Overview

Stadio is a holding company for a collective of Private Higher Education Institutes (HEIs) in South Africa and Namibia. They currently occupy around 1% of the existing market share, which only consists of around 35% of the overall youths aged 18-24 in South Africa. There are several constraints which create the large structural mismatch between supply and demand in the higher education sector (colleges and universities). SA’s public universities are full despite the massive backlog and Stadio only faces one major competitor in the local private space: ADvTECH.

Having listed on the JSE in 2017, Stadio is a very early stage company and, over the last three years, has been rapidly acquiring and consolidating existing private HEIs under its name. Its primary operating model is distance learning, favouring an 80% distance-, 20% contact-learning split and has a broad and competitive offering of accredited programmes with many more in the pipeline.

Stadio is a spin-off of the JSE darling Curro Holdings and is in many ways viewed as the latter’s tertiary education counterpart. It is managed by passionate and experienced founder-CEOs and has a 44% anchor shareholder in PSG Alpha.

When the company first listed, there was rampant speculation around its performance and the share price bubbled to a point where it was trading at a Price-Earnings ratio of 875 at its peak. Since then, the company’s share price has been progressively decreasing despite the company’s continued improvement.

The company has outperformed all targets set by management since 2017 and, given the significant demand for HEIs, the expected increase in distance learning due to COVID-19-enforced social distancing and the niche positioning that several of Stadio’s subsidiaries occupy, we expect the drivers for growth to increase or at least remain consistent enough to meet managements’ conservative targets.

Although early stage and still progressing through its J-curve, the company is operating cash flow positive and has very little debt on the balance sheet. The premise with the J-curve is that current earnings are understated due to the heavier cost-per-student in the early stages of the company’s growth. The operating model, (primarily distance learning) is positioned to return much higher earnings-per-student as the company scales.

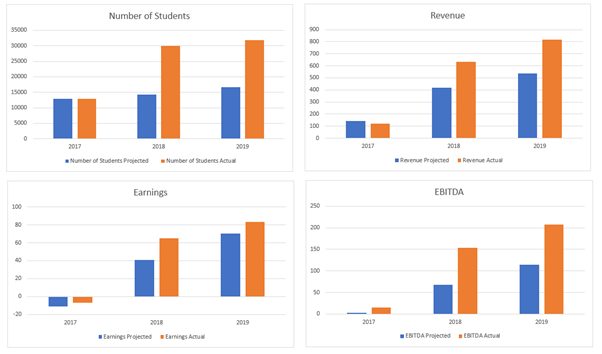

Here is a brief overview of the historical growth and the future growth expected (Figure 1). If management can attain these growth rates and continue to trade at a price-earnings multiple around 15, they can expect the share price to be around R6.2 per share in 2026. This is a CAGR of 27% for 6 years.

Why is the market under-pricing Stadio?

“When you locate a bargain, you must ask, ‘Why me, God? Why am I the only one who could find this bargain?”

CHARLIE MUNGER

From the outset, Stadio looks by no means undervalued. It is trading on a PE of 18, has a negative net-net working capital valuation and is nearly double the tangible book value. It is also carrying a large amount of goodwill (nearly 40% of its asset base) on its balance sheet – the remnant of a recent acquisition spree. As the companies were all private, there is no way of adequately approximating their intrinsic value, but the large amount of goodwill suggests that Stadio may have overpaid for these acquisitions.

A back-of-the-envelope discounted cash flow analysis (DCF) using a discount rate of 15% suggests that earnings per share needs to grow at 17% (6% if you factor for tangible book value in the valuation) for the next 10 years to justify current price. Tangible book value includes the goodwill mentioned above and therefore may not be a good indicator of liquidation value. This is a lot of growth that is baked into Stadio’s price already.

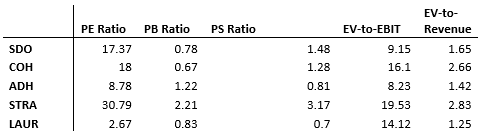

Relative to its peers both local (COH and ADH) and international (STRA and LAUR), Stadio appears priced reasonably on a Price to Sales, Price to Book and EV-Revenue basis (Figure 2).

As mentioned above, the narrative is that the bubble price was so inflated post 2017 listing that its deflation simply brought it more in-line with the intrinsic value. Hence, although the company’s performance has been increasing over the past three years the initial speculation priced it so highly that it had nowhere to go but down.

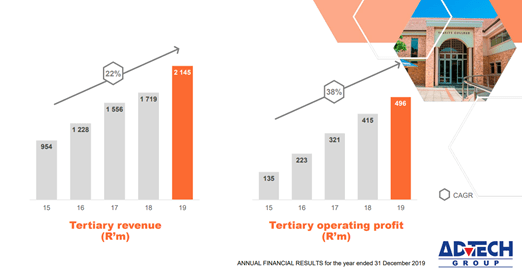

In addition to the speculation, there are several bearish features which have dampened the price: Firstly, Stadio has a very strong, significantly more established competitor in ADvTECH (ADH), who is also aggressively expanding into the tertiary education and online learning space. ADvTECH’s tertiary education flagship, Varsity College, offers both contact and distance learning and has been the primary brand in Private HEI for the last couple years. It is an established company with growing revenue, decent cash flow and will experience the same market drivers as Stadio. Figure 3 below shows the growth of ADvTECH’s tertiary segment over the last half-decade.

While the strong growth shown by ADvTECH’s revenues and operating profit speak to an undersupplied market, they also pose a threat to Stadio. It may be that the market is not expecting Stadio to meet its predicted targets on the grounds that ADvTECH is more likely to the expanding capture market share.

