Investment Thesis Overview

As mentioned above, Alaris Holdings designs, manufactures, and supplies defence and specialised antennas. It has a market cap of R300 million. The group generates over 90% of its revenue ex-South Africa through its acquired subsidiaries, all of which have experienced significant growth since acquisition and have decent growth prospects in foreign markets.

The company’s key strategic pillars are its global footprint, in-house intellectual property (IP), and niche expertise. Looking forward, the company has sufficient cash on hand to enable more acquisitions but has expressed greater interest in organically growing subsidiaries which it believes are well positioned to capitalise on growing market share in their niches.

The company has evolved from a SA-based manufacturer which exports its products overseas, to a holding company headquartered in South Africa which invests in global RF technology companies with similar business models that inter-operate as bespoke product and solution design factories for their clients.

While Alaris offers commoditized, standard models of antennas and RF technology, its primary income is generated from the high-margin bespoke products which are custom-designed. This operating model solidifies a working relationship with a customer and creates a minor switching cost moat for Alaris. This moat stacks well with the extreme specialisation necessary in the high-end defence RF industry which, when combined with the in-house IP that Alaris generates, affords them reasonable pricing power and customer retention.

The investment thesis for South African based investors is this: Alaris is under-priced relative to its business quality and demonstrable growth prospects, and will act as a hedge against both ZAR depreciation (as it earns majority USD and EUR) and broader market uncertainty arising from international tension (as the defence sector is typically counter-cyclical to the broader market which outperforms in times of stability).

On a local value-add front, the company still manufactures a large portion of its products in South Africa and hence creates both wealth and jobs locally, while deriving indirect foreign investment by way of sales overseas. As a continent, Africa should be looking beyond its current commodity exports towards exporting increasingly sophisticated, processed, and value-added goods like RF technology.

Bear Case

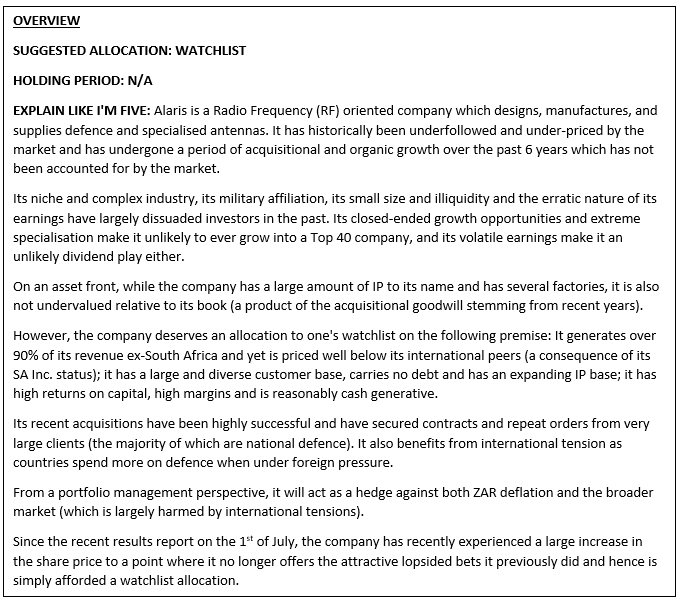

Barring the recent jump in share price (approximately 60%) during the time of writing this article, Alaris has been perpetually undervalued by the market. Figure 1 shows the current traditional valuation multiples over the course of 2020. The red line shows the time of writing.

As indicated by Figure 1, the company has been progressively downgraded on all fronts by the market barring the last week. This 60% increase in share price (due to the recent half-year results release) has brought the share closer to its intrinsic value and, while there is still further upside to be had, especially over the long term, the bear case now holds more water as the higher the price of the stock, typically the more subject to loss the investment becomes.

Essentially, the bear case is threefold:

- The RF technology field (in particular, in the defence sector) leans heavily on innovation from companies as each try to develop more advanced products with old models becoming progressively obsolete.

Like most technology companies, this subjects Alaris to the need to constantly innovate. However, unlike most technology companies, Alaris does not operate in a data-enhanced “winner-take-most” market where the implementation of feedback loops and strategic flywheels afford the most innovative companies a structural advantage.

