Foreword

This is the first of a long, three-part article. If you are interested and looking to invest into ARC, we recommend reading the whole thing. Should you be pressed for time, you can skim the bold sections and you will get the gist of it all. If your interest is merely cursory or a fleeting thought, then we would recommend the “Explain Like I’m Five” section of the summary above.

Overview

African Rainbow Capital Investments (JSE: AIL) is a holding company trading at a massive discount to the sum of its parts. This discount is somewhere around the estimated range of 50-70%.

As a rule of thumb, South African holding companies, whether they are PSG, Remgro, Naspers or ARC Investments (ARC), tend to trade at a discount of anywhere between 15-25% to their NAV. This is a far cry from the days gone by where conglomerates fetched premium prices due to investors jumping on the hype trains of word like “synergy” or “economies of scale”, suggesting that various businesses can work together and be worth more as a whole than as individual companies.

It is surprising however to see a holding company trading at such a staggering discount to what the management believe their assets are worth. As we shall see in the segment below on holding companies, either ARC’s accountants are significantly overestimating their underlying assets, or the market is missing something here.

This is Part 1 in a three-part series unpacking the investment potential of ARC, including some insights into the African market and a cheeky little exposition into the nature of valuing holding companies, courtesy of Professor Brian Kantor.

Part 1, this essay, will outline the investment thesis and explain a little about the nature of the company itself. Part 2 will provide a general comment on holding companies in South Africa and will act as a springboard for the arguments of Part 3. Part 3 will in turn attempt a back-of-the-envelope calculation valuing the major underlying holdings of ARC and will expand on their role in the African market at large.

Right, here we go: We are fundamentally value investors. It is not our job to speculate on market movements, predict macro-industry trends or try to “find the next big thing”. Our job is to look for companies that Mr. Market is unfairly undervaluing, determine if they are wonderful businesses run by great management and determine whether the downside of investing in these businesses is absolutely dwarfed by the upside they will return. This is not a simple task, so we try to make it simpler by narrowing our focus and selecting only no-brainer companies to invest in.

Unfortunately, holding companies are very rarely no-brainers. They are hard to evaluate at the best of times, harder still when their underlying assets are unlisted, and information is scarce. Thus, to justify the “no-brainer”-ness of the investment, we need to ensure the downside is very minimal indeed and the upside is rather magnificent.

In short, here is an overview of the investment thesis:

- ARC Investments offers access to high-growth potential subsidiaries (Rain and TymeBank), as well as very quality companies (Afrimat and Alexander Forbes) all well below their intrinsic value (shares trade at approximately 50-70% discount to NAV).

- Investments are diversified across industries and trading cheaply thus providing a very limited downside with strong growth prospects and strong positioning. It is a classic case of “heads I win, tails I don’t lose much”.

- ARC Investments has capable management with a good track record who have a competitive advantage in being able to acquire investments at a BBBEE discount and cultivate synergies across their network of investments.

- They have strong market positioning and the massive discount to NAV suggests the market is currently estimating poor returns on capital employed by management. Thus, any increase in valuation of underlying assets will have a doubled effect in the share price, increasing both NAV and the market’s appreciation of management.

Now that you have heard the thesis, let us look at some of the risks that threaten to derail it:

- This is a value trap and the discount will remain significant for a long enough time to impoverish the CAGR of this investment.

- The underlying assets are overvalued in management’s accounting. Thus, the supposed margin of safety is non-existent.

- The underlying assets all drastically underperform in the coming years, decreasing NAV and increasing the market’s distrust of management.

- COVID-19 or another similar disaster wipes out all value in underlying assets.

- Management makes very poor allocation decisions going forward and – as in the case of Brait (JSE:BAT) – severely damaging shareholder value.

Some more general risks (those non-specific to the investment thesis) will further include:

- Currency and or national market deterioration could threaten both the trading environment of underlying assets and the performance of the company relative to global equities.

- Credit and counter-party risk. ARC’s debtors may default, damaging shareholder value. This is especially pertinent due to the effect of COVID-19 on financial institutions.