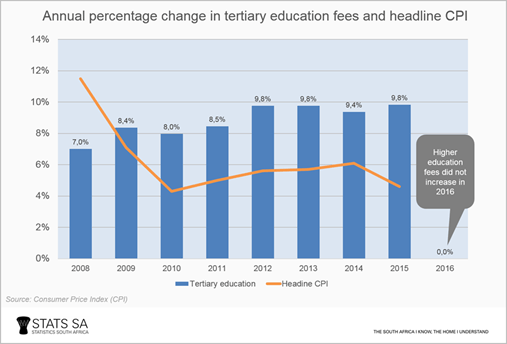

A second reason the market may be under-pricing Stadio is the high growth expectations the management has of itself. In Figure 1, the compounded annual growth rate (CAGR) required to achieve the targeted 56000 students by 2026 is ~10%. However, to achieve the targeted R500 million in post-tax earnings in the same year requires earnings to compound at 39% per annum. Assuming students only increase to the 56000 targeted, this requires earnings per student to compound at a rate of 21% per annum. The current inflationary cost of tertiary education is around 9.2% per annum in South Africa (Figure 4).

While this makes the required earnings per student CAGR a little more achievable, it still suggests that management is banking on a significant reduction in operating cost per student as the company scales up through the J-curve. The market is likely aware of these high growth rates necessary and is pricing Stadio for underperformance.

A further consideration against the company is their relative unknown brand. While many subsidiaries enjoy decent consumer awareness, very little of the market has been introduced to the “Stadio” brand. This is likely to cause them difficulty as they begin to consolidate their subsidiaries into the “One Stadio Multiversity” over the coming years. The rapid growth in Stadio’s asset base (due to acquisitions and thus goodwill on the balance sheet) with a comparatively lesser growth in revenue suggests either possible inefficiencies in their current model or a case of overpaying.

While it is true that there is significant demand for higher education in SA, the demand is not necessarily aligned with Stadio’s offering. Stadio offers both niche market products (such as its subsidiary, AFDA’s, high-end dramatic schooling) and broadly appealing products (such as a BCom from Milpark or Southern Business School). None of these products however will appeal to the large majority of those in South Africa aged between 18-24 who wish to attend university but will be unable to as they cannot afford the fees. This is because Stadio is not enough of a low-cost supplier to offer programmes at fees affordable to those mentioned. Thus, although the bulk of South Africa’s tertiary-aged youth would normally be eligible to attend, Stadio has still priced them out of its model.

Add to this that many of the company’s products (such as those offered by the very expensive liberal arts school AFDA) are seen by the market as the domain of those who have the money to get into university, but not the marks or desire, and one will find that Stadio has the beginnings of a brand/demand issue that will likely cause complications in the future. AFDA in particular has been anecdotally accused of poor administration and of not providing value equivalent to its hefty price tag.

A final thought on why Stadio is under-priced: Its primary operating model is low-cost distance learning. While traditionally the education industry has had high barriers to entry (large capital expenditure requirements and a distinguished brand) and has generated wide moats (switching costs and network effects), the online learning platforms have significantly lower barriers to entry and their moats are comparatively thin.

The distance learning industry is not geographically constrained and hence faces a broader pool of competition. It is in danger of commoditization via sources like YouTube and Udemy with the only real defence being accreditation. While this is unlikely to derail the thesis of growth over the next several years, it is a danger to the overall industry from which Stadio draws 80% of its customer base. Having covered the bear case, let us look at the crux of the thesis: the demand.

The South African education sector.

DISCLAIMER: A LOT OF THE STATISTICS HEREIN ON EDUCATION IN SOUTH AFRICA COME FROM STATSSA’S 2016 AND 2017 REPORTS. THESE ARE NOW LIKELY OUT OF DATE. AS THEY ARE THE MOST RECENT REPORTS ON THE SUBJECT, THEY WILL SUFFICE AS A PROXY. GOOD SECONDARY SOURCES ARE HERE AND HERE .

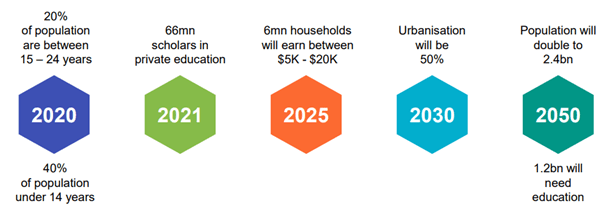

The broad investment case for Africa at large is outlined in Figure 5 below (taken from ADvTECH’s 2019 Investor Presentation).

A brief word on the holistic picture of South Africa’s economy may serve to elucidate Figure 5 above: South Africa has a very unequal society with its Gini coefficient being one of the world’s highest. This disparity has created a large class of people (the very poor) who will attend the free but woefully inadequate government schooling, a significant middle class who attend the fee-charging government schools and receive decent education, and a elite upper class who attend the country’s private schools, many of which rank among the world’s best.

This division has led to a large matric class each year who can neither afford nor are academically competent enough to attend one of the state-subsidized universities. This class is primarily made up of the very poor (whose schooling deprived them of the academic capacity) and the middle class (who usually cannot afford the high fees). Thus, many of the universities have been accused of catering too much to the elite who pay their fees. To date, the clearest expression of this dynamic has been in the #FeesMustFall movement that spread across campuses in 2016.

The government is aware of this and has made many efforts to widen the access to tertiary education, however budgetary constraints, increasing university overheads, fiscal mismanagement and limited infrastructure severely limit the amount of students that are able to attend existing public HEIs. The value of subsidies made available by the government is already much larger a percentage of the budget than that of comparative countries. There is only so much the government can spend on education.

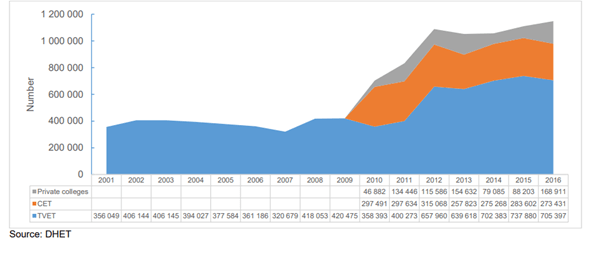

Studies suggest that the trend is towards urbanisation and nation-wide upskilling (per StatsSA, the % of people with a tertiary qualification between ages 23-38 increased from 10.9% in 2002 to 14.9% in 2018). This is set to increase further as the African consumer progresses from an agrarian to an industrialized urban consumer. In essence, the “pie” of school-leavers looking to attend university is both growing year on year, and compounding as applicants who could not get access in their first year out of school re-apply in their second (Figure 6).