While the requirement for innovation does serve as a barrier to entry in the RF industry, and while Alaris does place a lot of emphasis on in-house IP generation, the nature of their business makes that IP a necessity for successful operation rather than a moat or competitive advantage.

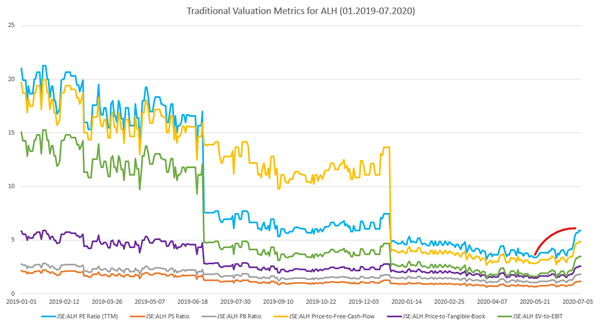

Further, because of their small size and reliance on innovation, employee turnover is a large risk for Alaris. The company needs to both recruit existing experts and develop expertise in recent graduates before they become worth more to the business than they cost. This time taken to develop the niche expertise subjects the company further to downside risk. Alaris also remains a small player in the global scale, even within its RF/defence niche. An approximate market share diagram is shown below in Figure 2 (as judged by annual revenue

The smaller market size of ALH means that, while there is more room for growth, it is also facing stiff competition from the more established players who benefit from synergies (Hensoldt and Reutech are both owned by conglomerates) and economies of scale. It is important to note however that most of the RF technology companies are private and are not accessible by most investors.

- The second component of the bear case is more related to the market than the company itself. Because of their illiquidity, small size and highly technical industry, investigation into their worth as an investment is often more costly for analysts than the benefit of even significant upside.

The factors that cause market disinterest are structural and unlikely to be catalysed away. The company will never grow exponentially. It operates in too niche an industry which is by nature closed-ended. The lumpy nature of its contract work causes very irregular cash flows and earnings which makes estimating intrinsic value very difficult and the volatile growth metrics in the past are unstable at best. Finally, the military application of its products may damage market perception.

All considered, the market may never recognise the value of Alaris Holdings. At least not in a timeframe which yields a sufficient CAGR.

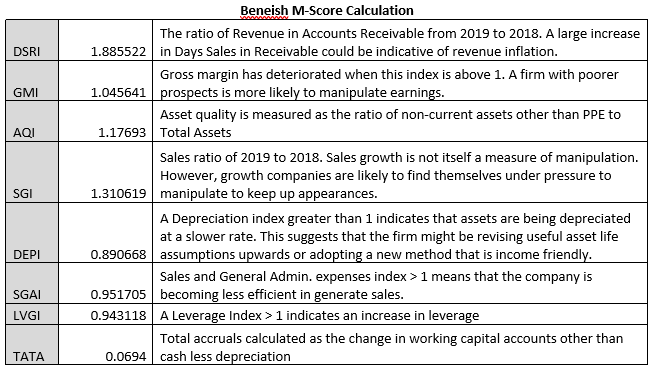

- Finally, there are minor traits in Alaris’ accountancy that are typical red flags for investors. This however is said with much caution as to-date, their management has been nothing short of upstanding and transparent.

Figure 3 below shows the breakdown of a Beneish M-Score. The M-Score is a probabilistic weighing of various factors that are likely to increase the odds that a company is manipulating or will manipulate earnings. ALH’s M-Score is -0.95, and anything above -2.22 suggests the company is likely to be an accounting manipulator.

Separate somewhat from the bear case, but nevertheless something that is not in ALH’s favour: the board is 100% white and 70% male. It is not BB-BEE compliant and this will likely harm its ability to enter local government contracts. It also disallows certain funds from investing in it and dissuades certain clients/suppliers from engaging. All considered, when you are a South African company, you most certainly want to be BB-BEE certified.

Management also has 5.4% of the company’s market cap outstanding as options owed to directors and management. This will negligibly dilute the estimated earnings and valuations going forward, but is nevertheless mentioning, as options awarded to management are typically not things that are in line with shareholder interests.