- Cash flow for almost all companies is tight during the COVID-19 crisis. This may cause a liquidity issue for the managements of both ARC and its underlying assets.

Low Risk, High Reward

Having outlined the risks above, the following will be a quick suggestion for the reader to think of in answer or mitigation to the risks raised.

- A value trap occurs when the reason for the low valuation is the company is experiencing authentic financial issues in its core businesses and has little to no growth potential. Holding companies are subject to value traps in their underlying assets but as non-trading entities they themselves cannot be a value trap. Thus, we must address the potential for value traps in underlying entities (which is done in Part 3 of this essay). Regarding the valuation of ARC itself, such a steep discount to NAV is largely caused by either the market’s mistrust of the management (as can be seen in the segment on Valuing a Holding Company), bogus valuations of underlying assets apparent to the market, or the excessive fees charged by management. While there is the possibility of the market remaining unconvinced of the value of the underlying assets for a long enough time to detriment the CAGR this investment brings, we can and do factor that in to our estimations of potential outcomes when we perform our Kelly criterion assessment.

- This will be addressed in Part 3 of this essay when unpacking the value of the underlying assets. However, this risk, along with that of underperformance, are by far the most threatening to the investment thesis. We attempt to mitigate them by reviewing management’s valuations and, as with the above, factoring for uncertainty in our calculations on potential payoffs.

- Same as above.

- This cannot be mitigated outside of factoring for it in our calculations.

- This one is also a large concern and is often the primary justification for the discount to NAV that holding companies face: investors believe the allocators in holding companies cannot return a better ROI net of management fees than is available elsewhere. As our position in the company is not sufficient to warrant control over the capital allocation, we can only mitigate this by factoring this possibility into our calculations.

While the management at ARC have a good track record and appear honest and open people, it is better to factor for such a risk than to neglect it on the grounds of being a “good judge of character”. This is a key lesson to be learned from the downfall of companies like Brait (JSE: BAT) and Steinhoff (JSE: SNH).

The majority of risks (including most of those above) are discussed by the company in their latest annual report (pg. 96). Further, the company’s interim results (pg. 54) includes a more recent discussion on the more general risks.

Understanding these risks is vital to the investor. Outside of obtaining a controlling stake, we cannot do much to mitigate them but factor for them in our calculations.

While none of them appear to us to threaten the investment thesis to the point of obsoletion, incorporating them into a risk assessment is still important.

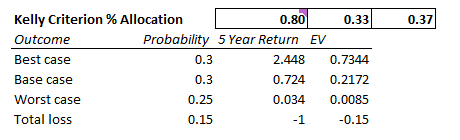

Underneath is one of our favourite tools in “betsizing” – the Kelly formula. In his book Fortune’s Formula, William Poundstone outlines the use of it in determining optimal portfolio amounts to “bet” on investments, given their expected return. Using this formula yields the below percentage of the portfolio to place in ARC.

The calculations are based on several assumptions:

- Best case: Share price realizes current NAV in 5 years. 5 Year CAGR = 28%

- Base case: Share price continues to be subdued to NAV at an approximately 50% discount for 5 years. 5 Year CAGR = 11%

- Worst case: AIL investments must be written down 70% and sold off. 5 Year CAGR = 0.6%

- Total loss: Complete loss of shareholder return.

- Return is calculated using current share price of R2.9 and an estimated current NAV of R10/share.

Note 1: The above assumptions conservatively factor for no growth in the current NAV outside of that theoretically required as a catalyst for spurring on realization of value.

Note 2: Yes, we know that shareholders will not realize the written value of the assets if they are sold off due to transactional costs and capital gains tax but bear with us here. The point is to factor for the rough estimate, not work out the exact return.

Note 3: I have used 5 years as the timeframe for several reasons:

- I believe it is a more accurate timeframe to reflect the growth potential of the investments.

- Assuming an extended timeframe forces a higher return rate to justify the investment on a CAGR basis.

- It allows for the monitoring of the investment over time. Should the NAV not be growing at all, while the investment thesis still holds, it would be a concern and would cast doubt on management. Factoring for such a timeframe regardless of growth potential affords one a limited sense of optionality to determine the return of the investment as it progresses.