In 2017, the percentage of students at private HEIs in South Africa accounted for 15% of total students enrolled. Judging by similar emerging market economies in Brazil (88%) and Chile (93%), there is still a long runway for private Higher Education Institutes.

Private HEIs have been gaining traction in the last decade. Figure 7 below shows the increase in private HEI’s share of the market for students who, whilst not studying towards a degree, are still in training for a diploma or attending a trade school.

In this article, the Norwegian CMI outlined its approach towards South African universities, as well as some of the challenges faced by the public sector. An interesting takeaway from the article is the below:

“The biggest challenge in South Africa’s higher education is however, not the issue of fees, but continued poor access and very high dropout rates for those who have entered the system. While there has been an impressive increase in the number of black students, also from very poor households, the proportion of poor black students at South African universities are very limited. Less than five per cent of black secondary students with parents earning less than 120 000 qualify for entry into universities while the percentage of students with parents earning more than 600 000 is 70 percent. And even more disturbing: Barely 50 percent of undergraduate students have managed to graduate five years after entry. And among those being supported by the national financial aid scheme two-thirds of undergraduate students have become drop-outs five years after entering. Most drop out after the first year, many because the financial support is insufficient and with accommodation and transport being too expensive, but mostly because they fail to pass exams.”

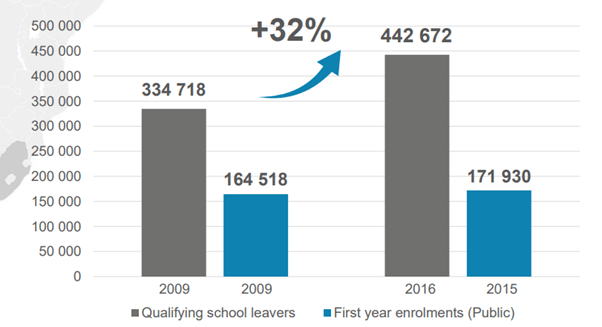

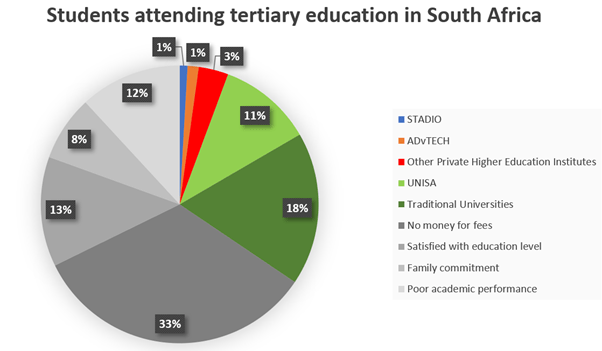

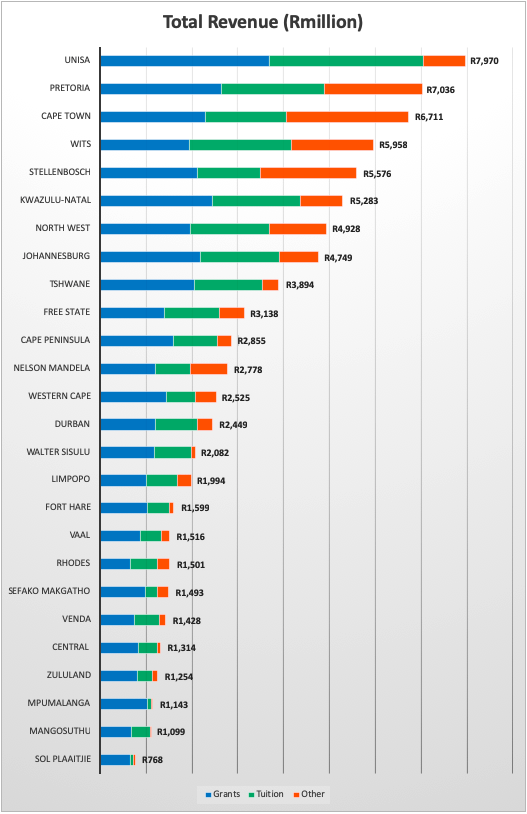

Figure 8 illustrates the extent of the demand relative to supply for higher education in South Africa. The grayscale segments are those who are currently between the age of 18-24 and are not attending university for the reasons below. The key takeaway from this graph is the comparatively small amount of increase both Stadio and ADvTECH need to double their market share, as well as the significant supply shortage created by the public universities (UNISA & Traditional Universities).

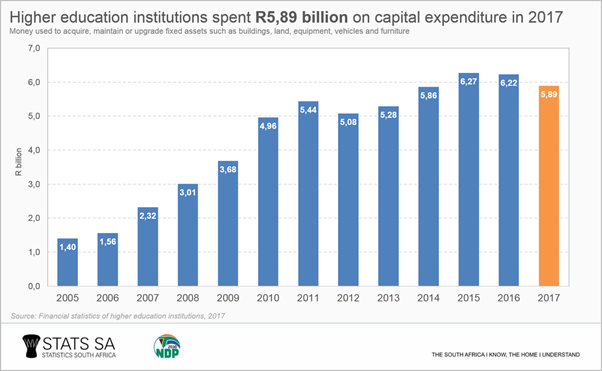

Most public universities are heavily subsidised by both the government and alumni, generating very little of their own profit despite the high fees. Their operating model relies heavily on this (limited) external funding (Figure 9). As these universities continue to expand to try and accommodate the growing “pie” of those who need tertiary education, they will continue to run into funding issues. Figure 10 shows the increase in capital expenditure that the public universities have experienced as they attempt to adjust to this demand.