As unpacked above, the bear case is primarily about an industry-specific lack of moats around ALH. It is backed by a non-transient market neglect and the probabilistic incentive to manipulate accounts on an M-Score basis. Similarly, the bull case rests on one primary reason and is underpinned by two secondaries.

Bull Case

“If you have more than one reason to do something… just don’t do it. It does not mean that one reason is better than two, just that by invoking more than one reason you are trying to convince yourself to do something. Obvious decisions (robust to error) require no more than a single reason.”

Nassim Taleb, “Antifragile”.

As mentioned above, the bull case rests on a primary reason: Alaris is undervalued relative to its peers and its future earnings. The secondary reasons underpinning this primary reason are that this expansion affords the investor a sturdy hedge against the ZAR and market uncertainty, and that it is a high-quality company.

As far as relative valuation goes, ALH is trading at:

- P/E of 5.89,

- P/S of 1.16,

- P/Tangible Book of 2.56,

- P/FCF of 4.86,

- EV-EBIT of 3.48

While such low multiples are not uncommon in South African small caps, they are very irregular for a global technology company with strong fundamentals, decent growth, and no debt. Add to this that 67c of the share price (R2.8) is cash, and one is effectively paying R2.1 per share for rest of the company.

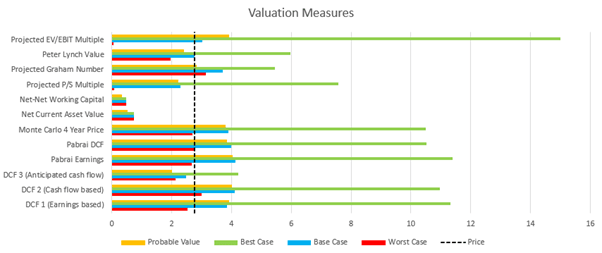

On an intrinsic valuation basis, Figure 4 outlines how the market is currently valuing ALH relative to its prospects. As can be seen, prior to the recent increase in share price from around R1.8 per share to R2.8 per share, the market was valuing ALH well within its worst-case limits. The current price is marked by the black line and, while still at the upper end of the worst-case valuation, it is now more reasonably valued.

Even so, the current price is well below the values expected should the company continue with its current 10-year annualised growth rates (best-case).

Figure 4 has used various valuation methods to arrive at a spread of valuations. All have been very conservative. The probabilities for the best-, base-, and worst-cases are 20%, 30% and 20% respectively with a 30% probability of total loss occurring. As such, the probable value is the sum of the valuation of those cases weighted with their probability. It is likely that these estimates are too conservative and underemphasize the difference between the intrinsic value and the market price.

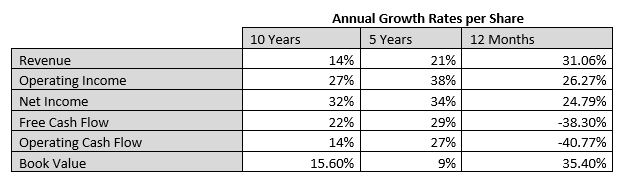

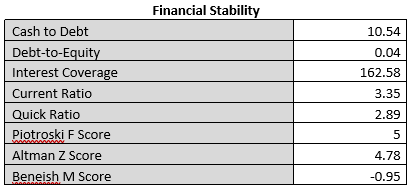

The company has grown at respectable rates over the last 10 years (Figure 5), and is sitting in a comfortable financial position (Figure 6) with minimal debt, a strong cash balance, healthy financial stability (a Piotroski F-Score of greater than 4) and is nowhere near bankruptcy (an Altman-Z Score of greater than 2.99).

A high-quality company is as follows: it compounds high rates of return on investment while maintaining above average margins over a long period of time and translating the subsequent earnings generated effectively into cash for shareholders.

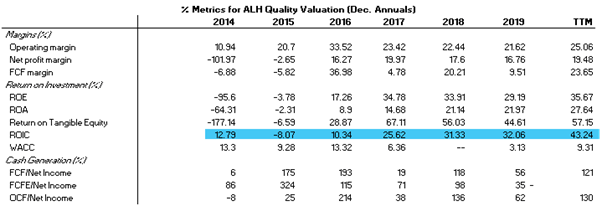

In Figure 7 although erratic, the metrics for ALH suggest it is a high-quality company as defined above. The ROIC (highlighted in blue) has in recent years improved significantly because of the company’s expansion overseas (along with most other metrics) to the point that it now far outsizes the company’s WACC. This is indicative of a company generating more value than it absorbs.

