The point of this article is to argue – in simple, non-academic terms – for diversification and risk hedging within the concentrated, long-only, equities-based, “value investing” community.

Many who identify as “value investors” run a very concentrated portfolio in the footsteps of Charlie Munger and Mohnish Pabrai. The orthodox reasons for concentration are these:

- Models promoting diversification are based off impractical academic arguments (cf. the CAPM model) which identify beta as risk and,

- If you have the stomach for volatility, then you should embrace it through concentration because:

- It is the fastest way to accumulate wealth (cf. the Kelly Criterion).

- Risk comes from not knowing what you are doing. If you know what you are doing, you need not diversify.

- Diversification begets mediocre results.

While these arguments hold water, especially in their counter to the use of beta as a risk measure, they undervalue the benefits of a truly diversified portfolio in mitigating true risk and enhancing overall returns.

To unpack this, let us return to the first principles: Investing is about buying assets for less than they are worth. This is enabled by market volatility. Volatility (read beta) then, is not risk. Risk is the potential for loss of capital, and rule number one is to not lose capital.

Therefore, the market value of your portfolio drawdown during market corrections is not an accurate reflection of your assumed risk level. Rather, such market volatility provides opportunity to acquire more assets for less than they are worth. Looking to risk mitigation beyond volatility requires thinking about which assets you buy and how you can create structural advantages for yourself in buying them.

Thus, the goal is twofold. Firstly, one must capitalise on market volatility and secondly, one must mitigate risk. There are numerous ways to achieve this, and “stacking” these ways helps to create a structural advantage for yourself. From the outset, true risk of capital loss can be broadly categorized into three buckets:

A. Your original thesis was wrong ab initio (e.g. you strayed outside of your circle of competence and mistook a cyclical upturn for a structural change).

B. Your original thesis becomes wrong over time (e.g. you bet on a great company at a great price, but macroeconomic events curtailed your thesis).

C. A “black swan” event occurred, and you were just unlucky.

All three buckets require decision-making under uncertainty and factoring for what you ultimately do not know (even Mohnish Pabrai famously suggests that you assume a base failure rate of 33% for all your theses. We can be conservative and attribute this solely to the bucket A). This is ignorance risk – you simply do not know what you do not know.

Risk mitigation then must address all three of the above buckets, through the stacking of a variety of ways. To give an example: some ways are behavioural (i.e. not checking stock prices every day or running through a checklist prior to a purchase decision) and can enable you to mitigate risk of poor decision-making and ignorance. Portfolio management opens other ways to mitigate risk in diversification and hedging.

Traditional risk-parity models view diversification as an allocation of volatility across a portfolio of uncorrelated asset classes. The underlying belief here is that when one asset class underperforms, another will outperform as capital is transferred across asset classes (i.e. stocks to gold in a market drawdown). This view of capital allocation holds that the primary goal is to maximise return while minimizing volatility and thus achieve a minimum-variance portfolio.

There exist two issues with traditional risk-parity funds. One is their predominantly macro-economic approach, which requires knowledge of a breadth of asset classes. One man alone cannot know enough about all asset classes to effectively manage a successful macro-risk-parity fund. Thus, extra fees are incurred to both rebalance the assets according to their variance weightings and recent performance, and to curate the necessary knowledge to understand the macro-environment in which such funds operate.

The other issue is leverage. Although the model is adept at spreading risk, traditional risk-parity models require significant amounts of leverage to yield significant returns. The issue with this leverage is that a large amount of the traditional portfolio includes bonds, notoriously negatively skewed investments (small probability of large losses and large probability of small gains). This makes them subject to blow-up risk.

Two principles here are worthy of extraction:

- Multi-asset diversification can aid in the distribution of risk (albeit one of permanent capital loss rather than volatility) through inversely correlated assets.

- The market occasionally experiences selloffs in one asset class that make another intrinsically more valuable.