In summary, the public HEIs face the below challenges:

- Limited budget available to institutions from the national fiscus

- First-year enrolment demand exceeds public university capacity

- Infrastructure provision under strain

- High drop-out rates, low graduation rates and the long-time taken to graduate

- Limited articulation possibilities

- Increase in operational costs placing further pressure on government to increase funding to these institutions

- Subject to intermittent student and staff protests

The private sector serves to reduce the pressure on the state to provide education to youths and reduces the longer periods of studying taken at public universities (thus negating extended state subsidisation for the student). Thus, Stadio’s lower cost, its average module success rate of 80.9% and its ability to adapt quickly to changing market demands should be a compelling set of statistic to all stakeholders, including those in the public sector who are looking to offload some of the burden.

To the prospective investor, the combination of all these measurements should suggest two things:

- There is a structural demand that is unlikely to go away anytime soon, and

- The subsidy-dependant “business model” of public universities is unsustainable in attempting to meet this demand.

The question now remains, how likely is Stadio to meet this demand to the extent targeted by management within a short enough time frame to yield a winning ROI for investors?

A look at Stadio’s management, growth and metrics.

Of all the companies analysed here, Stadio is by far “doing the greatest good” in the orthodox sense. Besides their drive towards “widening access to higher education”, Stadio dedicates 1-3% of revenue per annum towards scholarships and bursaries, engages students in a host of socially-responsible outreach activities and the majority of both staff and students are black and female. All great things. That said though, the business of companies is business, not charity.

The value add of Stadio to all stakeholders is outlined in Figure 11 below.

Until earlier this year, Stadio was led by Dr Chris van der Merwe (57), a highly respected name in the SA education industry. Chris founded Curro in 1998 and Stadio in 2015 and has since led both to achieve both growth and nation-wide impact. Dr van der Merwe has since handed over the reigns to Mr. Chris Vorster (52), who is also a founder-CEO and began the Southern Business School in 1996, which he merged with Stadio in 2017. Dr van der Merwe is retiring to be a non-executive director on the board. Both men are very high-calibre individuals with deep experience and – for all intents and purposes – appear to be men of integrity.

The management are incentivised with cash benefits for increasing organic revenue growth, the EBITDA margin and core Headline Earnings Per Share (CHEPS). These incentives are not excessive and serve to align the management with shareholder’s interest in the short term. Management are also entitled to share options of up to 7% of the company subject to similar metrics. All this can be found from page 77 in the company’s latest annual report onwards.

The board of Stadio is comprised of individuals with a very broad set of skills. Further, it is racially diverse (Figure 12) – a meaningful metric given that the abovementioned wealth divisions are largely along racial lines. It is also slanted towards those with experience with 67% of the board being older than 50 years.

The management are also well aligned with shareholder interests, with 11% of the company being owned by directors (Figure 13).

To-date, management have met or exceeded every target they set in the 2017 listing (Figure 14). Should they continue to do so, and the company trades at a Price/Earnings multiple around 15 (currently: 18), then the valuation should experience a 5x return within the coming 6 years. In this instance, we would be buying the company today (R1.5) for a 6 year forward P/E ratio of 3.6. Not exactly Pabrai’s hidden P/E of 1, but decently close.

Regarding the outperformance above, analyst Anthony Clark believes that the acquisition of subsidiaries like Southern Business School (SBS) have helped a lot as their education is tailored in an asset-light, learning-heavy manner. It is Stadio’s belief that the primary purpose of education institutions is to educate, hence they reduce non-essential overheads as far as possible (as reflected in the large portion of value-add to educators in Figure 11) This means that, relative to traditional universities and UNISA, Stadio’s operating costs are significantly lower, enabling them to be competitive despite the government subsidies to the former.

It is important investors note this cost-saving distinction. In a 2019 interview, then-CEO Chris van der Merwe noted that Curro’s slow progress through the J-curve had cost investors significant potential returns and had taught management a lesson about overspending on certain unnecessary ancillary offerings that do not increase the school’s return on investment. He reiterated that Stadio was intent on progressing through the J-curve as quickly as possible and would keep a lid on costs as much as possible to expedite the process.

The core of management’s strategy (as set out in the 2017 listing prospectus) has been to accumulate existing brands in the private HEI space and to then consolidate them into One Stadio Multiversity brand. To date, the growth in infrastructure and acquisitions have been funded by the capital raising associated with listing (R640m), a BBBEE ownership transaction (R200m) and some debt taken on in 2017 which has been almost entirely repaid. While management is still keen on expanding into offering STEM field qualifications (a deficit in their current offering), they have for the most part finished their initial acquisition spree and will be focused on consolidation going forward.

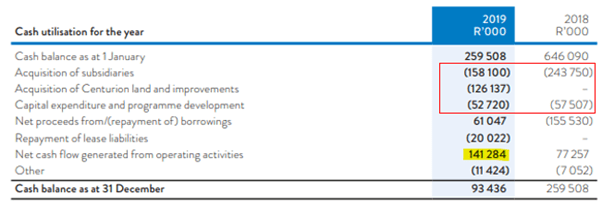

The cost of their acquisitions have been high (as evidenced by the goodwill mentioned above), but the company is still cash positive with the operating cash flow increasing year-on-year (see the highlighted component in Figure 15). The financial director expects that in the long run (3-5 years) the company will reap the efficiencies of these acquisitions, but in the short-to-medium run the company is likely to incur additional costs associated with the migration of all these brands into the Multiversity.