The undervaluation component of the bull thesis suggests that the market is (or was, until the recent surge in share price) still pricing ALH as the company it was in 2014, prior to the international expansion.

In 2014, the company made a significant accounting loss, and much of 2015 was spent in recovery. This loss in net income presents a very distorted picture and skews results largely. While revenue tracks well for 2014, the company concluded the purchase of Aucom (see below) through equity. The shares used to purchase Aucom were valued at 75c per share at the time of conclusion but were required to be valued at 271c per share by IFRS3 legislation. This revaluation had to be recorded as an expense of R95 million. This was repeated in June of 2014 when the share price rose to 290c per share (a recorded loss of R9.4 million).

This explains the large drop in earnings in Figures 8 and 9 below in years 2014 and 2015, as well as the poorer metrics in those years in Figure 7 above.

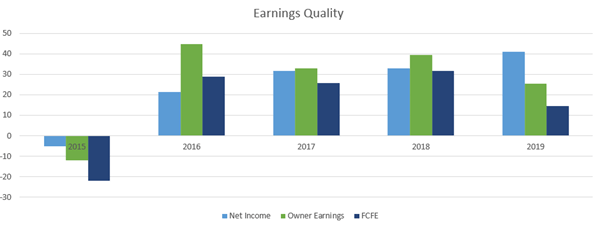

Figure 8 below shows the relationship between net income (EPS), owner earnings, and free cash flow. The more similar they are, the higher the quality of earnings. Here, ALH has had a high quality of earnings for the past 4 years, during which time they have been expanding internationally.

The company has also been growing revenue steadily over the past decade. The large difference between revenue and operating or net income, as well as the large loss in 2014 distorts the image on the graph, but net income and operating income have been similarly growing since 2007.

The above figures suggest that ALH is growing both in market share and in quality. This growth is attributable to management’s decision to expand internationally.

On the topic of management (which is unpacked below), the company is (as almost all our favourite companies) founder led. Further, since October 2018, management have bought R1.15 million worth of stock with an average price of R2.27 per share. Since the last reporting period, management have bought R150 000 (at R1.81 per share average). Further, they have not sold any since June of 2016. As of the company’s 2019 report, directors and associates own 36% of the company.

All these suggest that management are not only aligned with shareholders but believe very strongly in their business’s prospects and have significant experience in the industry.

While the shortage of engineering skills worldwide may act as a barrier to entry for the industry, it also forces Alaris to pay a premium to its employees, and to invest strongly into reducing employee turnover. The company has 51 employees and invests heavily into IP generation across all entities. Of the 51 employees, 30 are engineers. Of the 30, 16 are involved in research and development. The company has a lucrative graduate programme, which involves offering students bursaries while they are employed at Alaris. Their investment thus far has yielded them 18 patents registered mainly in Europe, the US, Canada, the UK, and South Africa.

To summarize, the essence of the bull case is that Alaris is undervalued relative to the growth prospects of its subsidiaries (each of which is unpacked below) and that over time the market will realise this, driving the market price upwards.

Supporting this thesis is that Alaris enjoys:

- A very niche market with high technical barriers to entry,

- A diverse global customer base, which will act as a hedge to ZAR depreciation and market uncertainty,

- No debt and strong financials,

- Great returns on capital, high margins, and good cash convertibility,

- Consistent growth and IP generation and,

- Aligned management.

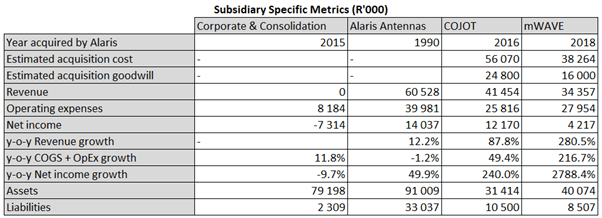

Industry and subsidiary growth prospects

Alaris Holdings was founded in 1990 as the defence division of Poynting Holdings, a general antenna manufacturer. They listed on the JSE in 2008 and struggled through several years until PSG stepped in as an anchor shareholder and helped repair their balance sheet. In 2015, Alaris (the profitable defence division) split from the struggling Poynting which went on to be delisted as a private entity run by the co-founder Andre Fourie.