As you can see, we have been very conservative in our estimations, factoring the majority of disaster, poor management and nationally related risks into the high expected probability assigned to total loss. Even with such conservative probabilities, Kelly suggests we allocate between 33% and 80% of our portfolio to the investment, depending on which variant of the Kelly Formula we use.

Several issues with the Kelly formula calculation, along with it’s variations are outlined well by Alon Bochman, CFA in this article. Ultimately however, it is a calculation used extensively by fund managers better than us at SA Equities (including Howard Marks and Mohnish Pabrai), so if it is good enough for them, it is good enough for us.

In one of his fantastic memos – this one on uncertainty – Howard Marks argues convincingly for what essentially amounts to factoring in that you could be very wrong in your assumptions. Ben Graham talks about it as having a Margin of Safety.

While the lopsided nature of this bet (as suggested by the Kelly formula) is already enough of a Margin of Safety for us, we will only be recommending 10% of your portfolio (not even half the lowest recommendation Kelly makes) be put into this bet. This should hopefully factor for the uncertainty all investors face when analysing companies.

It is not often one willingly quotes Donald Trump in public, but his self-quoting tweet on February 20, 2013 finds an odd home in this lopsided bet on ARC Investments.

In short, the risk to reward of this bet is skewed significantly in our favour.

Inside ARC

Until now, we have been looking at this investment largely through statistical lenses without unpacking the nature of the business itself.

The company believes that its empowerment credentials, balance sheet strength, the business track record of its leadership team and its brand allow it discounted investments in financial services businesses and to acquire majority or significant minority interests in non-financial services businesses. Basically, it is a BBBEE heavyweight that invests primarily in financials but likes to fling out occasionally.

ARC was founded in July 2015 (listed in 2017) and is a partially owned subsidiary of UBI. UBI was created in 2003 with the initial main purpose of building a broad-based Black-controlled investment entity as Sanlam’s (JSE: SLM) empowerment partner. In addition, the vision of UBI from the outset was to make a difference in the lives of ordinary South Africans by being a premier broad-based Black-owned and Black-controlled financial services group in South Africa.

Notable management include General Partner chairman Patrice Motsepe, Co-CEOs Johan van der Merwe and Johan van Zyl (who is also a member of the WWF South Africa board) and CFO Karen Bodenstein. The fund does not employ any other people full-time. The board of directors is discussed in the company’s 2019 Annual Report (pg. 106). We will leave it to the reader to make his own assumptions on their characters, and say only that from what we have been able to glean of the board and management from online sources, they seem to be trustworthy, capable and open individuals.

For us at SA Equities, this is a positive, meaningful company that genuinely looks to do good for South Africans. The fact that ARC happens to have a part-owner (Patrice Motsepe) who is the President’s brother-in-law and that it receives the VIP treatment from the public sector due to its BBBEE status is just a bonus.

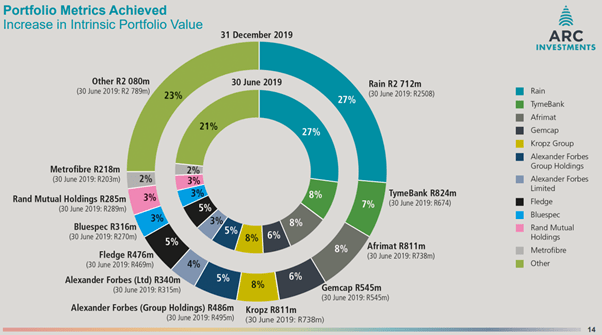

Being a holding company, ARC is made up of many subsidiaries. Figures 1 and 2 shows the major underlying assets and their growth since June of 2019. Key things you will notice are that:

- About a quarter of the investments are in financial services companies.

- Rain – a telecommunications start-up – is a very big part of the value.

- There is a whole chunk of “other” in the portfolio. These include A2X, a promising competitor exchange to the JSE, several minor investment and asset management firms diversified across a range of spheres, a couple of property holding companies, a renewable energies and resources fund, and some medium sized insurance agencies, all unlisted.