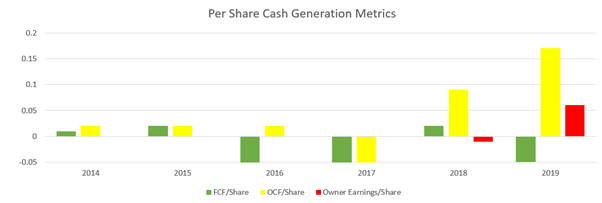

Figure 16 is a tracking of the per share cash generation metrics throughout all of the financials available for Stadio (including those available on it from its pre-listing stage when it was still under the wing of the listed Curro Holdings). The narrative of this graph is the increase in operating cash flow (OCF) per share. For an early stage venture it is yielding strong OCF growth, much of which is (per Figure 15) funding the expansion. This is encouraging as it suggests growth is already in an organic phase.

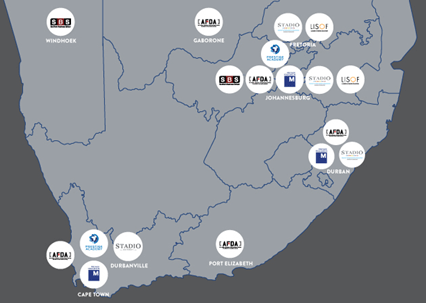

The red box in Figure 15 outlines the significant portion of cash spent on expansive growth. The land in Centurion, Johannesburg is to be one of two “headquarters” for the One Stadio Multiversity brand. The other is based in Durbanville, Cape Town. Both will act as a campus for students and will feature a combination of all Stadio’s subsidiaries (Figure 17 shows the current geographical footprint). Each of these subsidiaries have strong brands, with AFDA and Prestige being the leading brands in their niche markets.

Acquisitional growth typically creates issues like interpersonal division as absorbed entities retain their brands and management. There is no guarantee that the cultural fit will remain homogenous between the brands. While to date, management has been headstrong in their commitment to acquisitional growth, their focus looking forward seems to be primarily on integrating the now-acquired brands under their umbrella. There is little talk of more acquisitions in their recent annual report and far more on consolidation and the growth and accreditation of existing platforms. It looks as though the growth they need to get to R500 million earnings by 2026 is expected to come from organic growth.

On the topic of acquisitional growth, Chris van der Merwe believes the company have been conservative in their expansion relative to competitor ADvTECH’s aggressive buying up of land. He holds that Stadio’s decision to acquire existing brands was to establish it as a competitor as soon as possible. The average time taken to accredit a programme in South Africa is 2 years, so Stadio’s decision to acquire rather than develop their own programmes from the outset was as much for growth as it was to distinguish itself as a market player upon listing. Looking forward, he says, there will be more focus on accrediting in-house programmes and increasing in-house research output to generate internal material.

When pressed about the discrepancy between Stadio’s brand and those of its subsidiaries and competitors, Chris’s stance was that a brand must be grown organically. He believes that the “prestige gap” between private and public education will lessen as Stadio engages with the market more actively.

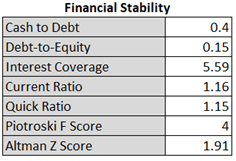

Currently, Stadio is sitting in a secure financial position, well positioned to weather and profit from the COVID-19 onset. Figure 18 shows the financial stability of its balance sheet. Information on what each of these metrics mean will be available with a Google search, but are also discussed here. The Altman Z score and the Piotroski F Score are worrying as they are nearing the bottom of the score’s “safe” zones, however when read in conjunction with the rest of the metrics, the takeaway is that the company is, while not completely in the clear, comfortably secure.

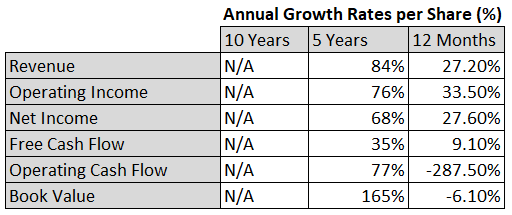

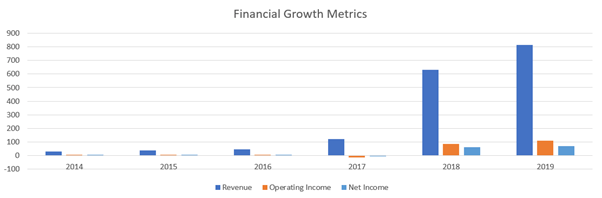

The company has grown rapidly since listing with Figures 19 and 20 show the growth rates across varying key performance indicators.

Figure 20’s growth in revenue graphically dwarfs the respective growth in operating income and net income, but they are similarly exponential. It is likely that these growth metrics above are much of the reason for the market valuing Stadio at its apparently high valuation multiples (cf. Figure 2).

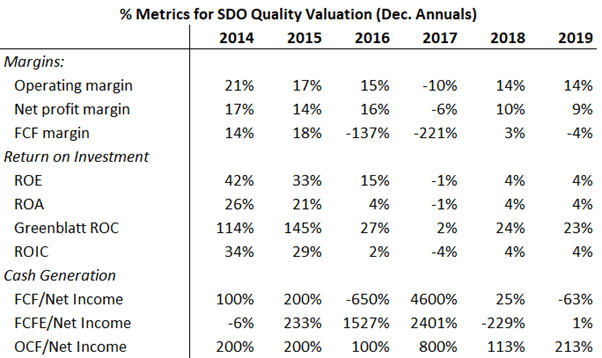

Management has done a fair, unremarkable job at returning capital, maintaining margins, and translating earnings into cash (Figure 21). In 2017, their year of listing, most metrics were down as the company made a loss in that year (as expected by management). Prior to 2017, many of the returns present an upwardly skewed depiction of the businesses quality as it was under the wing of Curro. Further, the cash generation metrics have fluctuated wildly and while this is to be expected of a company in its early stages, it is not an encouraging sign. The primary positive is the relatively steady increase in operating cash flow generation.

On the topic of Curro, Stadio’s management expect the school to act as a minor feeder into the multiversity once the consolidation is complete. The extent to which they believe this will increase student enrolment is uncertain, but given their forecasted numbers, they do not seem to believe the “feeder school argument” will have too strong an effect.