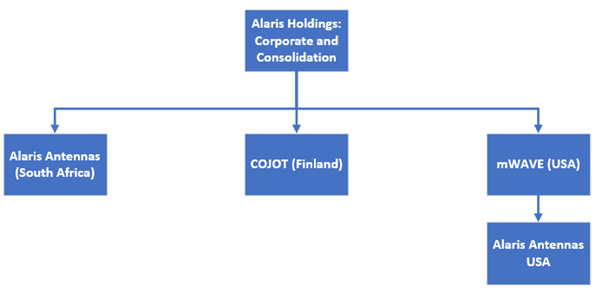

Since 2015, Alaris has reformed its strategy under the leadership of co-founder and current CEO Juergen Dresel, who has been with the company since 2000. As mentioned above, a key strategy of theirs has been to expand into overseas markets through acquisitions. Alaris is now made up of four operating entities (Figure 10), each of which inter-operate and service their own niches.

Alaris’ business is almost exclusively in the defence industry. Its clients are found mainly in international markets and are system integrators, frequency spectrum regulators or in the homeland security space. Their products are vital to the communication, tracking and surveillance systems used in armoured vehicles, aircrafts, naval vessels.

To date, the firm has identified the US as a growth node due to its large defence spending but recognises the challenges (primarily foreign regulations and existing relationships) with trying to break into the market from SA. Hence, they have opted for an acquisitional strategy. The group has a mandate to raise debt levels to between 25-50% of equity if they find high quality deals in the US.

The company used to include another entity: African Union Communications (“Aucom”). Aucom was acquired into Poynting in late 2013 and its acquisition included an earnout mechanism that resulted in complex accounting treatment with nonrecurring adjustments to profits over the three year earn-out period. Aucom was a multi-channel free-to-air and pay TV solution service provider which operate throughout Africa.

Despite outperforming management’s expectations, Aucom was ultimately disposed of in 2017, as management viewed the company as no longer a strategic fit. Alaris, having split from Poynting in 2015, had amended its strategy towards niche domination rather than broad operations. As Aucom was a reseller of antennas, but not in the defence sector and was not contributing towards R&D, Alaris decided to sell it. Since then, they have focused exclusively on buying companies which align with their core business model.

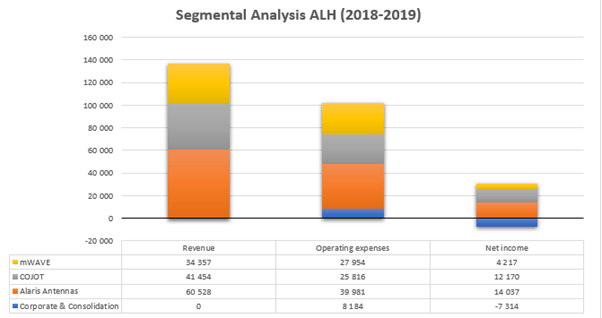

The company’s segmental contributions are outlined in Figures 11 and 12.

Alaris Antennas

Headquartered in SA, Alaris Antennas designs develops and manufactures bespoke and highly specialised RF products. Its (90%) foreign client base consists mostly of system integrators, frequency spectrum regulators and players in the homeland security space.

This segment benefits from large investment into R&D and holds a lot of its own IP, which management believes to be its competitive advantage. In the last reporting period, Alaris Antennas enjoyed large repeat orders which will likely be renewed. It leverages its client base off the international relationships garnered through the other business segments.

The strategy looking forward for Alaris is to focus on closer client interaction. This is leading (as evidenced by the past year’s performance) and will continue to lead towards significant repeat sales. Hopefully, this will cause a stability in revenue income for this segment.

COJOT

Founded in Finland in 1986 and acquired by Alaris in 2016, COJOT also designs, develops, and manufactures niche broadband antennas. Its primary clients are European defence companies and system integrators. Their primary sales regions are in the UK and in Europe because these countries (unlike emerging markets) have system integrator businesses that can buy their products.