- After telecommunications and financial services, most of the rest of the portfolio is agricultural.

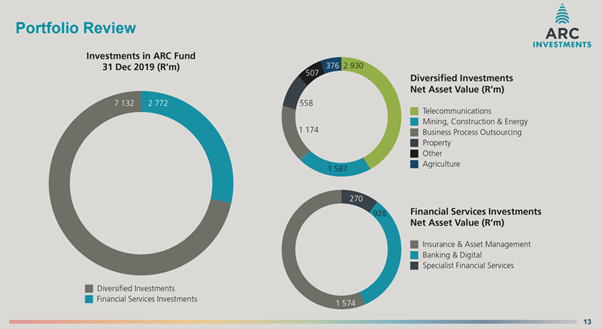

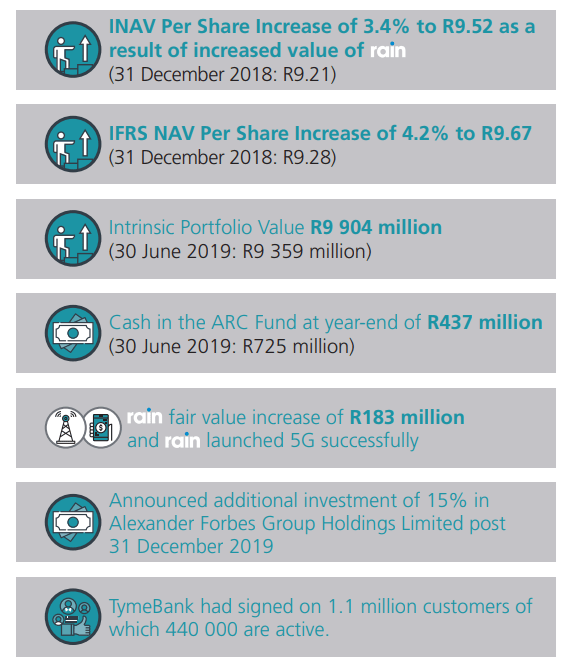

Figure 4 shows a quick overview of the financial position of the company. The disparity between the share price (R2.9 at the time of writing) and the intrinsic NAV shown is immediately apparent.

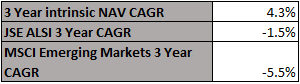

While it is hard to measure the investing prowess of management, one possible way of doing it is to compare their stated intrinsic NAV CAGR to the CAGR of two relative indexes: The JSE ALSI and the MSCI Emerging Markets. Now, I admit this is comparing apples with oranges seeing as ARC shareholders have certainly not realized even most of the NAV growth over the last couple years, that there might be inflated valuations of NAV and a combination of generally cheap SA Inc. shares and COVID’s effects on the MSCI EM index render the comparison a little less meaningful, however without information on the acquisition prices and exact current values, this makes for a decent enough proxy. That said, judging by this metric, ARC’s management certainly seems to be making decent investing decisions, especially given that the flagships of their portfolio are still very early in their growth stages.

ARC will likely need a catalyst of sorts to boost the share price into reflecting a value closer to the NAV. If anything, this is likely to be the continued meeting of rain and TymeBank’s goals as they progress through their growth curve (which they have been doing very successfully up until now). The market is anticipating a struggle in this tough, COVID-ridden economic environment. However, the online, low-cost nature of both these flagship companies uniquely positions it well to grow in such an environment.

This bet is not about growth though, it is simply about the realisation of the value that already exists (potentially tripling the share price if only to return to NAV).

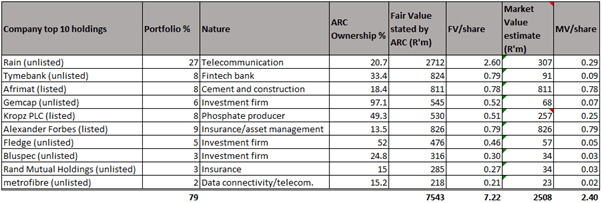

Our view is that the market is currently over-estimating the challenge faced by new companies in a tough environment and is creating undue downward pressure on the stock price to the neglect of the existing growth metrics achieved by Rain & TymeBank. This creates buying opportunity, as even if the TymeBank, Rain, Kropz, Afrimat, Gemcap and both Alexander Forbes holdings were written off entirely, the NAV of the stock would still be above market price! Further, the decreased stock price limits downside sufficiently to provide an adequate margin of safety. See Figure 6 below for a back of the envelope breakdown of ARC’s top 10 holdings.