All-in-all, Stadio ought to be seen a little more like a start-up than a typical listed company. Its simple, focused business model, financial position and operating cash generation are both positive signs, as are the facts that it has

- Established niche market brands in an industry which requires high capex and hard-to-acquire accreditation,

- A capable and aligned management team with access to capital and strong financial backing,

- An operating model which suggests exponential economies of scale, and

- Is in a market which is immensely and structurally undersupplied.

Looking to the competition, both in the form of ADvTECH and the public universities, one will find that Stadio is – while not a true low-cost supplier – better positioned to capitalize on the lower end of the market than its competitors and is one of the players most likely to gain market share rapidly. Its moats include being a low-cost provider (relative to traditional universities) due to its disruptive business model, having no legacy heavy asset base and being more agile and adaptive to market demands than competitors (all of which have entrenched systems that require significant effort to manoeuvre).

The industry, competitors, and distance learning

Traditional schools and universities are high fixed cost businesses. They require large amounts of capex, but also contain high operational leverage. Geographically, this means that it is unlikely there will be more than one university in each vicinity as any more would split the market share to a point where the unit-cost of a student is unprofitable. Further market entrants must pay for course accreditation, the marketing fees associated with becoming an established brand and the regulatory costs associated with rezoning land. Add this to the fact that a typical student is under social pressure to attend university, spends at least 3 years there, and pays their fees in advance and you have an industry with high barriers to entry and significant switching costs.

Most of these barriers dissipate with the implementation of distance learning. The geographic barriers are eroded, and local distance learning firms must compete with international firms. In South Africa, international distance learning firms cannot compete with local firms pricing (due largely to the difference in ZAR/USD purchasing power) and hence do not threaten too much of Stadio’s market. Further, the switching cost associated with online universities is significantly lower as you do not need to relocate to attend them.

However, in theory, the lower capital expenditure required and the potential for rapid scalability suggest that distance learning-oriented institutions will receive significantly better ROI than traditional universities as the per-unit costs shrink exponentially with scale.

The lifestyle appeal of universities like Stellenbosch or UCT makes them the elite of the institutions and gives them decent pricing power. These institutions are unlikely to compete much with Stadio as their contact learning will be priced out of reach of most of Stadio’s target market anyway. The real competitors for Stadio are the middle-lower tier universities like UKZN, the massive distance learning centre Unisa and of course, ADvTECH. Stadio’s market is unlikely to be the high-end school leavers who can afford the traditional university fees. They are targeting instead the working adults and middle-lower class students looking to gain a quality education without the frills provided by a university like Stellenbosch.

An important distinction here is between accredited and unaccredited education. On the unaccredited front, there are wonderful free resources like YouTube, Khan Academy, Quantic and EdX. There are also low-cost paid resources like Udemy and Masterclass. Stadio will likely never compete with these international players as their infrastructure is too established and they are the epitome of low-cost providers.

The bulk of the market share for accredited distance education however will be up for debate. Given the importance of and years spent in tertiary education by the average student, product differentiators like user experience, interactive interfaces, efficient administration and international accreditation will be key in determining who will get the lion’s share of the market in years to come.

On this front, both ADvTECH and Stadio have Unisa beat. The advantage of a private HEI is that the smaller classes improve access to staff and offer more support (both virtually and in person). They both offer real industry exposure and niche qualifications (with Stadio edging out ADvTECH’s Varsity College in this area) and because the students are customers, they will typically receive better service.

While the target market will likely gravitate towards the provider of the better service, the reality is that as it is not a lifestyle experience and given that all firms will be offering accredited qualifications, the distance learning market is likely to become commoditized. While this will benefit the South African consumer, it does not afford Stadio much pricing power.

Further, traditional universities like Unisa and the lower-middle class universities are heavily subsidised and currently have a near monopoly on accredited distance learning (albeit as mentioned, without the pricing power a monopoly brings, and without the growth potential for structural reasons discussed above). This means that competing with them will be harder for Stadio.

Much of the basis for growth in ADvTECH and Stadio will be the claiming of those who do not get in to the existing universities, thus their competition will more likely be with each other than with public HEIs, which are already experiencing constraints. It also means that their pricing against each other will play an important role in the future. Both ADvTECH and Stadio have very low returns on invested capital, largely due to their recent acquisitions and expansion.

ADvTECH is an established business operating across sub-Saharan Africa which listed on the JSE in 1987. Its flagship, Varsity College, was established in 1991 to assist part-time Unisa students and was acquired by ADvTECH in 1997. The company has very solid financials and has experienced strong growth in the last half-decade. Some of the criticisms against it is that its aggressive expansion in the last decade has been fuelled largely by debt-financed acquisitions, that its spending policy has been too lavish and that the market segment for its mid-fee model is not as large as ADvTECH originally thought.

Much of these criticisms however revolve around ADvTECH’s primary and secondary school business, which accounts for about 60% of their revenue. The other 40% is from their tertiary education segment, much of which is distance learning oriented, and is growing rapidly (Figure 3).