In recent years, COJOT has had a focus on European and Asian markets as growth nodes. CEO Juergen Dresel has stated that the geopolitical uncertainty and inter-country rivalry caused by major world events like Brexit and the US-China trade wars have been very good for COJOT’s business as major governments spend more on defence in times of tension.

While COJOT does manufacture some of their own products, they also outsource some manufacturing to partners who experience economies of scale. This subjects them to key partner risk as larger players in their value chain may decide to hike up prices.

Like Alaris Antennas, this company has a strong client-centric model which – because of the specialised and bespoke nature of its products – causes a (mediocre) intangible switching moat based on relationships. Further, COJOT expects that the integration with Alaris USA will yield more exposure to the US market (which is currently negligible for them).

Three important notes on COJOT:

- Their revenue is inconsistent and “lumpy” as it is almost entirely project dependant.

- Management believes that “smart antennas” and drone technology are experiencing increasing demand globally and they are adjusting COJOT’s product range to cater increasingly for this demand.

- They are expanding their premise in the second half of 2020 due to outgrowing their current premises.

mWAVE & Alaris USA

mWAVE is the USA-based segment that Alaris acquired in 2017. It has since created its own sub-division of Alaris USA. Where COJOT is a highly specialised designer, mWAVE deals a little more with the broader market and designs and manufactures both standard and custom microwave antenna products. mWAVE’s products are used across sectors in the scientific, defence and academic communities.

Alaris USA (established in 2019) is the portal through which COJOT and Alaris Antennas market their products to the US market. Both mWAVE and Alaris USA have been integrated into the ERP system of the broader Alaris Holdings group and management expects this integration to yield improved margins for the US segments. All US based clients of COJOT and Alaris Antennas have been handed over to Alaris USA and management expect this business model to increase inter-segmental activities significantly.

The competitive advantage of Alaris USA lies in its ability to offer a broad range of specialised products through its partnerships with COJOT and Alaris Antennas. Its status and location as a US company allows it to capitalise on closer interactions and relationships with its US customer base.

In the US, when the Democrats are in power, defence spending drops significantly. The reverse is true of a Republican victory. Ergo, a Biden victory in the upcoming election is likely to dampen Alaris USA & mWAVE’s revenues somewhat.

One negative arising from the acquisition of mWAVE is the fact that Alaris was willing to settle the R40 million purchase in part with R8 million worth of shares (it earned R6.1 million in net income in 2017, making the purchase on a P/E multiple of 6.6 and generating R16 million of goodwill). Given the relatively small amount of equity used in the deal and the fact that it was not funded with debt, the use of equity is negligible in damaging our opinion of Alaris.

Notably, in the acquisition hunt, Alaris passed on ARA, a US based scientific research and engineering company in favour of mWAVE. As evidenced by the recent results and the Alaris USA division, this was a strategic decision well in line with the group’s decision to narrow its focus to its niche.

Corporate and Consolidation

This is the headquarter division of the group. It produces no revenue and simply absorbs the costs associated with being a listed entity and running shared services (e.g. board remuneration, legal fees, and currency hedging).

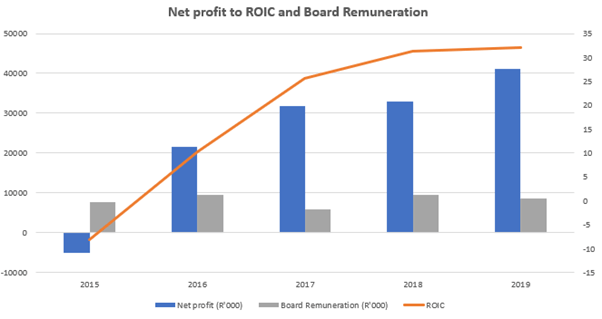

As far as the board’s remuneration goes, the company could do a better job of incentivizing performance for management. As a large portion of the board are company executives, their payments since Alaris split from Poynting has been relatively constant, despite largely improving metrics in terms of ROIC and net income. While this does not mean the board is under-paid, it simply means that payment should correlate more with performance (Figure 13).