As equity investors, these two principles are not to be scoffed at. To achieve the goal of compounding capital through acquiring quality equity far below its intrinsic value, it would help to have insurance for the broader market selloffs. Not only would this insurance hedge our own losses, but it would give us the liquidity when it is most valuable. The cost of this insurance would have to be weighed against its potential reward, but as Buffett said: “cash combined with courage in a time of crisis is priceless”.

“Fat tail” hedging strategies or long-volatility funds which use options strategies to capitalise on price fluctuations are a great way to implement effective diversification into a portfolio of assets. These funds typically offer convex upside during market crashes, but have “bleed” during years of stability, but this is limited downside that can be offset by the portfolio growth during these years.1 They are essentially a “heads I win, tails I don’t lose much” type of bet. Their small downside is offset by the gains from the broader equity positions, while they offer unknown upside when all else is crashing.

These strategies will not mitigate bucket A type risk, but it will hedge against broader market drawdowns – providing you with several ways of mitigating risk:

- Liquidity in a crisis and the acquisition of more assets,

- Continued compounding without drawdown effects,

- Behavioural security from selling during a panic selloff – or “seeing green keeps you keen”.

The downside mitigation provided by fat-tail hedges is primarily for bucket C type risk and broad market drawdowns. Using options to hedge volatility on individual positions is unlikely to be cheap enough to generate alpha net of costs. However, using an ensemble of long volatility funds can provide a hedge against multiple volatility “paths”, all of which are unknown prior to the correction.

The second form of diversification that helps to mitigate risks in buckets A and B is to run a less concentrated portfolio, and to diversify it across geographic and industrial lines.2 The benefits here primarily come from hedging against the impact of structural geographic deficiencies (i.e. USD depreciation vs Chinese economy; or SA’s economic left-tilt & corruption damaging its business prospects over time). Secondary benefits – of industrial diversification – come from the mitigation of loss caused by secular inter-industry trends (i.e. newspapers).

It is this second form of diversification that is eschewed by most value investors. Many will hold that they already mitigate risk by either a) not investing in declining industries or, b) only buy deep-value companies within these industries. While these are good ways of risk management, they are only one strategy.

It is here that most value investors suffer from overconfidence. Risk comes from not knowing what you are doing, yes. But risk also comes from all the many biases you are prone to, from things outside of your control, and from being on the wrong end of dumb luck. Successful risk management comes not from one or two great strategies, but from stacking five, six, or seven different ways on top of each other. The scope of this paper is not to outline all the many methods of risk mitigation, but rather to suggest that diversification and tail-hedging should be a layer in all decision-making stacks.

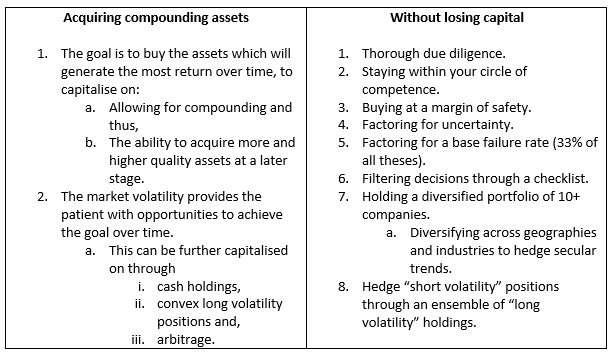

To recap:

- The goal is to acquire high quality assets for far less than they are worth and hold them until they are no longer worth keeping.

- There could be better assets of the same price or cheaper ones of equal quality or,

- The asset has deteriorated.

- To do the above without losing capital.

This can be subdivided into the below:

[1] Where long volatility is better than the typical bonds or gold allocation is in its direct application to equities. Both bonds and gold appreciate counter to equities (historically), but in significant shifts in correlation regimes, such as observed in Q1 2020, almost all assets experience a selloff. Barring long volatility which, by nature, appreciated.

[2] This is a tougher one to justify early in one’s career, given the benefits of specialisation that come from having your circle of competence within one geography and only a handful of industries. The counter to this is that understanding multiple industries across countries provides for a more robust development of mental models.