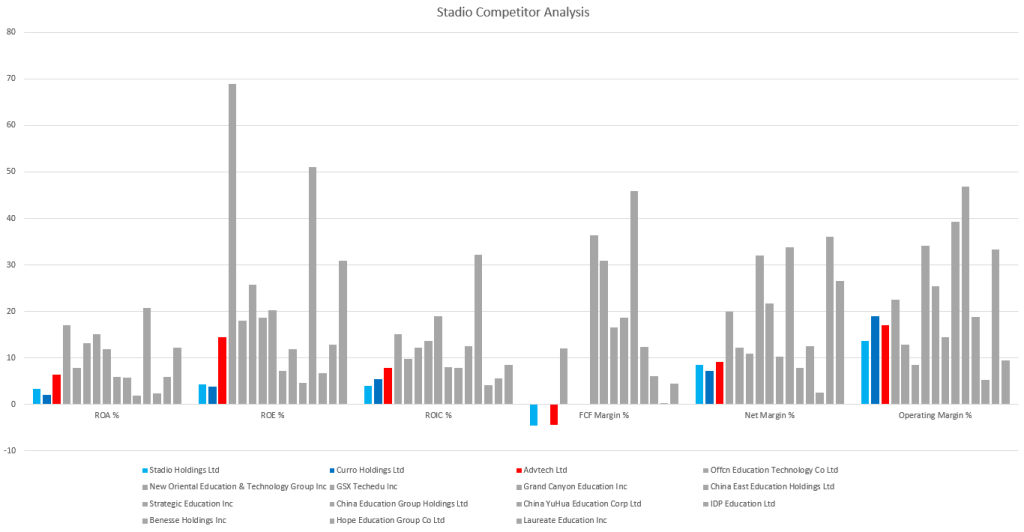

Figure 22 below is a comparison between ADvTECH, Curro, Stadio and a host of foreign competitor distance education firms.

The key takeaways from the figure above are as follows:

- Stadio is already achieving margins and returns like ADvTECH’s, despite being a much younger company,

- ADvTECH is currently achieving better returns than Stadio

- As Stadio and ADvTECH progress through the J-curve associated with their recent expansion, they will likely realize higher returns and margins more in line with global competitors.

Curro is included in the comparison above to provide a proxy to ADvTECH’s school segment returns. The result of this is that in the instance of ROE, ROA and ROIC, if ADvTECH’s school performance is anything like Curro’s, then it’s tertiary segment performance is likely understated in the depiction.

Whether the outperformance of ADvTECH is due to its managerial excellence or the large market demand is up for discussion. It is likely both. Any part of it attributable to market demand is a promising opportunity for Stadio, while any part attributable to management is certainly threatening.

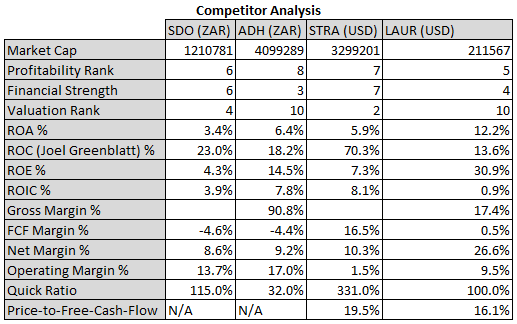

Figure 23 contains several metrics for Stadio (SDO), ADvTECH (ADH) and two of its leading international peers, Strategic Education (STRA) and Laureate Education (LAUR).

The combination of Figures 22 and 23 suggest that currently, ADvTECH is closer to its international peers while Stadio appears to underperform. This is likely due to its relative infancy as a stand-alone company and it is likely to experience growth in these metrics as it progresses through the J-curve.

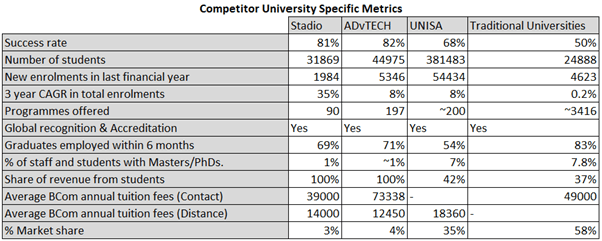

Figure 24 is especially important, as it outlines many of the areas not determinable by financial analysis alone. Given the differing stages of ADvTECH and Stadio’s business, a financial comparison is of limited use. Instead, understanding the products will offer insight into the business models.

The data for this table was compiled from a variety of sources, and the “Traditional Universities” column, being an aggregation of data from all universities, is likely not an accurate representation of any one individual institution. For instance, the Number of Students is simply the total number of students attending traditional universities divided by the number of traditional universities that there are.

The first thing to note is the distinct success rate differences between private (Stadio/ADvTECH) and public HEIs. This speaks to the equivalent or better education quality offered. The second is the number of programmes offered. At present, Stadio still offers comparatively few programmes, with most of its deficit being in the STEM field.

While both ADvTECH and Stadio prioritise graduate employment as a metric by which to judge education quality, neither perform outstandingly well when measured against traditional universities. The reason for this is threefold: firstly, Stadio holds that around 25% of their students either continue with their studies after graduation, which is not measured in their metric, secondly, the company emphasizes an entrepreneurial approach to working and encourages its students to start their own businesses. This too is not measured in the metric. Thirdly and most importantly – as this article suggests, the majority of employers still value contact learning over distance learning in choosing employees.

The difference in the percentage of students and staff with Masters/PhDs is an important one, as it suggests that if ADvTECH and Stadio would like to ultimately develop their universities into competitive academic institutions capable of producing research and generating internal material for study, they will need to focus on increasing their output of doctors.

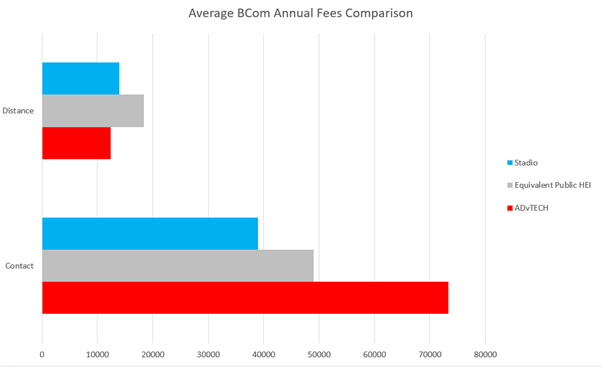

The final important takeaway from the table above is the difference in pricing. Stadio is pricing its products (both contact and distance, with the exception of AFDA) towards the lower end of the market, while ADvTECH is continuing its mid-tier targeting through Varsity College’s contact component which is, in many cases, even more expensive than traditional universities. ADvTECH’s distance component is priced slightly under Stadio’s, making it the cheapest available qualification.