ARC’s approach to shareholder value is to grow it via fair value appreciation of the underlying assets. It typically does not pay dividends and intends to reinvest cash received from the assets into further investment opportunities. If you believe in the ability of management to allocate capital, then this is – when factoring in the tax on dividends – clearly a better strategy than returning cash to the investor’s hands.

As with most holding companies, the fact that they are bought at a discount mean that there is potential for the unlocking of value by breaking up the underlying assets at a later stage. Usually, there is some incorporation of capital gains tax threatening investors’ returns on unbundling. However, in the case of unlisted assets (i.e.: TymeBank and rain) being listing on the stock exchanges, it will have the same positive effect on the share price of ARC as unbundling would on other holding companies, but without the necessary increase in capital gains tax for investors. Further, listed companies often trade at multiples higher than those of private companies, primarily due to the ownership liquidity premium that accompanies being listed.

As we shall see in the Part 2, having the market judge how much underlying assets should be valued (i.e. by listing them on the stock exchanges) is all but guaranteed to decrease the discount to NAV.

Further, increases in valuation of the underlying assets suggests increasing NAV, but will also provide the market with surety that the allocators of the holding company are making good choices – this will in turn decrease the market discount to NAV (which accounts partially for the potential of poor managerial allocation). Thus, any increase in underlying value will have a double effect on the share price: not only will it decrease the discount, but it will also increase the NAV.

To sum it up: If the underlying assets grow, that growth is reflected twice over in the investment in ARC. If the underlying assets are listed, that listing further narrows the discount to NAV, potentially increasing the investment further. Finally, the dividend-less model of ARC is well suited to their investment structure and goals, saving investors painful tax deductions and still compounding their capital. All the while, as we as investors wait for the somewhat inevitable unlocking of value, we – due to the venture-capital-esque and minor investment firms in the “other” section of ARC’s portfolio – are exposed to the potential massive upside that one of these little bets can pay off. Not only do we have this all-upside exposure, but we have it without any of the usual downside associated with venture capitalism and bets on early stage companies, simply because we bought in at a price when the market was essentially offering the majority of ARC’s assets for free while the listed engines of Kropz, Afrimat and Alexander Forbes chug along, returning cash to the hands of ARC’s management and nearly justifying the entire ARC share purchase themselves.

While the majority are pricing for uncertainty and negative future performance, there is the possibility that they may be wrong. The odds presented to us in this investment are so good that even if the majority ends up being right, it is a good enough bet to justify the cost. Here, we are not trying to predict which way the market is going. We are not interested in “being right”. We are trying to evaluate, humbly, what the possible range of outcomes is and how we can be wrong and still make money.

Ray Dalio, renown fund manager said it well:

You can’t make money agreeing with the consensus view, which is already embedded in the price. Yet whenever you’re betting against the consensus, there’s a significant probability you’re going to be wrong, so you have to be humble.”

Ray dalio, CIO at bridgewater associates

Continue reading in Part 2.

[Update] I have sold out of this position entirely as of September 2020. Please see Q3 Letter to Shareholders (https://vineyardholdings.files.wordpress.com/2020/10/vh_lettertoshareholders_2020.10.19.pdf) for more as to why. I no longer recommend it as a buy.

LikeLike

Hey, great articles. Care to share why ARC’s thesis has changed(and did that prompt a sale on your part?).

Keep on putting out good content!

LikeLike

Hi Simphiwe

Thanks for the comment. What changed is my investing approach – I’ve moved to focus increasingly on quality than deep value. I think ARC is likely still cheap and still think many of the underlying holdings are decent, but ManCo’s remuneration policy is a joke at the expense of shareholders. I underestimated this at the time of writing, but it came through when a capital raise was suggested to pay ManCo fees.

LikeLike