One critique of management’s capital allocation thus far has been their share repurchase history (Figure 14). It appears that there is little thought around benefit to shareholders and more thought towards capital raising for the business’ acquisitions. While the acquisitions have undoubtedly brought value to the group, this value has yet to find its way into shareholder’s hands through dividends or a share increase.

In summary, the group at large is looking strategically towards increasing cross-selling opportunities and synergies across segments. Despite the large amount of cash on hand and openness to acquisition, the group has now shifted its strategy towards organic growth and increased IP generation. Each business segment seems well positioned for growth and Alaris has established itself as a dominant player in its niche.

Risk and Odds

When thinking about risk, the potential for loss of capital is paramount. Volatility (and hence beta) is not risk unless a sale locks in the permanent loss of capital. As those with a long-term time horizon can thus afford to forgo a volatility analysis, our risk-taking strategy centres around understanding real threats to the company and to the investment thesis.

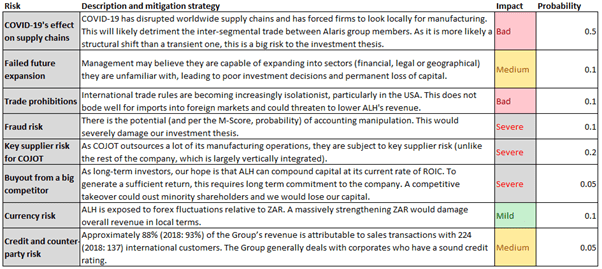

Figure 15 below outlines a broad range of potential risks that may derail the company and/or the thesis. Following this, Figure 16 is a brief overview of a SWOT analysis for ALH to contextualize the risks in Figure 15.

The biggest risk by far to the investment is the potential disruption of COVID-19 on supply chains (Figure 15). As nations consolidate their supply chains and localise their suppliers, isolationism and protectionist policies are likely to flourish. Regarding the short term effects of the virus, CEO Dresel said that the company has a diversified supply chain and sufficient working capital for the short to medium run. However, per analyst Irnest Kaplan‘s comments to the Business Day newspaper, the virus is likely to result in a slowdown in the firms immediate business.

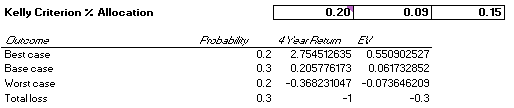

Thus, in our calculations below, the potential for total loss of investment has been set at 30% and the potential for worst case scenario (which includes zero growth over 10 years and a downwards Price/Sales multiple revaluation) at 20%. Thus, the total potential downside for this investment has been set at 50% probability. This is unpacked in the Kelly Criterion in Figure 17.

While the suggested allocation is 20% of one’s bankroll, this is not high enough to warrant a no-brainer bet and is part of why ALH is simply recommended as a company to watch.

Running a simple Monte Carlo simulation on the best-, base- and worst-case scenarios yields a risk-to-gain probability table shown in Figure 18. Evidentially, there is a large spread in potential outcomes. This is attributable largely to the very conservative estimates used in determining risk and in the conservative growth rates (around 20% maximum annually) in the best-case scenario.

As seen, the risk-to-gain probability is slanted uncomfortably towards capital loss at this point, given that the share price has recently surged.

Should the share price fall to around R2/share, the company will become far more appealing from an investment perspective. Although there is likely still significant upside in the long-run, the risk-to-reward odds are no longer stacked in our favour. Hence, it is a temporary watchlist-only allocation for ALH.

If interested, here is a list of sources for an analysis of the RF industry:

- The future of RF in defence industry and a similar article here.

- Military Aerospace news article on the high demands of the RF industry

- A well-written blog over viewing the industr (start here)

- This industry report by Mordor Intelligence is probably the most NB source to read.

- A military article on RF in the defence industry

- A journal report on RF in the military

- Another journal report

- An article by mouser, one of ALH’s biggest competitors

- A research report on an industry analysis

- A local South African reseller

- A news release on an overview of the industry

- An article on radio antennas

- A Fortune industry report

- Engineering news article on innovation in the industry

- A prediction for rapid industry growth

One thought on “Alaris Holdings: A case study on intelligent international expansion.”