The fee comparison is highlighted in the graph below (Figure 25). Over 50% of South Africa’s registered students are studying towards a commerce degree, so the fee comparison below uses a BCom as its reference point.

To summarize:

- Distance education is very different to contact education and is likely to increase in commoditization, depressing prices and widening access to consumers.

- Stadio is well positioned to capture some of these consumers but will face stiff competition from ADvTECH.

- Stadio’s contact offerings are significantly cheaper than its competitors and its distance learning offer, while not the cheapest, is cheap enough to appeal to those who would normally try to attend Unisa but are unable to gain access.

- Stadio is in its development phase and most of its metrics are understated and have significant room for growth if judged by the metrics its peers are attaining.

These four points suggest that despite the competitiveness between the two firms, both are likely to gain market share significantly in the coming years. However, because of ADvTECH’s school segment, its shareholders are less likely than those who own Stadio to experience the compounding value that such a gain will generate. While both are strong, well positioned companies, Stadio has better growth prospects.

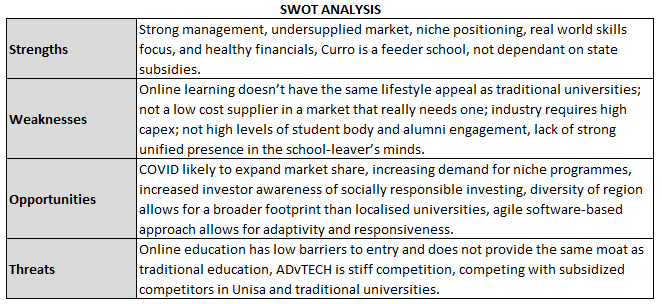

A brief SWOT analysis will hopefully provide a little help (Figure 26).

Valuation & odds

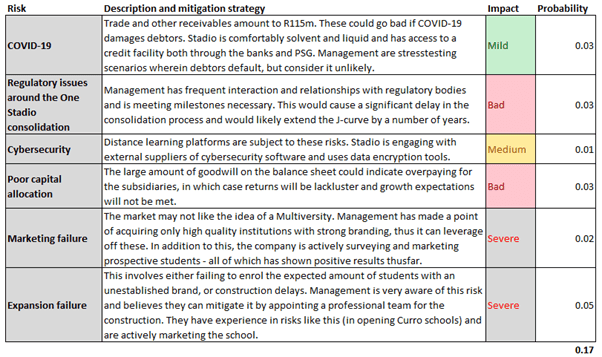

In addition to the bear case mentioned earlier, outlined below is a brief overview of the potential risks associated with Stadio that could threaten to derail the investment thesis (Figure 27).

To understand how to value companies, please see the investment thesis for ISA Holdings as the below will simply contain a brief outline of the numbers, not the valuation process itself.

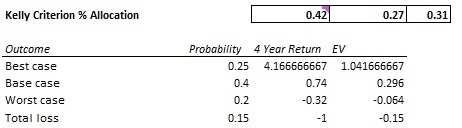

The below valuation (Figure 29) is comprised of a few traditional valuation models, as well as several discount cash flow (DCF) models, each with varying methods of calculating intrinsic value, and running each model through three potential scenarios:

- Best case: Stadio grows at a rate that meets management’s expectations within 6 years (25% probability).

- Base case: Stadio grows at half the rate expected by management (40%)

- Worst case: Stadio grows around 5% per year (20%).

- Total loss of capital based on our evaluation of the risks above (15%)

These are comfortably conservative expectations. Management’s expectations have consistently been outperformed, and the demand is so high, that it is likely the best-case scenario is even too conservative. However, for the sake of precaution, the above probabilities are used.

Under these scenarios, a simple Kelly formula arrives at the below results (Figure 28). According to this, 42% of one’s portfolio should be allocated to Stadio. This allocation requires a high degree of volatility tolerance, as well as self-assuredness. Hence, the overall recommendation, given the uncertainty of growth, is that between 8-10% of your portfolio is allocated.

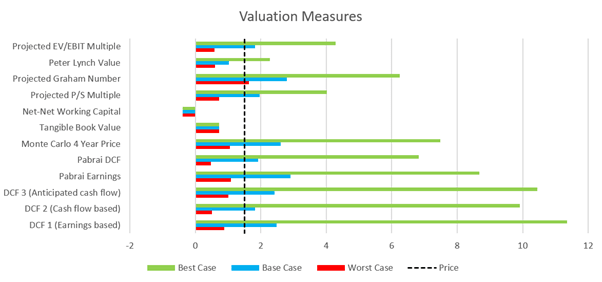

The breadth of valuations in Figure 29 suggests that despite the bear case near the beginning of the article, Stadio is trading near the lower end of its range of intrinsic values. The bet is that Stadio’s price is unlikely to fall much further, while the upside is asymmetrical. It is a classic “heads I win, tails, I don’t lose much”.

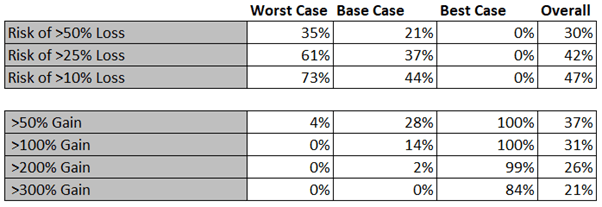

Finally, running the above figures through a simple Monte Carlo simulation yields the below results (Figure 30). The risk of losing >50% is only slightly more than the probability of gaining >200%.

Overall, given the bear case above and the high chance of loss, we are not comfortable allocating more than 10% of our portfolio to Stadio. That said, the lopsided nature of this bet presents opportunity for a good investment. Stadio also provides the investor with a sense of wholesome contribution to society through its business model.

One thought on “Stadio Holdings: Strong growth prospects in an undersupplied sector.”