai.com.

Hi Jordan have just found your website through your Tencent deep dive. Thank you for taking the time to write out these detailed articles. I am young investor with no formal education in financial markets so your analysis is very much appreciated.

keep up the good work, I look forward to reading more.

LikeLike